The banking landscape in 2026 is shifting, and retirees must adapt their strategies to protect their hard-earned savings. With the Federal Reserve stabilizing interest rates after a series of late-2025 cuts, locking in certificate of deposit yields before they drift lower is a top priority. Meanwhile, changing consumer regulations, accelerated local branch closures, and the rapid expansion of instant payment networks force older Americans to rethink how they access their money. Understanding these distinct adjustments allows you to avoid overdraft fees, sidestep new transfer delays with your Social Security direct deposits, and maximize your federal deposit insurance coverage. Here is exactly what you need to know to navigate your retirement finances safely this year.

1. CD Yields Are Stabilizing After Recent Rate Cuts

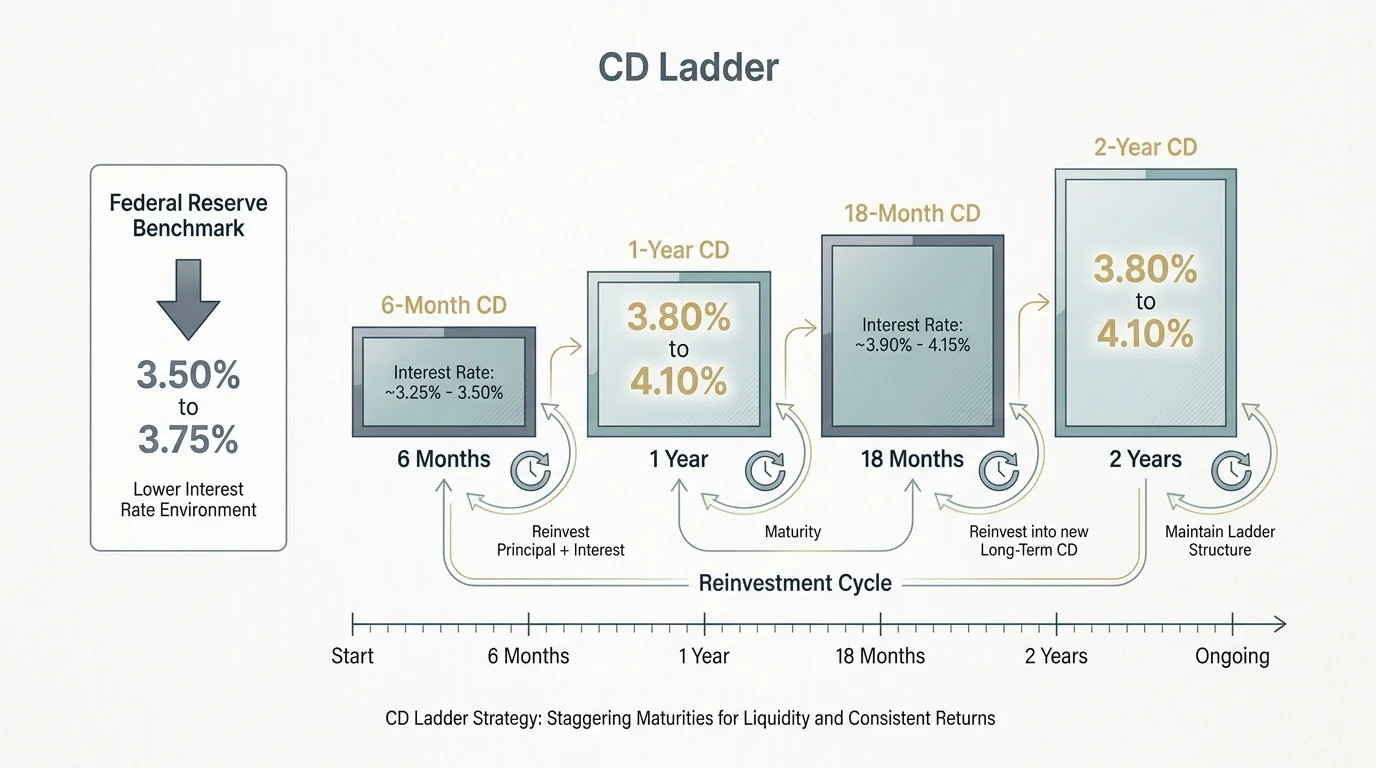

If you rely on interest income to supplement your retirement budget, you have likely noticed that the days of guaranteed 5.5% certificate of deposit (CD) returns are over. The Federal Reserve implemented a series of rate cuts in the latter half of 2025, bringing the federal funds benchmark rate down to the 3.50% to 3.75% range. For 2026, the central bank has signaled a pause—meaning the rapid decline in rates has slowed, but yields are not climbing back to their recent peaks.

As of May 2026, top online banks are offering CD rates hovering around 3.80% to 4.10% for one-year and two-year terms. While this represents a drop from previous years, these yields still comfortably outpace inflation, which is currently holding near 3%. Because banks price their CDs based on future expectations, locking in a rate now protects your cash if the Fed resumes cutting rates later in the year.

Instead of putting all your cash into a single long-term CD, consider building a CD ladder. This strategy involves dividing your investment across multiple terms—such as six months, one year, eighteen months, and two years. As each CD matures, you can reinvest the funds at the current rate or use the cash for living expenses. This provides a steady stream of accessible money without sacrificing the higher yields associated with longer commitments.

| CD Strategy | How It Works | Best For |

|---|---|---|

| Short-Term Ladder (6 to 12 months) | Splitting funds across 3-month, 6-month, and 12-month CDs. | Retirees who need frequent access to cash for upcoming medical or household expenses. |

| Long-Term Ladder (1 to 3 years) | Locking money into 1-year, 2-year, and 3-year terms. | Protecting a portion of your portfolio against projected Federal Reserve rate cuts. |

| No-Penalty CDs | Accepting a slightly lower interest rate in exchange for the right to withdraw funds before maturity without a fee. | Emergency funds that need to earn more than a standard savings account but must remain fully liquid. |

2. Local Bank Branch Closures Continue to Accelerate

The shift away from physical banking is moving faster than ever. In 2025, the banking industry shuttered roughly 8,000 branches globally, with the United States accounting for up to 1,400 of those closures. For younger consumers who manage their finances entirely via smartphone apps, a missing building on Main Street barely registers. But for retirees, the disappearance of local branches removes critical access to in-person services.

Bank consolidation—where larger institutions buy out smaller community banks and close overlapping locations—is heavily impacting suburban and rural areas. If your local branch closes, you lose immediate access to safe deposit boxes, cashier’s checks, in-person notarization, and the ability to withdraw large sums of physical cash quickly. Furthermore, many banks are replacing full-service branches with “smart branches” that feature advanced ATMs but lack loan officers or dedicated customer service representatives.

To stay ahead of this trend, review your current bank’s physical footprint in your immediate area. If your primary bank announces a closure, you generally have 90 days of notice. Use that time to retrieve items from your safe deposit box and evaluate whether a local credit union might serve your needs better. Credit unions often maintain physical community locations long after national banks withdraw, providing the face-to-face interaction many retirees prefer when dealing with complex financial questions.

3. Stricter Social Security Direct Deposit Protocols

The era of receiving a paper Social Security check in the mail is functionally over, as the government mandated electronic payments by late 2025. Almost all retirees now receive their monthly benefits via direct deposit. However, if you decide to change banks—perhaps because your local branch closed or you found a better interest rate online—you need to navigate new fraud prevention rules implemented by the Social Security Administration (SSA).

To combat a sharp rise in account takeover fraud, the SSA has tightened its security protocols for updating banking information. In 2026, when you request a change to your direct deposit routing and account numbers, the agency may impose a mandatory waiting period of up to 30 days. This hold allows the SSA to verify your identity and ensure a scammer is not attempting to redirect your monthly check into their own account.

If you initiate this change online through your my Social Security account, the system may trigger a manual review, and you might even be required to verify your identity in person at a local SSA field office. To avoid a terrifying disruption in your cash flow, never close your old bank account as soon as you submit the change. Keep enough funds in the old account to cover automatic bill payments, and wait until your Social Security check successfully lands in the new account before shutting down the old one completely.

4. The Federal Overdraft Fee Cap Was Repealed

Overdraft fees have long been a pain point for budget-conscious consumers. In late 2024, the Consumer Financial Protection Bureau (CFPB) finalized a rule that would have capped overdraft fees at $5 for banks with more than $10 billion in assets. However, in a major shift for 2026, that federal protection is gone. The rule was officially nullified in May 2025 via a Congressional Review Act resolution signed by the president.

Because the federal cap was overturned, large financial institutions maintain the discretion to charge substantial overdraft fees, which routinely run between $25 and $35 per transaction. If a delayed deposit or an unexpected medical bill pulls your checking account below zero, your bank can legally hit you with multiple fees in a single day.

However, depending on where you live, state laws might offer some protection. For instance, California implemented a state-level cap limiting overdraft fees to $14 per occurrence for state-chartered credit unions starting January 1, 2026. Because the rules now vary wildly by institution and state, the safest approach is proactive management. Link your checking account to a savings account so that funds transfer automatically if you overdraw, or simply decline overdraft coverage altogether. By declining the coverage, a transaction that exceeds your balance will simply be declined at the register rather than processed with a hefty penalty fee attached.

5. FedNow Brings Instant Payments (and Instant Fraud Risk)

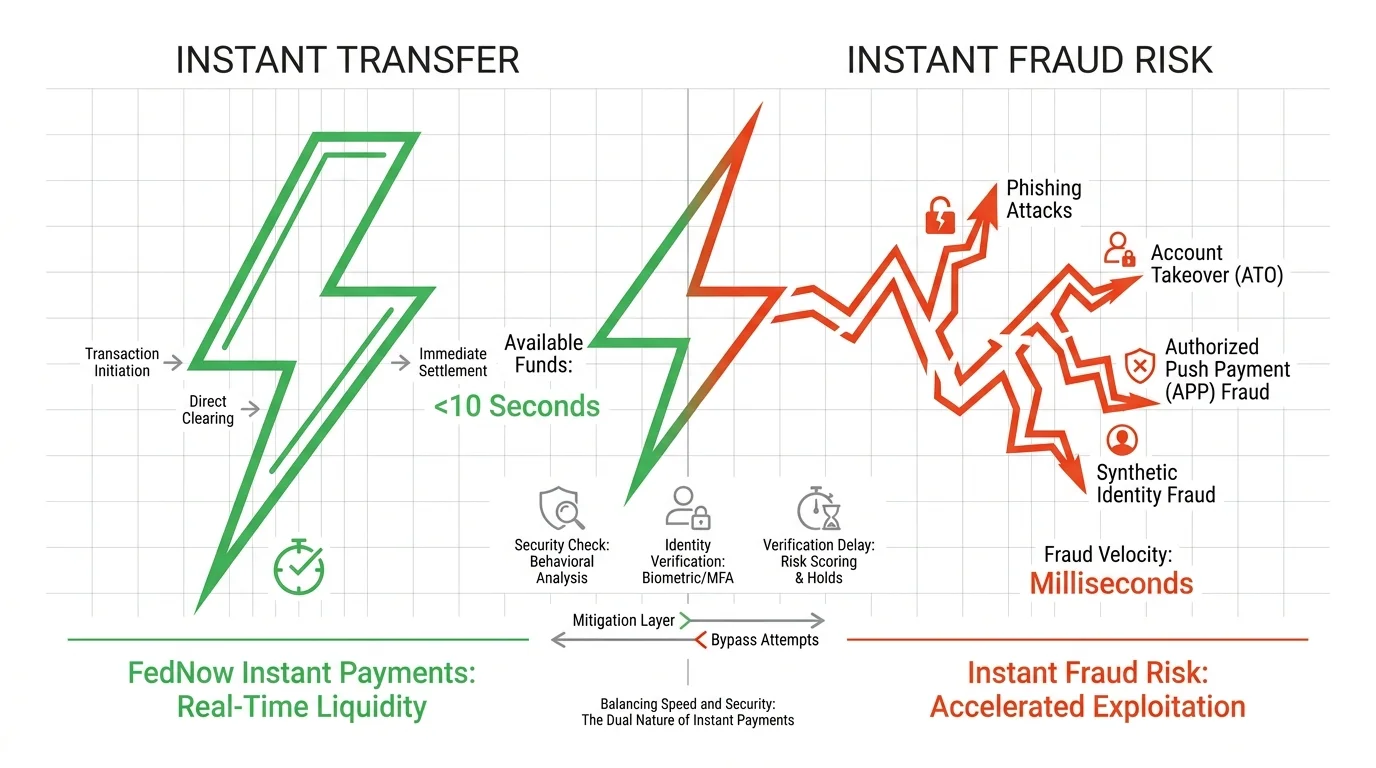

The way money moves behind the scenes is undergoing a massive upgrade. The Federal Reserve’s FedNow service, launched in 2023, has now expanded to include more than 1,500 participating financial institutions as of 2025 and 2026. Unlike traditional bank transfers that take days to clear—and pause entirely on weekends and federal holidays—FedNow settles payments instantly, 24 hours a day, 365 days a year.

For retirees, instant payments offer clear benefits. If you need to send emergency cash to a family member, or if a government agency issues a disaster relief payment, the money arrives in seconds. You no longer have to wait three business days for a check to clear before you can pay your mortgage.

But the speed of FedNow removes the traditional banking buffer that protects consumers from mistakes. In the past, if you realized you had been tricked into writing a check or initiating a transfer, you could call your bank the next morning and issue a stop-payment order. With instant payments, settlement is final the moment you hit “send.” Scammers are highly aware of this change and frequently exploit the system, demanding immediate transfers for fake emergency medical bills or IRS tax penalties. Once the money hits the scammer’s account, it is immediately withdrawn, leaving the bank with no way to pull the funds back.

6. Patchwork Reimbursement Policies for Zelle and P2P Scams

Peer-to-peer (P2P) payment apps like Zelle and Venmo have become standard tools for splitting dinner bills or paying the lawn care service. However, as fraud on these platforms skyrockets, the rules governing who takes the financial loss are shifting in 2026.

Federal law, specifically Regulation E, dictates that if a criminal hacks into your account and sends money without your permission, it is considered an “unauthorized transfer,” and your bank must generally reimburse you. But scammers have evolved. Today, they rely on “authorized push payment” (APP) scams. They impersonate a bank fraud department, a utility company, or a panicked grandchild, tricking you into logging in and authorizing the transfer yourself. Because you pressed the button, banks historically classified these as authorized transactions and refused refunds.

Under intense pressure from lawmakers, policies are slowly fracturing. While there is no universal federal law forcing banks to refund authorized scams in 2026, some networks have updated their internal rules. Zelle, for example, now requires its participating banks to reimburse victims of specific “imposter scams” where a criminal convincingly impersonates a bank employee or government official. Still, getting this money back requires filing formal disputes, navigating appeals, and dealing with lengthy investigations. The most reliable protection is behavioral: treat P2P apps exactly like physical cash. Never send money to someone you do not know personally, and never rely on caller ID to verify who is on the phone.

7. Strategic Account Structuring to Maximize FDIC Coverage

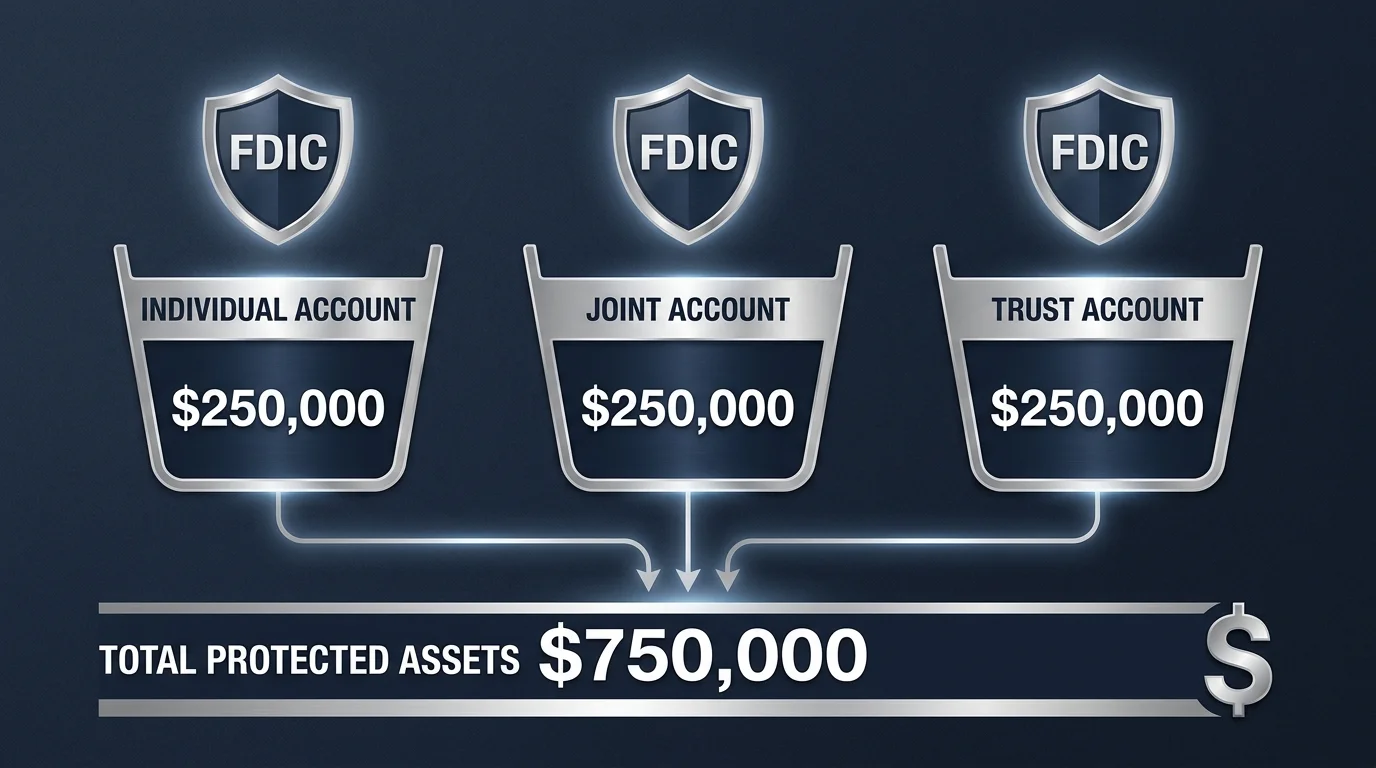

As bank consolidation accelerates and economic uncertainties persist, ensuring your life savings are fully insured by the Federal Deposit Insurance Corporation (FDIC) is a non-negotiable step. The standard insurance amount remains at $250,000 per depositor, per insured bank, for each account ownership category.

While there have been legislative proposals—such as the Main Street Depositor Protection Act—aiming to increase this cap, none have passed into law for 2026. The $250,000 threshold remains the ironclad rule. The danger for retirees lies in bank mergers. If you intentionally split $400,000 between Bank A and Bank B to keep both accounts under the $250,000 limit, and Bank A suddenly acquires Bank B, your combined balance at the new mega-bank now exceeds the insured limit. If the institution fails, the uninsured $150,000 is at risk.

You can legitimately expand your coverage beyond $250,000 at a single bank by utilizing different ownership categories. For example, an individual checking account is insured up to $250,000. A joint savings account with a spouse is insured up to $500,000 ($250,000 per co-owner). Traditional and Roth IRAs fall into a separate category, insured up to an additional $250,000. Revocable trust accounts scale based on the number of unique beneficiaries. To ensure your structuring is correct, use the FDIC’s Electronic Deposit Insurance Estimator (EDIE), which allows you to input your exact account types and confirm your coverage.

Things to Watch Out For

Even with careful planning, modern banking is full of traps designed to catch consumers off guard. Watch out for these specific scenarios:

- Testing new transfer tools with large amounts: If you are using FedNow or a new P2P app for the first time, never send a large sum right away. Send a $1 test transaction and verify with the recipient over the phone that the money arrived safely. Only then should you send the full amount.

- Trusting text messages about “locked” accounts: Scammers routinely send fake text alerts claiming your account has been frozen due to suspicious activity, providing a link to “unlock” it. Do not tap the link. Close the message, look at the back of your debit card, and dial the customer service number printed there.

- Ignoring mailed notices about your bank accounts: Banks are required to send written notices regarding branch closures, fee schedule changes, and updates to their terms of service. Tossing these envelopes into the recycling bin unread can lead to unexpected monthly maintenance fees or a sudden loss of local access.

- Closing an old checking account prematurely: When switching banks, do not close your old account until all outstanding checks have cleared and at least two billing cycles of automated payments have successfully transitioned to the new account. A bounced payment can trigger late fees and damage your credit score.

When DIY Isn’t Enough

While most everyday banking tasks are manageable on your own, certain situations require the expertise of a licensed professional. Consider seeking outside help if you face the following:

- Structuring large sums of cash across multiple trusts: If you recently sold a home or business and have liquid assets far exceeding FDIC limits, a certified financial planner or estate attorney can help you structure revocable trusts or utilize sweep networks to ensure every dollar is insured.

- Managing the financial transition of a deceased spouse: When a spouse passes away, bank accounts, pensions, and Social Security benefits must be carefully untangled and retitled. A professional can guide you through the probate process and prevent you from accidentally triggering tax liabilities.

- Recovering from significant financial fraud: If a scammer successfully drains your retirement accounts and the bank denies your reimbursement claim, you may need a consumer protection attorney to formally escalate the dispute and pursue legal remedies under the Electronic Fund Transfer Act.

Frequently Asked Questions

Will my Social Security check stop if my local bank branch closes?

No. Your Social Security direct deposit is tied to your account’s electronic routing and account numbers, not the physical building. As long as the bank itself remains in business, your deposits will continue seamlessly.

Are digital-only banks safe for my retirement savings?

Yes, provided they are FDIC-insured. Digital banks often offer higher CD and savings yields because they do not have the overhead costs of maintaining physical branches. Always verify their FDIC membership by looking for the FDIC logo on their website or searching the agency’s official database.

What is the difference between Zelle and FedNow?

Zelle is a private peer-to-peer app owned by a consortium of large banks, primarily used by consumers to send money to friends and family. FedNow is a payment infrastructure operated directly by the Federal Reserve, used by banks behind the scenes to clear payments, payroll, and transfers instantly.

How do I know if my bank is federally insured?

You can look for the official FDIC sign at physical branches or the logo on the bank’s homepage. For absolute certainty, use the BankFind tool on the official FDIC website to search for your institution’s specific legal name.

Final Thoughts

The banking changes of 2026 reward those who pay attention. By securing high CD yields while they last, adapting to stricter federal deposit rules, and treating instant digital payments with the utmost caution, you can protect your cash from inflation, fees, and fraud. Take an hour this week to log into your accounts, review your overdraft settings, and run your balances through the FDIC estimator. A few proactive adjustments today will grant you profound peace of mind tomorrow.

Last updated: May 2026. Rules, prices, and details change—verify current information with official sources before acting on it.

This article provides general information only. Every reader’s situation is different—what works for others may not be the right fit for you. For personalized guidance on health, legal, or financial matters, consult a qualified professional.