Moving into retirement changes the way you look at a bank statement. Without a daily commute or the demands of raising a family, expenses that once felt mandatory quickly become prime targets for the chopping block. Retirees are actively auditing their monthly bills to ensure every dollar supports their new lifestyle instead of funding outdated habits. From consolidating streaming services to rethinking insurance policies, shifting your budget allows you to combat inflation and protect your nest egg. By identifying these common financial drains, you can comfortably eliminate unnecessary costs without sacrificing your quality of life. Here is exactly what budget-conscious seniors are cutting first.

At a Glance

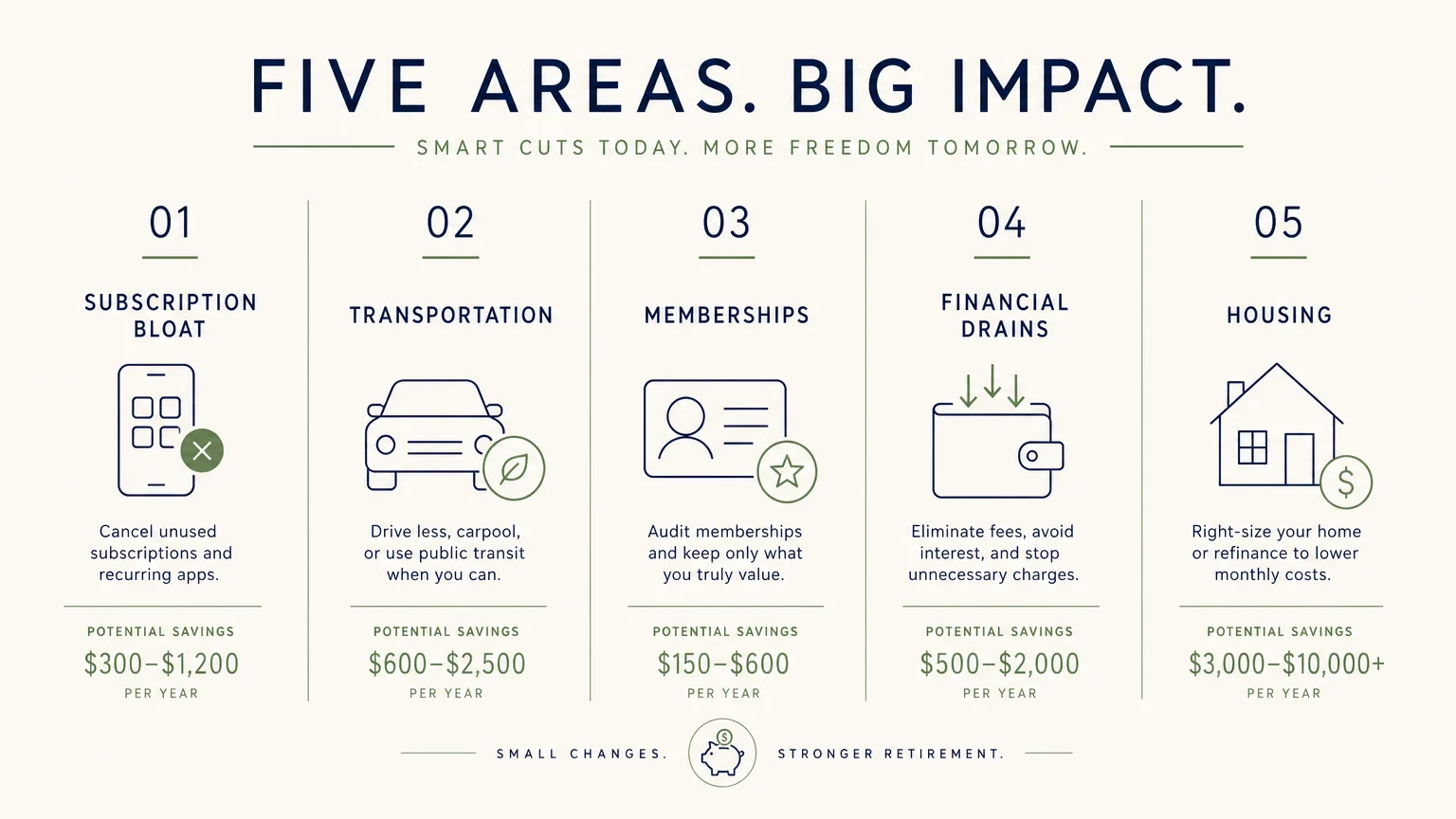

- Subscription Bloat: Consolidating cable and streaming services saves hundreds of dollars a year.

- Transportation: Selling a second vehicle eliminates insurance, maintenance, and registration costs.

- Memberships: Utilizing Medicare Advantage fitness perks replaces expensive out-of-pocket gym fees.

- Financial Drains: Downgrading premium credit cards and high-fee investment accounts protects your actual wealth.

- Housing: Downsizing from an oversized family home cuts property taxes and constant upkeep.

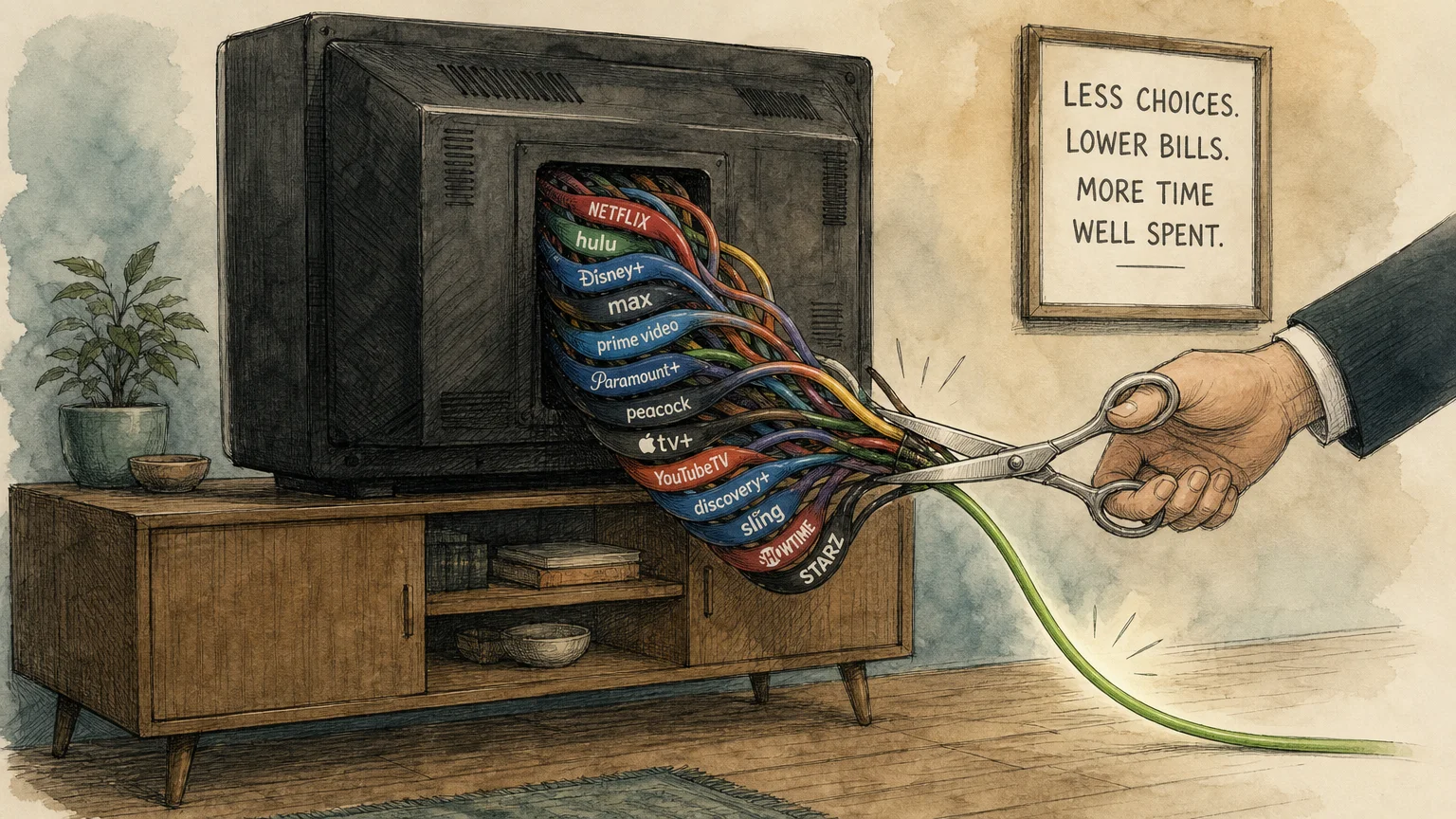

1. Cable TV and Duplicate Streaming Services

Entertainment costs often spiral out of control during your working years because you simply do not have the time to audit your subscriptions. By 2026, the average traditional cable bill hovers around $147 per month. Over a year, that is nearly $1,800 dedicated solely to television—a steep price when you likely only watch a handful of channels.

Retirees are cutting the cord, but they are also getting smarter about the streaming services that replace it. It is easy to accumulate five or six different streaming platforms at $15 to $20 a piece, which quickly recreates the cost of a bloated cable package. Budget-conscious seniors are adopting a strategy called “churning.” Instead of paying for Netflix, Hulu, Disney+, and Max all year long, they subscribe to one service for a few months, watch the shows they want, and then rotate to a different platform. This simple adjustment keeps your entertainment fresh while keeping your monthly bill under $30.

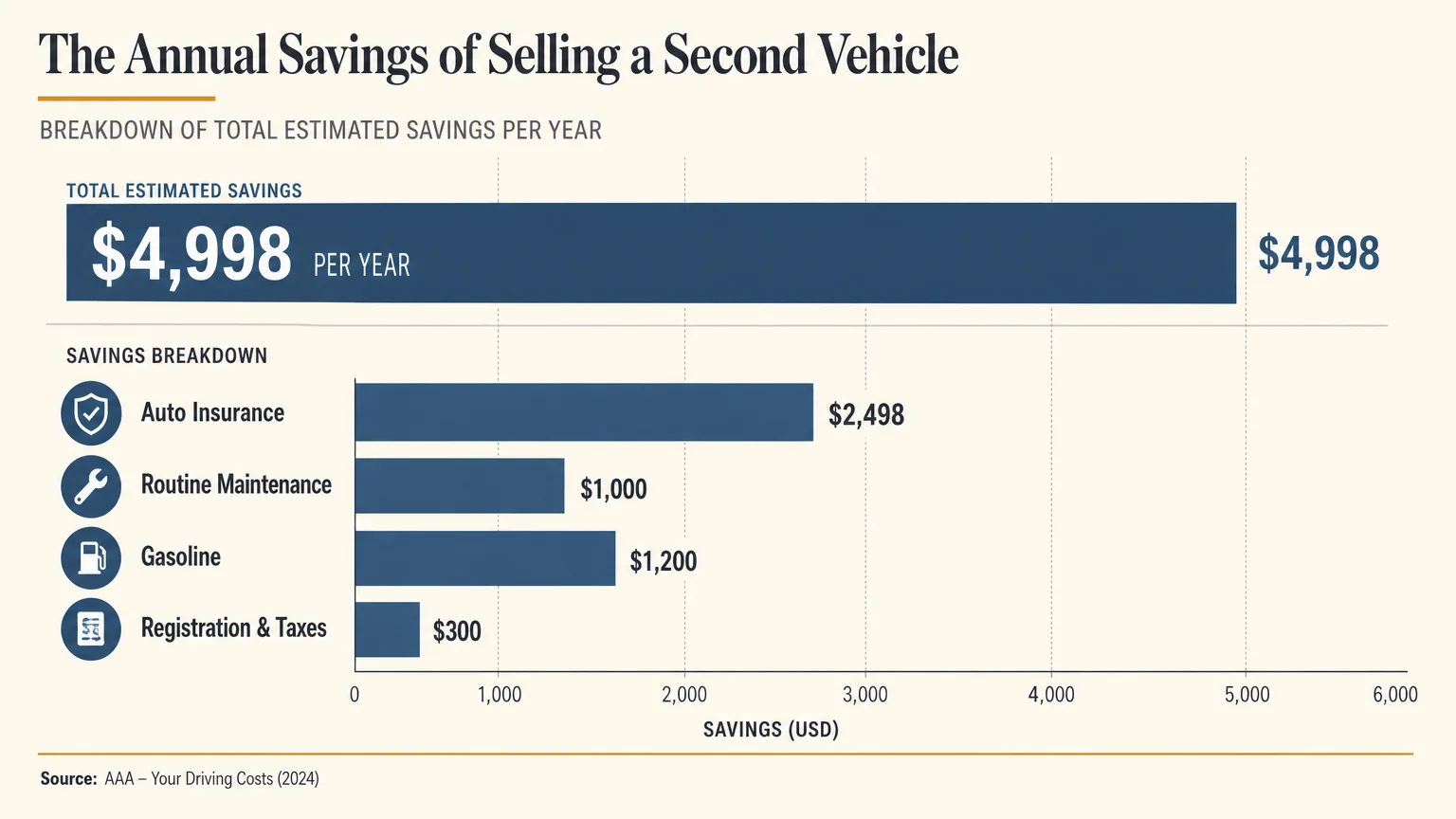

2. The Second Family Vehicle

When two spouses are commuting to different jobs, a two-car household is a necessity. In retirement, that second vehicle often sits in the driveway collecting dust, yet it continues to drain your bank account every single month.

According to current auto insurance data, the “age premium curve” means rates hit their lowest around age 60, but begin creeping back up after age 70 as statistical risks increase. The average full-coverage policy for a 70-year-old driver is approximately $2,498 per year. When you add in routine maintenance, gasoline, and local registration fees, that idle car is remarkably expensive.

| Expense Category | Estimated Annual Cost for a Second Vehicle |

|---|---|

| Auto Insurance (Age 70+) | $2,498 |

| Routine Maintenance & Repairs | $1,000 |

| Gasoline (Moderate Driving) | $1,200 |

| Registration & Local Taxes | $300 |

| Total Estimated Savings | $4,998 per year |

Selling the second car not only provides an immediate lump sum of cash to add to your savings, but it also permanently deletes roughly $5,000 in recurring annual expenses from your retirement budgeting spreadsheet.

3. Out-of-Pocket Gym Memberships

Staying active is a critical part of aging well. The National Institute on Aging routinely emphasizes that regular physical activity improves balance, builds stamina, and reduces the risk of chronic conditions. However, you do not need to pay a commercial gym $40 to $100 a month to maintain your health.

Many retirees are cutting their expensive health club memberships in favor of programs like SilverSneakers. While Original Medicare (Part A and Part B) does not cover fitness programs, many Medicare Advantage (Part C) plans include fitness benefits at no additional cost. These programs provide free access to thousands of participating gyms, recreation centers, and online fitness classes across the country. If you are paying out of pocket for a treadmill you only use twice a week, checking your Medicare Advantage plan for included fitness benefits is an easy way to save $600 or more annually.

4. Premium Travel Credit Cards

During your peak earning and traveling years, carrying a premium travel credit card makes a lot of sense. Cards like the Platinum Card from American Express or the Chase Sapphire Reserve charge annual fees ranging from $400 to $695. In exchange, they offer luxury perks like airport lounge access, airline fee credits, and elite hotel status.

Retirees are taking a hard look at whether their travel habits still justify these massive fees. If you are taking one or two direct flights a year to visit grandchildren, airport lounge access loses its value. Furthermore, premium cards often require you to jump through hoops—like booking through specific portals or using specific vendor credits—to break even. Many seniors are cutting these expensive cards and switching to simple, no-annual-fee cash-back cards. Earning a flat 2% cash back on groceries and medical bills is often far more lucrative for a retiree than chasing airline miles.

5. Unnecessary Life Insurance Policies

Life insurance is designed to replace your income and protect your dependents if you pass away unexpectedly. But once you reach retirement, the financial landscape shifts. Your mortgage is likely paid off, your children are financially independent adults, and you are no longer relying on a steady paycheck that needs replacing.

Retirees are frequently dropping expensive life insurance premiums that no longer serve a purpose. If you hold a term life policy that is becoming exorbitantly expensive to renew in your 60s or 70s, letting it expire is often the right move. If you hold a permanent whole life policy, you might be paying high premiums to maintain a death benefit your heirs do not actually need to survive. Some retirees choose to surrender these permanent policies, taking the accumulated cash value as a lump sum to bolster their immediate retirement savings.

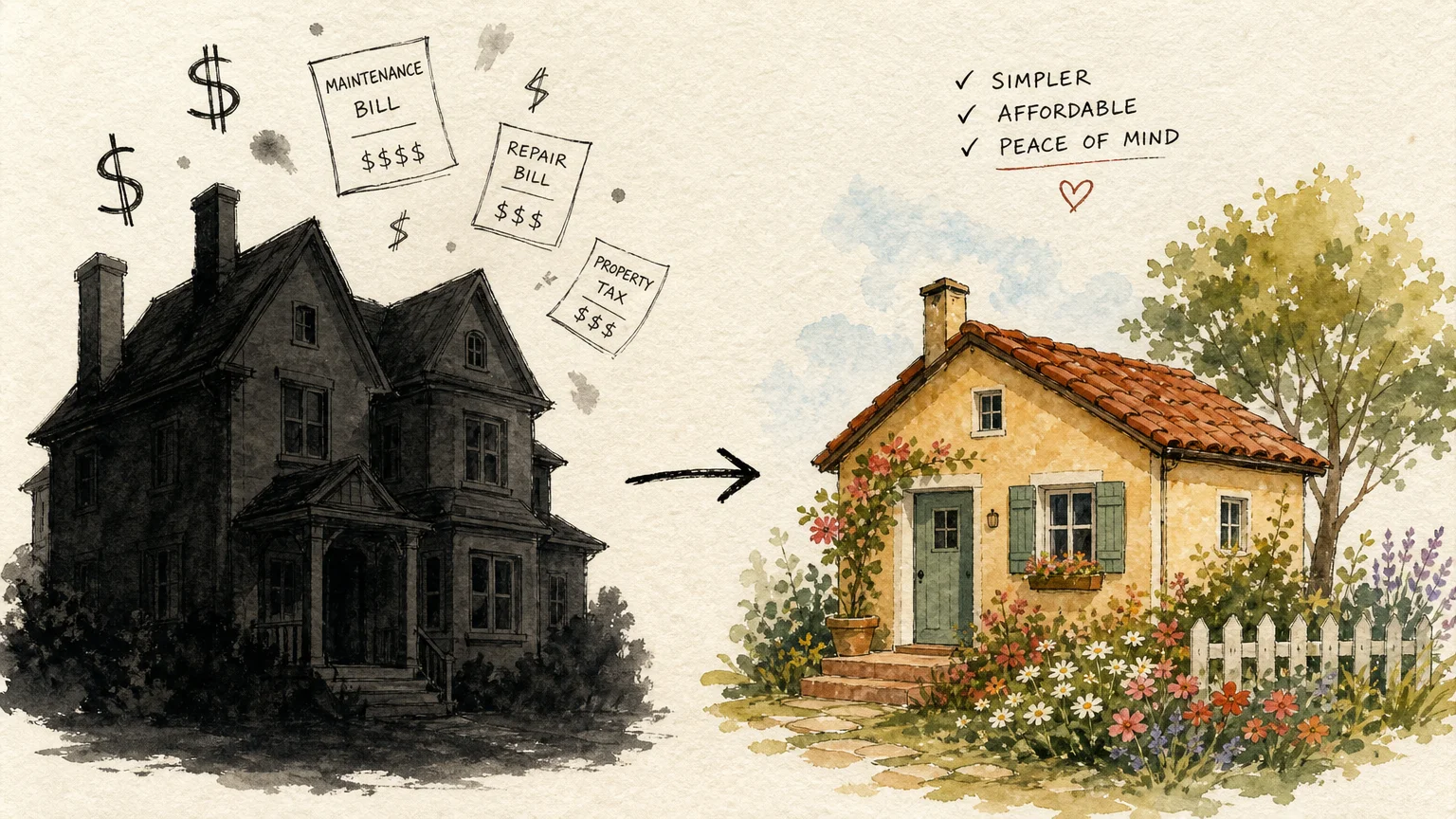

6. The Hidden Costs of “Over-Housing”

Your four-bedroom family home holds decades of memories, but it also holds an incredible amount of hidden costs. Heating and cooling empty rooms, paying property taxes on square footage you never use, and keeping up with endless repairs will drain a fixed income rapidly.

A common rule of thumb in real estate is that a homeowner should budget 1% to 4% of their home’s value for annual maintenance. On a $400,000 home, that is $4,000 to $16,000 a year just to keep the roof intact, the lawn mowed, and the appliances running. Downsizing to a smaller, more manageable property—such as a condominium or a single-story patio home—drastically reduces property taxes, utility bills, and maintenance costs. It also eliminates the physical toll of cleaning a massive house, allowing you to spend your time and money on experiences rather than upkeep.

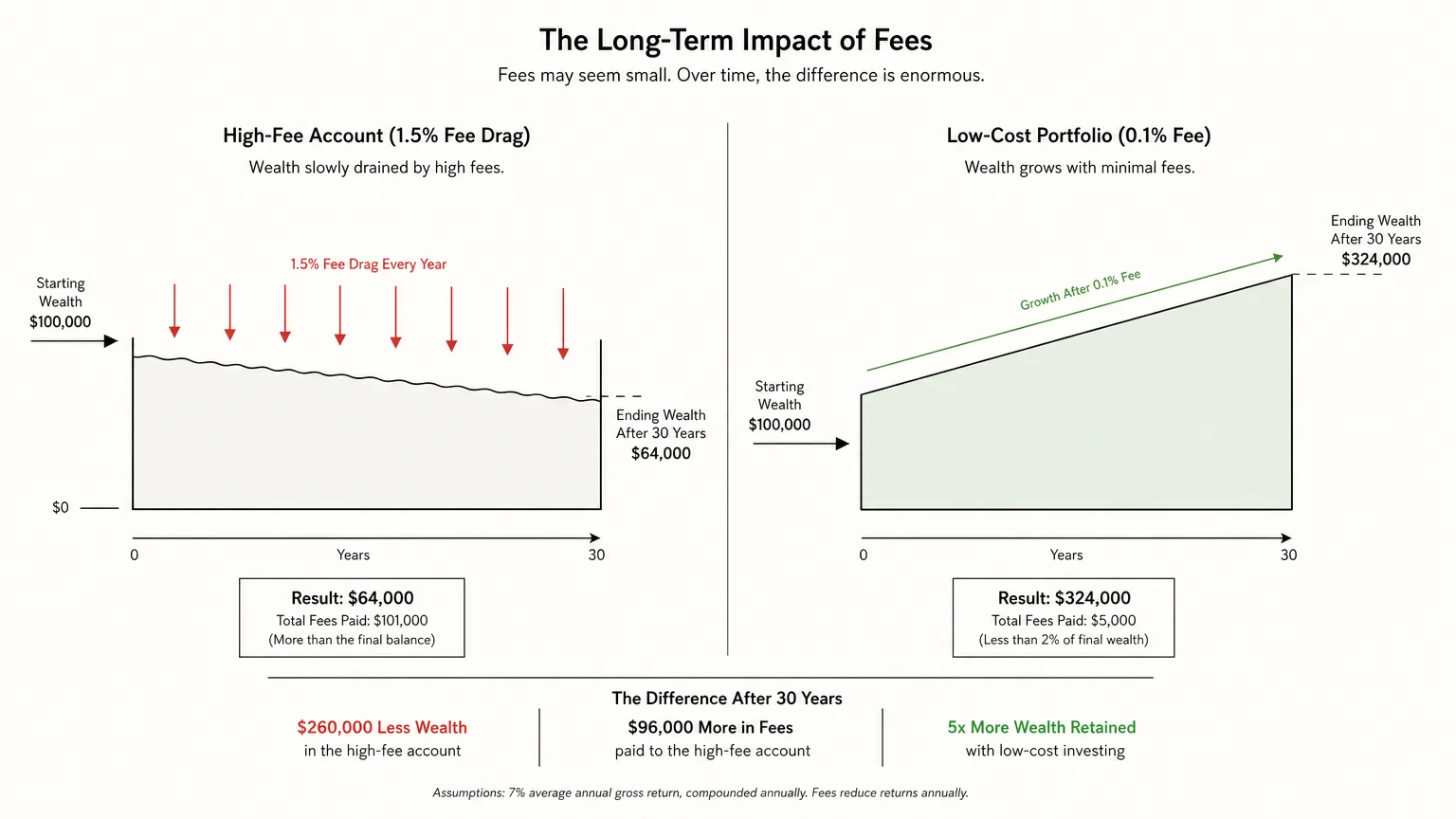

7. High-Fee Financial Advisor Accounts

When you are building your wealth, paying a financial advisor 1% to 1.5% of your assets under management (AUM) might feel reasonable for the growth they provide. But in retirement, when your focus shifts from aggressive growth to wealth preservation and income generation, those fees take a massive bite out of your nest egg.

According to the Consumer Financial Protection Bureau, maximizing your retirement income requires careful budgeting and an awareness of exactly where your money is going. A 1% fee on a $500,000 portfolio costs you $5,000 every single year, regardless of whether the market goes up or down. Retirees are increasingly moving away from high-fee advisory accounts. Instead, they are consolidating their money into low-cost index funds or hiring flat-fee, fee-only fiduciaries who charge a set hourly rate for a financial checkup. This move alone can save tens of thousands of dollars over a 20-year retirement.

8. Frequent Dining Out and Food Delivery Apps

The convenience of food delivery apps and frequent restaurant meals often peaks just before retirement, when time is scarce and work stress is high. Once you retire, you gain back the luxury of time, making expensive convenience food entirely unnecessary.

The markup on apps like UberEats or DoorDash is staggering when you account for service fees, delivery fees, inflated menu prices, and tips. A $15 burger can easily cost $25 by the time it reaches your door. Retirees are cutting these services entirely and reducing their restaurant outings. Instead of paying a 300% markup on dinner and drinks, they are optimizing their grocery runs, cooking elaborate meals at home, and shifting their social dining to more affordable lunch menus or home-hosted potlucks. Taking control of your food budget is one of the fastest ways to inject extra cash into your daily life.

Worth Keeping in Mind

- Insurance network changes: If you change your Medicare Advantage plan solely to get a free gym membership, ensure your preferred doctors and specialists are still in-network on the new plan.

- Transportation logistics: Before selling your second car, try doing a “dry run” for a month. Park the car and do not use it to see if sharing one vehicle causes logistical stress for you and your partner.

- Life insurance alternatives: If you drop your life insurance, ensure your estate has enough liquid cash to cover your final expenses and funeral costs so you do not burden your surviving family members.

- Downsizing costs: Remember that selling a home comes with closing costs, agent commissions, and moving expenses. Make sure the long-term savings of a smaller home outweigh the immediate costs of moving.

When to Get Professional Help

- Altering investment accounts: Moving money away from a high-fee advisor into a new brokerage can trigger capital gains taxes if not handled correctly. A tax professional can help you execute direct transfers to avoid accidental tax bills.

- Surrendering permanent insurance: Cashing out a whole life policy can sometimes result in taxable income if the cash value exceeds the premiums you paid. Consult a fiduciary before signing surrender paperwork.

- Selling a primary residence: If your home has appreciated significantly over the decades, you may face capital gains taxes upon selling, even with the primary residence exclusion. A certified public accountant (CPA) can help you plan the sale efficiently.

Trimming your expenses does not mean restricting your lifestyle; it means reallocating your money toward the things that actually matter to you right now. By eliminating outdated subscriptions, right-sizing your transportation, and refusing to pay unnecessary fees, you take absolute control of your fixed income. A leaner, smarter budget leaves you with more freedom to travel, spoil your grandchildren, and enjoy the retirement you worked so hard to build.

This article provides general information only. Every reader’s situation is different—what works for others may not be the right fit for you. For personalized guidance on health, legal, or financial matters, consult a qualified professional.

Last updated: June 2026. Rules, prices, and details change—verify current information with official sources before acting on it.