When the Federal Reserve adjusts interest rates, the ripple effect directly hits your retirement accounts and savings yields. If you are tracking your nest egg, understanding what rising interest rates mean for your retirement savings is critical. For years, savers navigated an environment where cash earned almost nothing and growth meant taking on significant stock market risk. Higher rates change that math completely. Suddenly, conservative investments like certificates of deposit, money market accounts, and bonds offer real returns, giving retirees a safer way to generate income. However, these rate hikes can also drag down certain stock prices and make carrying debt more expensive. Here is how to optimize your strategy when rates climb.

The Shift to a Higher for Longer Environment

The Federal Open Market Committee frequently meets to assess economic conditions, functioning as the thermostat for the United States economy. When inflation runs hot, the Federal Reserve raises the target range for the federal funds rate—the baseline interest rate that banks charge each other for overnight loans. While this rate does not directly set consumer rates, it acts as the foundation for the entire financial system. When the federal funds rate goes up, borrowing costs across the economy increase, which is designed to cool down consumer spending and business expansion.

In recent years, the market has transitioned out of the era of essentially free money. During the early 2020s, borrowing was historically cheap, driving up housing prices and stock valuations. Today, the economy has shifted into a higher-rate environment aimed at maintaining long-term price stability. While financial news usa headlines often focus on the negative impacts of rate hikes—such as expensive mortgages and slowing corporate growth—the narrative for retirees is entirely different. For budget-conscious Americans managing their retirement money, higher rates represent the return of safe yield. You no longer have to rely solely on the volatile stock market to generate the income needed to cover your daily living expenses.

How Rising Rates Boost Your Safe Investments

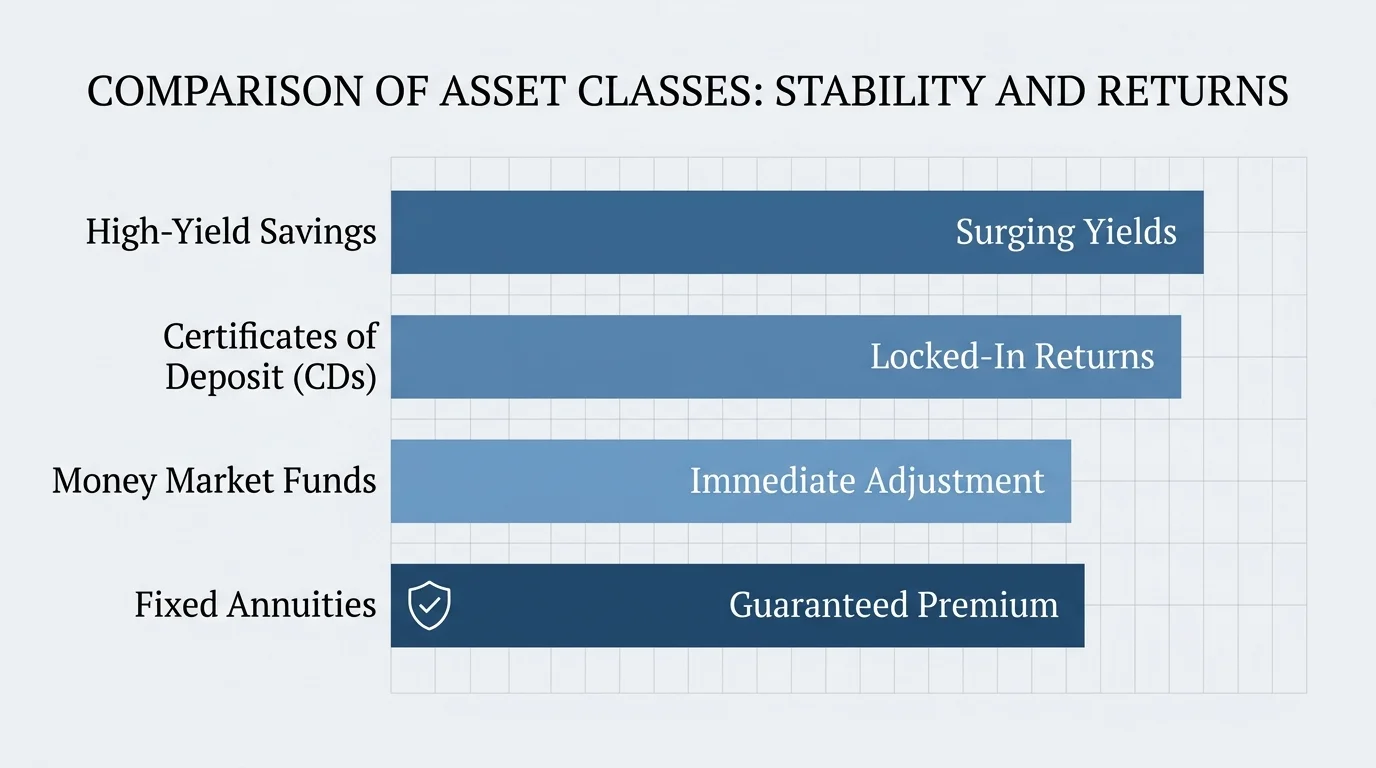

When interest rates climb, the biggest winners are conservative savers. Financial institutions must compete harder for your deposits, which means they are willing to pay you more for the privilege of holding your cash. If you know where to look, you can significantly increase the cash flow of your portfolio without taking on additional market risk. When evaluating interest rates, retirement planners should focus on three specific assets.

- High-Yield Savings Accounts and Certificates of Deposit: Traditional brick-and-mortar banks are notoriously slow to raise the interest rates they pay on standard checking and savings accounts. However, online banks and credit unions adjust their rates quickly to attract new customers. Data from the Federal Deposit Insurance Corporation (FDIC) consistently shows that national rate caps and average yields for certificates of deposit (CDs) surge during rate-hike cycles. By moving your emergency fund into a high-yield savings account or locking in a CD, you can turn stagnant cash into a reliable income stream.

- Money Market Funds: Not to be confused with money market deposit accounts at a retail bank, money market funds are offered by brokerage firms. These funds invest in ultra-short-term government debt, such as Treasury bills. Because the underlying debt matures in a matter of days or weeks, the yield on a money market fund adjusts almost immediately when the Federal Reserve raises rates. This makes them an excellent holding pen for your cash, offering total liquidity alongside highly competitive yields.

- Fixed Annuities: An annuity is essentially a contract between you and an insurance company. You provide a premium, and the insurer promises you a steady payout. Insurance companies take your premium and invest it heavily in corporate and government bonds. When interest rates are high, the insurer earns more on those underlying bonds and can subsequently offer much higher guaranteed payout rates to new annuity buyers. For retirees looking to lock in a guaranteed monthly paycheck for life, a high-rate environment offers excellent pricing.

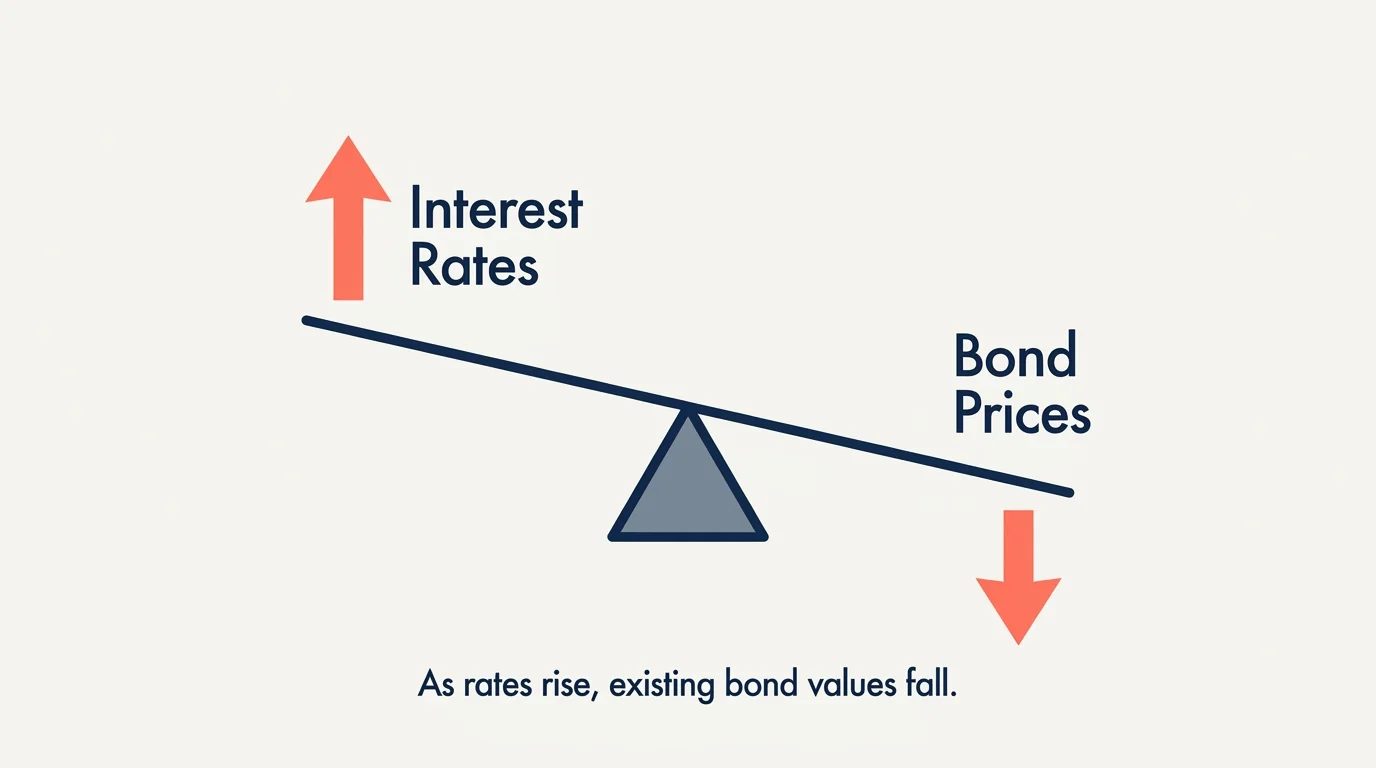

The Hidden Risk to Existing Bonds

While higher rates are fantastic for new cash, they present a hidden danger to the bonds you already own. Bonds are traditionally viewed as the safe anchor of a retirement portfolio, but they are not immune to market forces.

According to the U.S. Securities and Exchange Commission (SEC), market interest rates and bond prices generally move in opposite directions—a dynamic known as interest rate risk. To understand why this happens, imagine a seesaw. If you buy a 10-year Treasury bond paying a 2 percent yield, and the Federal Reserve subsequently raises rates so that new 10-year Treasury bonds pay 4 percent, your older bond becomes far less attractive to investors. If you need to sell your 2 percent bond on the secondary market before it matures, nobody will buy it at full price; you must sell it at a discount so the buyer achieves an effective 4 percent yield.

This dynamic explains why your bond mutual funds lose value when rates rise. Unlike individual bonds—which guarantee the return of your principal if you hold them to their exact maturity date—bond mutual funds constantly buy and sell bonds of varying maturities. When rates spike, the net asset value of the fund drops, resulting in a paper loss on your brokerage statement. However, if you hold the fund over time, the portfolio managers will continually replace the older bonds with new, higher-yielding ones, eventually restoring your portfolio’s value through larger monthly dividend distributions.

What Rising Interest Rates Mean for the Stock Market

For decades, retirees have relied on a traditional mix of stocks and bonds to provide both growth and income. When interest rates rise, the stock portion of your portfolio faces distinct challenges, depending heavily on the types of companies you own.

Higher borrowing costs directly impact corporate balance sheets. When loans are expensive, companies are less likely to finance new factories, hire aggressively, or buy back their own stock. This slowing expansion often leads to lower earnings reports, triggering stock market sell-offs.

Growth stocks—particularly technology companies—tend to suffer the most during rate hikes. The valuation of a growth company is largely based on its projected future earnings. When interest rates rise, investors discount the value of those future earnings because they can get a guaranteed, risk-free return right now in the bond market. If a safe Treasury bill pays 5 percent, investors demand a significantly higher potential return to justify taking a risk on a volatile tech startup.

Conversely, value stocks and dividend-paying companies often weather the storm more effectively. Businesses that generate strong, consistent cash flow today—such as utility providers, consumer staples, and healthcare companies—become more attractive to older investors seeking stability. Financial institutions, particularly banks, can even benefit from rising rates by widening their net interest margin, which is the profitable difference between the interest they charge on loans and the interest they pay out on deposits.

Comparing Asset Performance in a Rising Rate Environment

To simplify how these moving parts affect your overall net worth, here is a breakdown of how common asset classes generally react when benchmark interest rates climb.

| Asset Class | Impact of Rising Rates | The Underlying Reason |

|---|---|---|

| New CDs & High-Yield Savings | Positive (Higher Yields) | Banks and credit unions must offer higher APYs to compete for your deposits as benchmark rates rise. |

| Existing Fixed-Rate Bonds | Negative (Price Drop) | Older bonds paying lower interest lose resale value compared to newly issued, higher-yielding bonds. |

| New Fixed Annuities | Positive (Higher Payouts) | Insurance companies earn more on their bond investments and pass those higher payout rates to new buyers. |

| Growth Stocks | Negative (Valuation Drop) | Higher borrowing costs stunt corporate expansion, making projected future profits less appealing. |

| Variable-Rate Debt (HELOCs, Credit Cards) | Negative (Costs More) | Lenders automatically adjust your interest rate upward based on the prime rate, increasing your monthly payment. |

Debt and the Retirement Equation: What Can Go Wrong

When assessing your savings impact, it is crucial to examine the liability side of your balance sheet. Rising interest rates can easily derail a carefully constructed retirement plan if you fall into a few common traps.

- Carrying variable-rate debt into retirement: Credit cards and Home Equity Lines of Credit (HELOCs) are almost always tied to the prime rate. When the Federal Reserve hikes rates, your credit card APR increases immediately. If you carry a revolving balance, the extra interest charges will quickly devour your fixed monthly income. Paying off variable-rate debt should be an immediate priority before leaving the workforce.

- Panic-selling bond mutual funds: Seeing the value of your bond portfolio drop can trigger an emotional response. If you sell your bond funds during a rate hike, you permanently lock in your capital losses. If you remain patient, the fund will eventually cycle into higher-yielding bonds, repairing the temporary damage through larger dividend payouts.

- Locking up too much cash in long-term CDs: Securing a 5-year CD might seem brilliant today, but if inflation spikes and rates climb even higher, your money is trapped earning a sub-par return. If you withdraw early to chase a better rate, the bank will hit you with penalty fees that wipe out your interest. To prevent this, consider CD laddering—buying multiple CDs with staggered maturity dates so you always have cash freeing up.

- Misunderstanding complex annuity contracts: Because higher rates make fixed annuities more attractive, some salespeople use the environment to aggressively push variable or indexed annuities. The Financial Industry Regulatory Authority (FINRA) actively monitors the industry for unsuitable annuity exchanges, noting that high fees and surrender charges often harm the consumer. Always read the fine print and understand the market risks before signing an annuity contract.

What This Means for You

For the better part of two decades, retirees faced a brutal reality: safe investments paid practically nothing. To generate enough income to survive, everyday Americans were forced to take on significant stock market risk, hoping the market would not crash the year they decided to retire.

The return of higher interest rates flips this dynamic back in favor of the cautious saver. You can now build a portfolio that generates a meaningful yield using a combination of government bonds, high-yield savings accounts, and fixed annuities without risking your principal in the stock market. This allows you to protect your nest egg from market volatility while still outpacing baseline inflation.

However, this financial safety requires your active participation. If you leave your retirement money sitting in a traditional checking account at a massive national bank, you will earn next to nothing. Large institutions rarely pass higher rates onto their existing customers automatically. You must actively move your cash into competitive high-yield accounts, money market funds, or staggered CDs to reap the rewards of the current economy updates.

Where Outside Advice Pays Off

Not every financial move requires a professional, but navigating the crosscurrents of interest rates, inflation, and tax laws can get complicated quickly. Consider seeking out a fiduciary financial advisor in these specific situations:

- Evaluating complex annuity contracts: Annuities are dense legal documents filled with hidden fees, riders, and surrender charges. A fee-only advisor can calculate whether a Single Premium Immediate Annuity genuinely improves your retirement income plan or if the internal costs outweigh the guaranteed benefits.

- Executing tax-efficient portfolio shifts: Selling off stock market gains to buy newly issued, higher-yielding bonds will trigger capital gains taxes. A professional can help you execute these trades inside tax-advantaged accounts—like an IRA or a 401(k)—to shield your wealth from the IRS.

- Managing bond fund duration: If you rely heavily on bond mutual funds for your monthly living expenses, an advisor can analyze the average duration of your funds. They will ensure your bond holdings align with your withdrawal timeline, reducing the chance of a sudden portfolio drop right when you need the cash most.

Frequently Asked Questions

Do rising interest rates hurt 401(k) accounts?

They can cause short-term fluctuations. Because a typical target-date 401(k) holds a mix of stocks and bond funds, a rate hike can temporarily depress both sides of your portfolio. Over the long term, however, the bond portion will begin generating higher dividend yields, which compounds your growth and provides more stable income later in retirement.

Should I wait for interest rates to peak before buying a CD?

Trying to time the exact peak of the interest rate market is impossible, even for Wall Street professionals. Instead of waiting, consider building a CD ladder. By dividing your cash into multiple CDs with staggered maturity dates—such as one, two, and three years—you ensure that some of your money is consistently freeing up to capture higher rates if they continue to rise.

Why do my existing bond funds lose money when rates go up?

Existing bonds were issued with a specific, fixed payout. When new bonds hit the market offering a higher payout, no investor wants to buy the older, lower-paying bonds at full price. The resale value of your old bonds drops, which drags down the overall net asset value of the bond mutual fund holding them.

As you plan for your future, remember that the economy operates in cycles. Interest rates will rise, fall, and stabilize over time based on broader economic forces. By understanding how these financial levers work, you can confidently shift your strategy to protect your nest egg and capture the best available returns, regardless of the economic climate. This is general informational content based on widely accepted guidance. Individual results vary. Verify current details—rules, prices, eligibility, regulations—with official sources before making important decisions.

Last updated: May 2026. Rules, prices, and details change—verify current information with official sources before acting on it.