Deciding when and how to claim Social Security is one of the most critical financial choices you will make, and being married adds entirely new layers to the math. Spousal and survivor benefits offer powerful ways to maximize your household income, but strict age limits, earnings caps, and hidden deadlines can easily derail your retirement if you miscalculate. You cannot afford to guess how these rules apply to your unique timeline. Whether you are coordinating a dual-income retirement or planning for a spouse who stayed home, understanding exactly how the Social Security Administration views your marriage ensures you capture every dollar you have earned. Here is exactly how the rules work for couples navigating the system today.

The Mechanics of Spousal Benefits

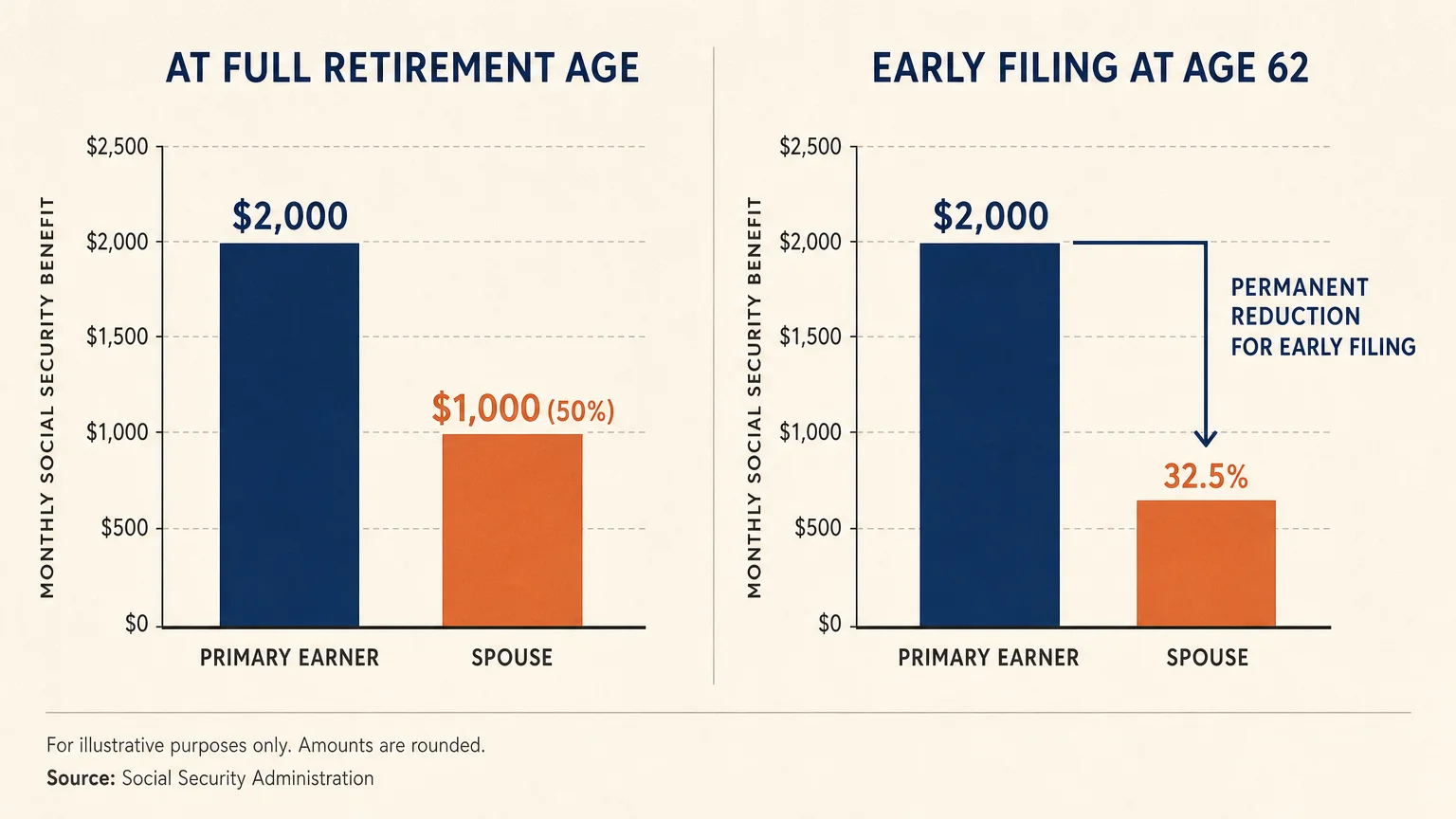

1. Spousal benefits cap at 50% of the worker’s primary insurance amount

The absolute maximum a spouse can receive on their partner’s work record is 50% of the primary earner’s full retirement age benefit. If your spouse’s full benefit is $2,000 a month, your maximum spousal benefit is $1,000. Claiming this spousal benefit does not reduce the primary earner’s check. However, to get that full 50%, you must wait until your own full retirement age to file. If you claim the spousal benefit early—as early as age 62—the Social Security Administration permanently reduces your percentage. For instance, claiming at 62 could reduce your spousal benefit to as little as 32.5% of the primary earner’s amount.

2. You cannot claim a spousal benefit until your partner actually files

You cannot receive a spousal benefit while your partner continues to defer their own retirement application. Even if you reach your full retirement age, the Social Security Administration will not pay you a spousal benefit until the primary earner officially files for their benefits. This rule requires strategic coordination. If the higher earner plans to delay claiming until age 70 to maximize their payout, the lower earner must also wait to access spousal benefits, though they can still claim their own individual benefit in the meantime if they qualify.

3. Waiting past full retirement age does not increase a spousal benefit

Workers who delay claiming their own retirement benefits past their full retirement age earn delayed retirement credits, boosting their payout by 8% per year up to age 70. Spousal benefits do not work this way. A spousal benefit maxes out at the claimant’s full retirement age. Waiting until age 68, 69, or 70 to claim a spousal benefit provides no financial advantage whatsoever. If your strategy relies primarily on spousal benefits, delaying past your full retirement age only means you forfeit months of checks.

4. The dual entitlement rule pays your own earned benefit first

You cannot double-dip by collecting your full individual benefit plus a full spousal benefit. Under the dual entitlement rule, the Social Security Administration always pays out your own earned benefit first. If your earned benefit is lower than your spousal benefit, the agency adds a supplemental amount to bring your total check up to the spousal maximum. For example, if your own benefit is $800 and your spousal benefit limit is $1,000, Social Security pays your $800 plus a $200 top-up. The end result is a $1,000 check, not $1,800.

Rules for Surviving Spouses

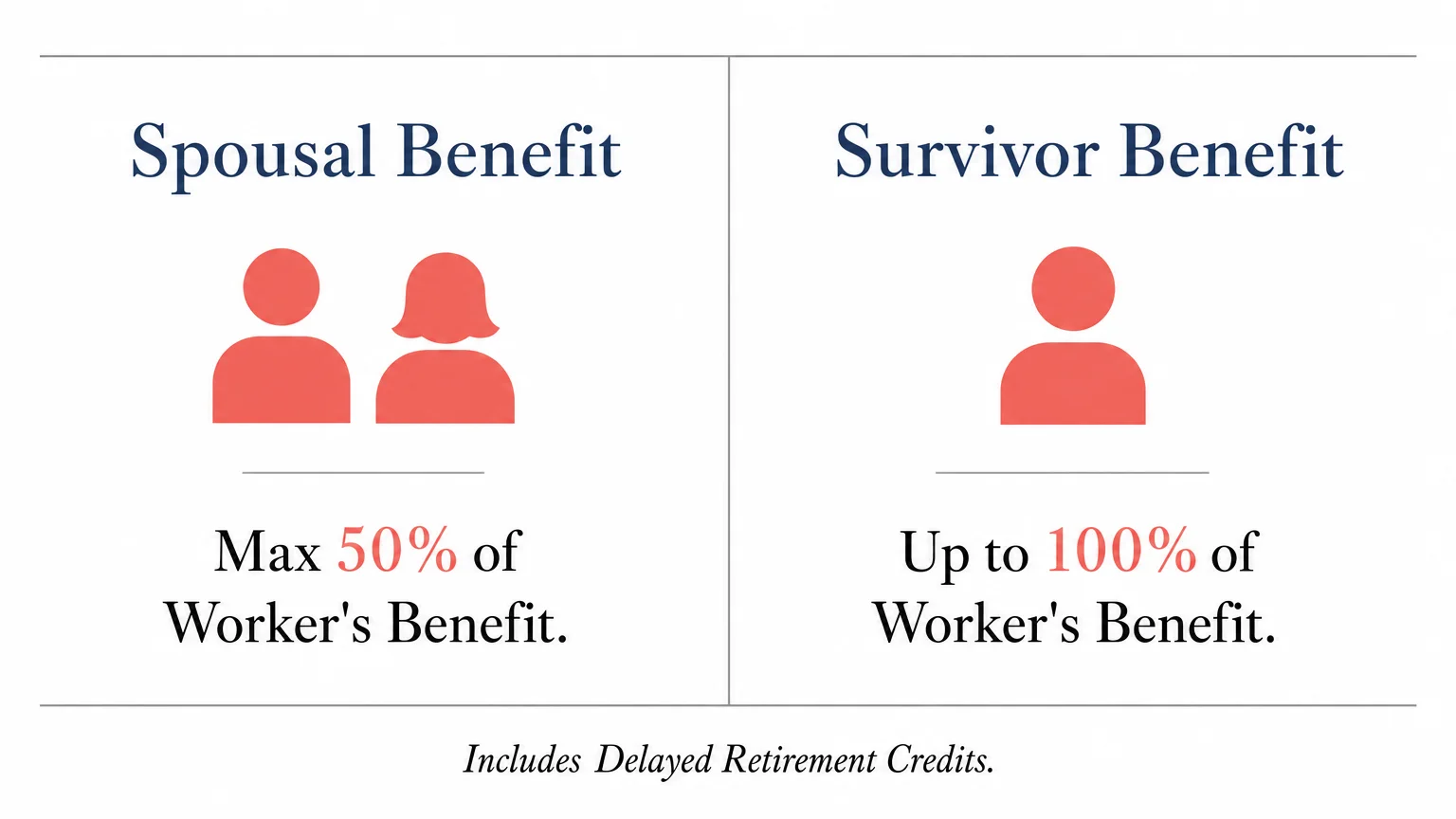

“The distinction between spousal and survivor benefits is where most costly mistakes happen. A spousal benefit is designed to supplement a living partner’s income, while a survivor benefit is meant to entirely replace the financial gap left by a spouse’s death.”

5. Survivor benefits can replace 100% of the deceased spouse’s check

Unlike spousal benefits, which are capped at 50%, survivor benefits can pay up to 100% of the deceased worker’s benefit. This includes any delayed retirement credits the deceased spouse accumulated by waiting to file. If the higher earner delayed their claim until age 70 and built a $3,500 monthly benefit, the surviving spouse can step into that exact $3,500 payment. However, when a spouse passes away, the household loses the smaller of the two Social Security checks; you receive the higher survivor benefit, but your own lower benefit stops.

6. You can claim a survivor benefit as early as age 60

While standard retirement and spousal benefits become available at age 62, surviving spouses can access survivor benefits starting at age 60 (or age 50 if the survivor has a qualifying disability). Claiming at age 60 permanently reduces the payment to 71.5% of the deceased spouse’s full amount. The monthly payout increases incrementally for every month you delay filing, reaching the full 100% replacement rate once you hit your survivor full retirement age.

7. You can switch between survivor benefits and your own retirement

Since 2015, new laws eliminated the ability to switch between spousal and individual benefits for most retirees. However, surviving spouses retain a powerful loophole: you can restrict your application to just one type of benefit and let the other grow. For instance, a widow might claim a reduced survivor benefit at age 60, allowing her own individual retirement benefit to grow untouched until it maximizes at age 70. At 70, she can switch to her own benefit if it provides a higher monthly payout. This requires actively filing the separate claims; the Social Security Administration does not switch you automatically.

8. Remarrying before age 60 permanently forfeits your survivor benefits

Marriage timing strictly dictates survivor eligibility. If a widow or widower remarries before turning 60 (or 50 if disabled), they lose their eligibility to collect survivor benefits on their deceased spouse’s work record. The payments simply stop. However, if the remarriage happens at age 60 or older, the survivor keeps full access to the deceased spouse’s benefits. The older couple can then decide whether the survivor should draw from the deceased spouse, the new spouse, or their own record, depending on which yields the highest check.

Divorce and Blended Families

9. Divorced spouses can claim on your record if the marriage lasted 10 years

Divorce does not necessarily sever your Social Security ties. If your marriage lasted at least 10 consecutive years and you are currently unmarried, you can claim spousal benefits based on your ex-spouse’s earnings history. You must be at least 62 years old, and your ex-spouse must be eligible for retirement benefits. Unlike current couples, if you have been divorced for at least two continuous years, you can claim the divorced spousal benefit even if your ex-spouse has not yet filed for their own benefits.

10. An ex-spouse’s claim does not reduce your current family’s benefits

A common fear in blended families is that an ex-spouse claiming benefits will drain the pool of money available to the current spouse. The Social Security Administration processes divorced spousal claims entirely separately. If your ex-spouse files for a benefit based on your earnings record, it has zero impact on your own monthly check, and it does not reduce the maximum spousal or survivor benefits available to your current spouse. The SSA does not even notify you when an ex-spouse files a claim.

Working, Taxes, and Deadlines

11. Earning over $24,480 before full retirement age triggers the earnings penalty

If you claim Social Security before your full retirement age but continue working, your income is subject to the retirement earnings test. For 2026, the standard earnings limit is $24,480. If you earn more than this threshold, the SSA withholds $1 of your benefits for every $2 you earn over the limit. In the specific calendar year you reach full retirement age, the limit jumps to $65,160, and the penalty drops to $1 withheld for every $3 earned above the limit—counting only earnings made before your birthday month.

12. Withheld money from the earnings test is not lost forever

Many couples mistakenly believe the earnings penalty permanently confiscates their benefits. It does not. The money withheld due to the Social Security earnings limit is simply deferred. Once you reach your full retirement age, the SSA recalculates your monthly benefit upward to account for the months you did not receive a check. Over the rest of your retirement, this higher monthly payment returns the withheld funds, assuming you live into your average life expectancy.

13. Full retirement age is firmly set at 67 for most upcoming retirees

The concept of full retirement age dictates exactly when you get 100% of your earned benefit, your spousal benefit, and avoids the earnings penalty. For anyone born in 1960 or later, full retirement age is exactly 67. The age scale slowly increased from 65 to 67 over several decades, but that transition is now complete. Miscalculating this age by assuming it is 65 will result in a permanent reduction to your lifetime monthly income.

14. The $255 death benefit requires swift action

When a spouse passes away, the surviving spouse is typically eligible for a one-time lump-sum death payment of $255. While the amount is incredibly modest—it has not increased since the 1950s—it is a guaranteed benefit meant to offset immediate costs. However, you must formally apply for this payment within two years of the date of death. Miss the deadline, and the funds are forfeited entirely.

Comparing Spousal and Survivor Benefits

Understanding the strict differences between these two benefit types helps couples plan their long-term financial security more accurately.

| Feature | Spousal Benefit (Living Spouse) | Survivor Benefit (Deceased Spouse) |

|---|---|---|

| Maximum Percentage | 50% of the primary earner’s full retirement age amount. | 100% of the deceased spouse’s actual payment amount. |

| Earliest Claim Age | Age 62 (unless caring for a qualifying child). | Age 60 (or age 50 if disabled). |

| Delayed Retirement Impact | Primary earner delaying past full retirement age does not increase spousal benefit. | Primary earner delaying past full retirement age directly increases the survivor payout. |

| Remarriage Rules | Divorced spousal benefits stop entirely if the claimant remarries at any age. | Survivor benefits continue seamlessly if the claimant remarries at age 60 or older. |

Things to Watch Out For

Navigating joint Social Security claims requires avoiding a few common traps that permanently impact your income.

- Assuming automatic enrollment: Social Security rarely switches your benefit automatically. If your spouse dies, and you are already collecting your own retirement benefit, you must proactively apply for the survivor benefit. It will not automatically appear in your bank account.

- Filing too early out of fear: Claiming at 62 locks in a permanent reduction of up to 30% for your own benefit, and heavily reduces your spousal payout. Unless health or immediate financial necessity dictates otherwise, locking in a lower payout limits your options later in life.

- Ignoring the tax implications: Up to 85% of your Social Security benefits become taxable if your combined household income exceeds $32,000. For dual-income retirees pulling from pensions, 401(k)s, and part-time work, this tax bite can take a heavy toll if not managed correctly.

- Forgetting Medicare premium deductions: By law, Medicare Part B premiums are deducted directly from your Social Security checks. When projecting your monthly household budget, remember that the gross benefit amount you see on your statements will be reduced by these healthcare premiums before hitting your bank account.

When DIY Isn’t Enough

While basic claiming rules are public, certain marital situations create immense complexity. In these specific scenarios, relying on free online calculators is risky, and professional guidance is strongly recommended.

- Government Pension Offset (GPO): If you or your spouse receives a pension from a government job where you did not pay Social Security taxes (such as certain teaching or state employee roles), the GPO can reduce your spousal or survivor benefits by two-thirds of your pension amount—sometimes wiping out the Social Security check entirely. A specialized advisor is crucial here.

- Significant age gaps: When spouses have an age gap of 10 years or more, the survivor benefit becomes the single most important factor in the older spouse’s filing strategy. A planner can mathematically model the exact month the older spouse should claim to protect the younger spouse’s longevity risk.

- Terminal illness diagnoses: If either spouse faces a shortened life expectancy, conventional wisdom about delaying benefits goes out the window. A financial professional can help you structure immediate claims to ensure the surviving spouse is positioned correctly without sacrificing vital liquidity.

Every dollar you secure through Social Security represents a direct return on decades of hard work. By treating your marital benefits as a strategic household asset rather than a simple individual payout, you protect your standard of living against inflation, market downturns, and unexpected life events. Review your earnings statements annually, run the math together, and make your claiming decisions based on the rules as they exist today.

This article provides general information only. Every reader’s situation is different—what works for others may not be the right fit for you. For personalized guidance on health, legal, or financial matters, consult a qualified professional.

Last updated: June 2026. Rules, prices, and details change—verify current information with official sources before acting on it.