Retirement planning often tricks you into believing that avoiding risk guarantees financial security. The truth is that playing it completely safe can quietly sabotage your future by exposing you to inflation, massive tax bills, and out-of-pocket medical costs. Moving your entire portfolio to cash might protect you from stock market crashes, but it practically guarantees your purchasing power will shrink over a twenty-year retirement. Similarly, claiming Social Security as early as possible or assuming Medicare covers all health needs feels reassuring in the moment, yet these choices often lead to severe cash flow shortages later in life. Protecting your nest egg requires understanding the hidden costs behind the most common, seemingly harmless money moves.

1. Fleeing the Stock Market for the Comfort of Cash

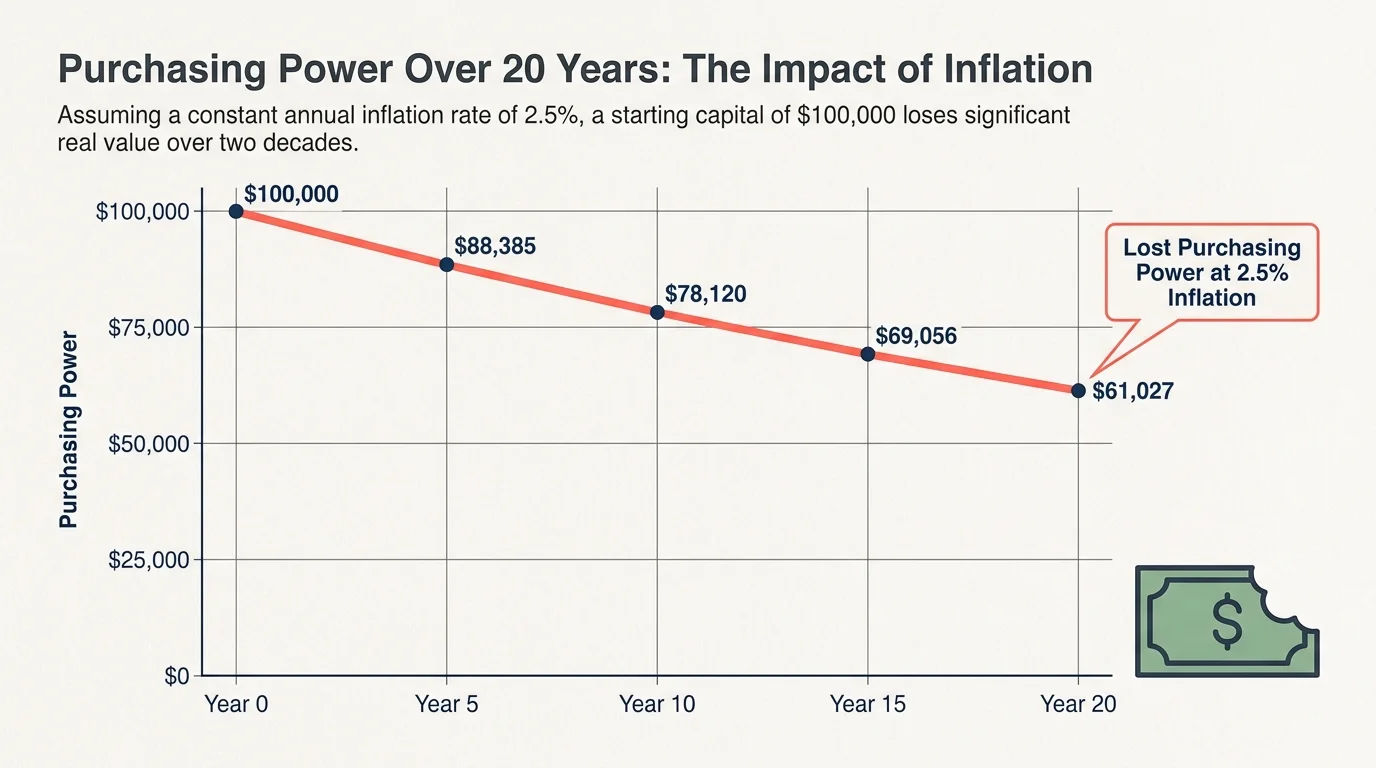

When the stock market turns volatile, selling off your equities and moving everything into high-yield savings accounts or certificates of deposit feels like the ultimate defensive move. You eliminate the daily anxiety of watching your portfolio value bounce up and down, and your principal appears perfectly secure on paper. However, while cash protects you from sudden market downturns, it heavily exposes you to inflation risk—a slow, invisible drain on your wealth.

Historical data from the Bureau of Labor Statistics shows that the United States inflation rate averaged roughly 2.5 percent annually over the past two decades, with periods of much steeper increases. Even at a modest 2.5 percent inflation rate, a hundred thousand dollars sitting in a perfectly safe bank account will lose a substantial portion of its purchasing power over a twenty-year retirement. Groceries, utilities, and property taxes will steadily rise, but your cash stack will not grow fast enough to keep up. To preserve your standard of living, you must maintain a balanced portfolio that includes equities designed to outpace inflation, rather than retreating entirely to cash.

2. Claiming Social Security at 62 to “Lock It In”

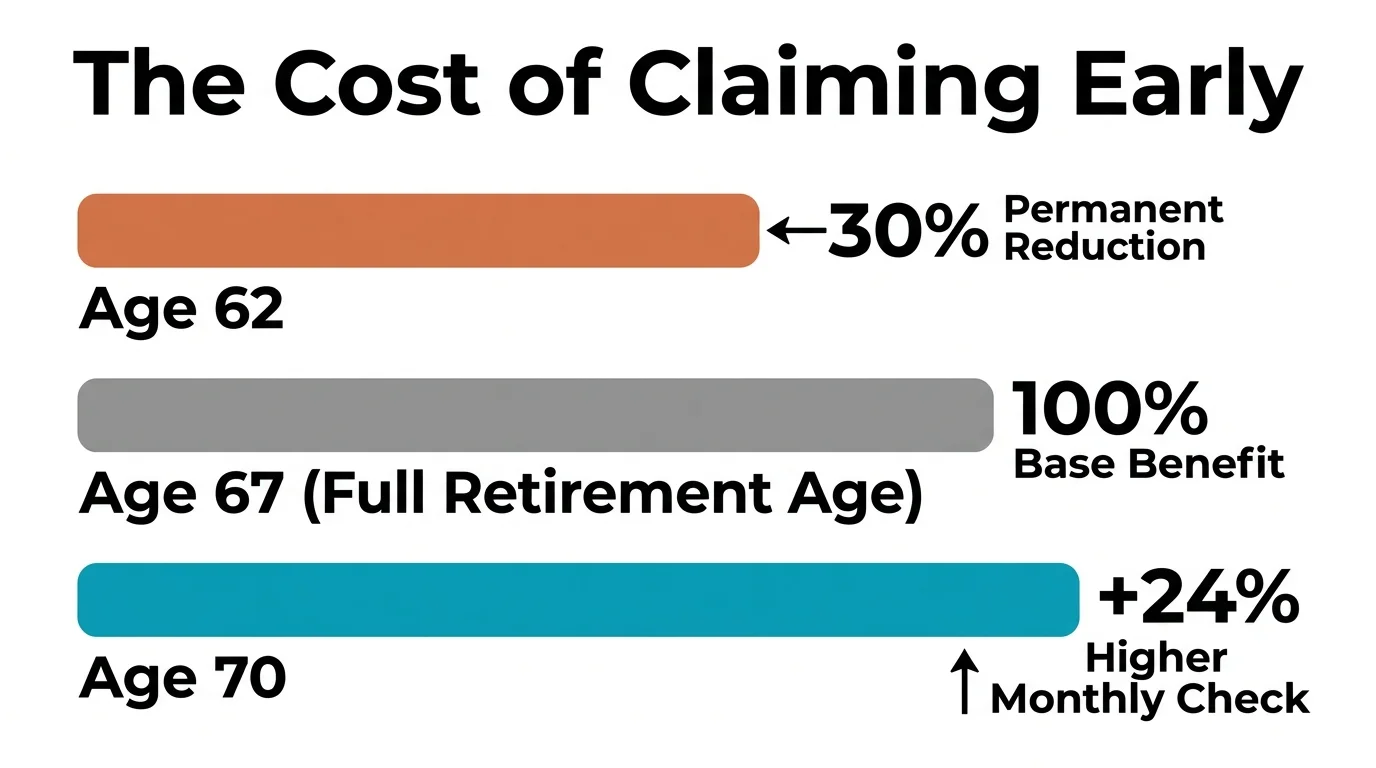

The temptation to claim Social Security benefits as soon as you reach age 62 is remarkably strong. Taking the money early feels like a guaranteed win; you lock in an income stream and start recouping the taxes you paid into the system for decades. Unfortunately, the math behind early claiming severely penalizes your lifetime earning potential.

If you were born in 1960 or later, your Full Retirement Age (FRA) is 67. According to Charles Schwab, taking benefits at age 62 permanently reduces your monthly check by 30 percent compared to waiting for your FRA. Conversely, waiting past your FRA earns you delayed retirement credits, increasing your base benefit by 8 percent for every year you delay up to age 70. This means claiming at 70 instead of 67 yields a 24 percent higher monthly check for the rest of your life. Unless you have severe health issues or face an immediate financial crisis, rushing to claim Social Security early often leaves hundreds of thousands of dollars on the table over a long retirement.

3. Draining Retirement Accounts to Pay Off a Low-Interest Mortgage

Entering retirement without a mortgage is a common American dream. The psychological relief of being completely debt-free leads many new retirees to withdraw a massive lump sum from their 401(k) or Traditional IRA to pay off their remaining home balance. While eliminating a monthly payment feels secure, doing so through a massive taxable withdrawal is often a mathematical disaster.

Withdrawals from pre-tax retirement accounts are treated as ordinary income by the IRS. Pulling out eighty thousand dollars to kill your mortgage will instantly inflate your taxable income for the year, potentially pushing you into a higher tax bracket and subjecting you to capital gains taxes on other investments. Furthermore, you lose the compound growth that money could have earned if left invested. If your mortgage carries an interest rate of 3 or 4 percent, and your retirement portfolio historically earns 6 or 7 percent, liquidating your investments to pay off the debt actually damages your net worth. It is usually far safer to maintain the low-interest mortgage and pay it off slowly using your regular monthly cash flow.

4. Skipping Medigap or Choosing the Cheapest Medicare Advantage Plan

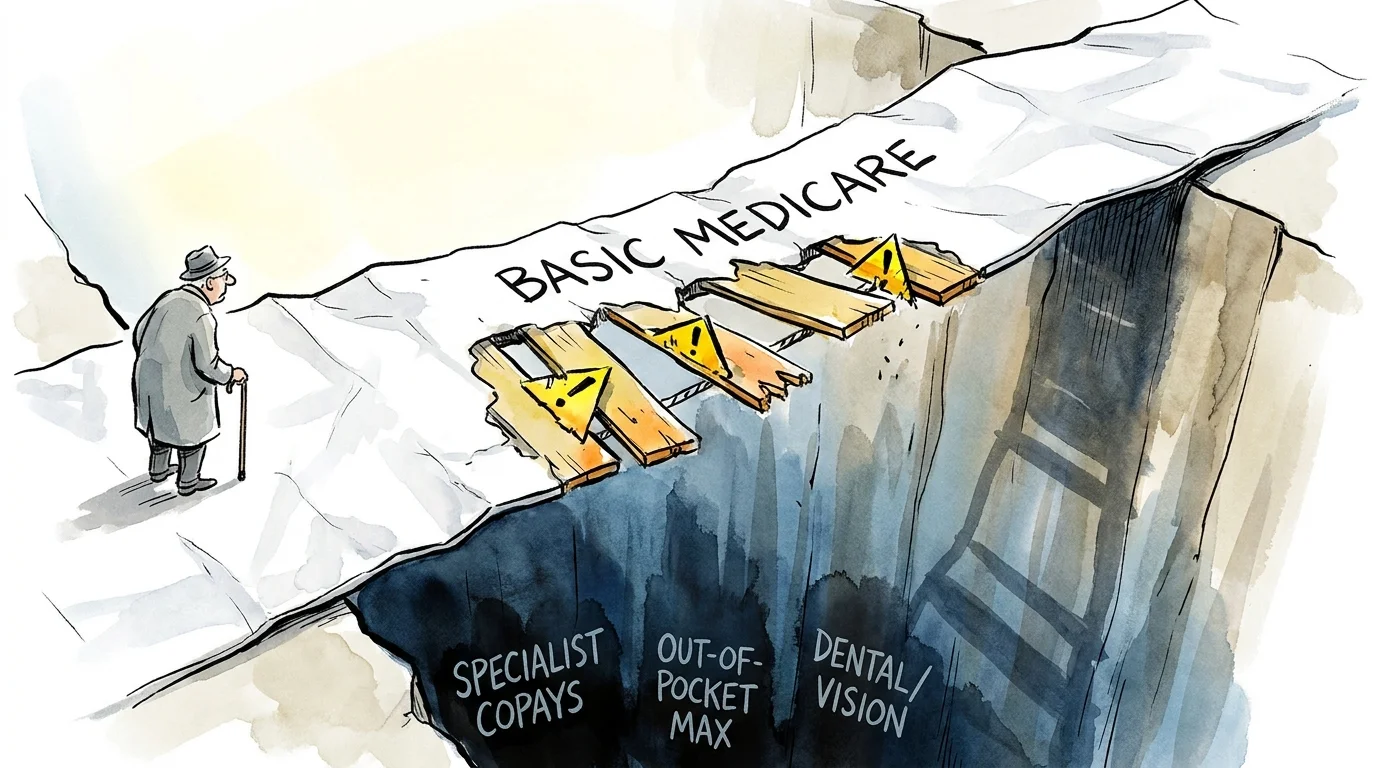

Healthcare costs represent one of the largest expenses in retirement, yet many retirees assume the basic Medicare coverage they receive at age 65 will handle everything. Original Medicare (Parts A and B) covers hospital stays and outpatient care, but Part B carries a 20 percent coinsurance requirement with absolutely no annual out-of-pocket maximum. If you face a severe illness or require expensive ongoing treatments, that 20 percent share could quickly bankrupt you.

To cap their liability, retirees choose between buying a supplemental Medigap policy or enrolling in a Medicare Advantage (Part C) plan. While Medicare Advantage plans often advertise zero-dollar monthly premiums, they come with network restrictions and variable out-of-pocket limits. Medicare Interactive notes that the federal out-of-pocket maximum for Medicare Advantage plans in 2026 is $9,250 for in-network services. Choosing the absolute cheapest health plan upfront feels like a smart budgeting move until a serious medical event exposes you to nearly ten thousand dollars in unexpected bills.

| Medicare Plan Structure | Out-of-Pocket Maximum | Network Restrictions |

|---|---|---|

| Original Medicare (Parts A & B) | None. You are responsible for 20% of Part B costs indefinitely. | None. You can see any provider nationwide that accepts Medicare. |

| Medicare Advantage (Part C) | Capped at $9,250 for in-network services in 2026. | Usually requires using a local HMO or PPO provider network. |

| Original Medicare + Medigap | Varies by plan, but covers most traditional gaps and coinsurance. | None. You can see any provider nationwide that accepts Medicare. |

1. A

2. worried

3. mother

4. reviews

5. past

6. due

7. bills

8

5. Bankrolling Adult Children Before Securing Your Own Solvency

Helping your children buy their first home, pay off student loans, or fund a wedding feels like the right thing to do. Many retirees prioritize their family’s financial ease over their own, assuming they can simply cut back on lifestyle expenses if funds get tight later. However, giving away your capital reduces the principal balance generating your retirement income, permanently shrinking your financial safety net.

You can always borrow money for a house, a car, or an education, but no bank will issue you a loan to fund your retirement. If bankrolling your adult children forces you to deplete your savings faster than planned, you may eventually become a financial burden to those same children when you require care later in life. Securing your own solvency first is not selfish; it is the most practical way to ensure you never have to depend on your family for basic living expenses.

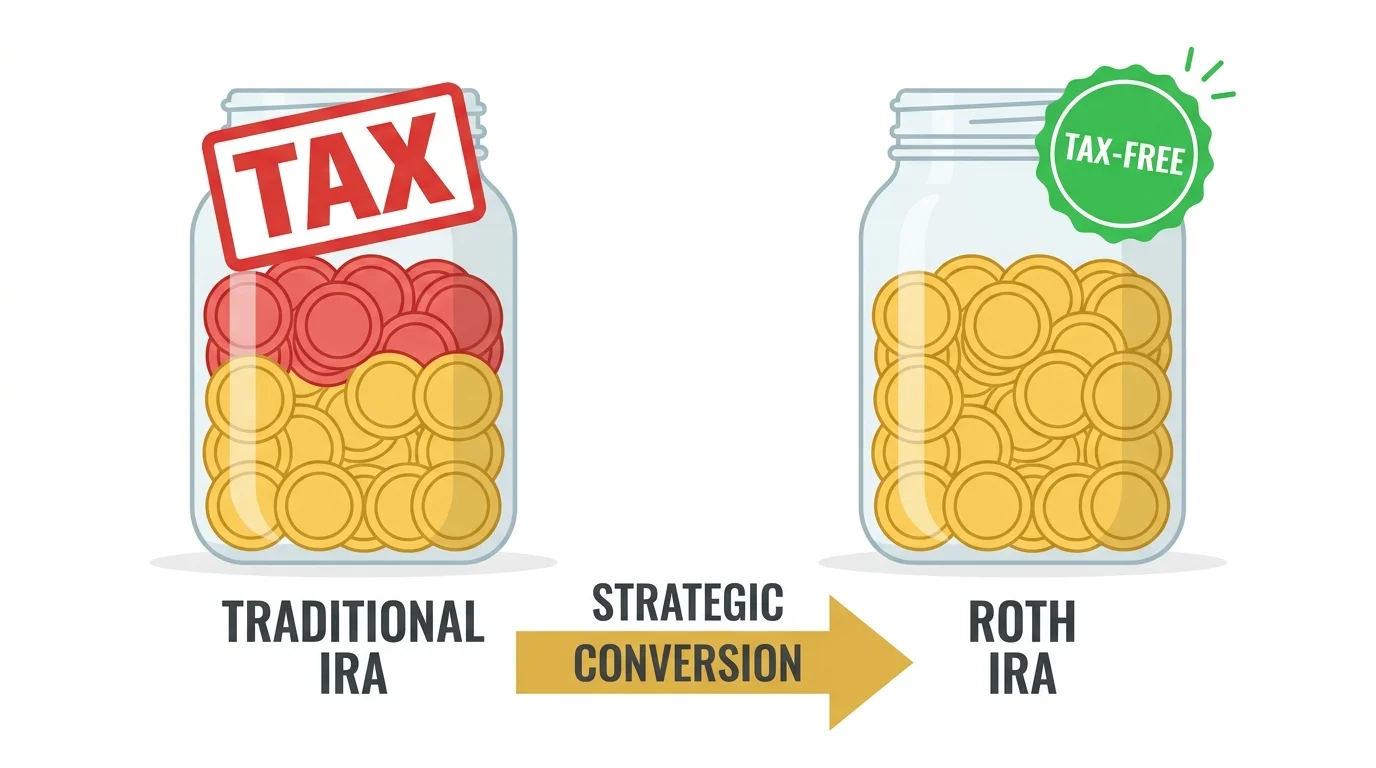

6. Hoarding Pre-Tax Accounts and Ignoring Roth Conversions

Watching your Traditional IRA or 401(k) grow tax-deferred for decades feels incredibly satisfying. Deferring taxes is a sound strategy during your high-earning working years, but hoarding those pre-tax accounts in retirement creates a ticking tax time bomb. The IRS will eventually force you to start withdrawing from these accounts through Required Minimum Distributions (RMDs), currently mandated to begin at age 73.

When RMDs kick in, you must withdraw a percentage of your account balance every year, whether you need the money or not. This forced withdrawal is taxed as ordinary income. A sudden spike in taxable income can push you into a higher marginal tax bracket and trigger the Income-Related Monthly Adjustment Amount (IRMAA), which substantially increases your Medicare Part B and Part D premiums. Strategically converting portions of your pre-tax money into a Roth IRA during early retirement—when your income is naturally lower—requires paying some taxes voluntarily now, but it shields you from massive, forced tax bills later.

7. Avoiding All Annuities Due to Their Negative Reputation

Annuities have earned a controversial reputation in the financial world, largely due to complex variable annuities loaded with high fees, surrender charges, and aggressive sales commissions. Because of this, many self-directed retirees swear off annuities entirely, assuming they are always a bad investment. This blanket avoidance limits your options for creating a guaranteed income floor.

While complex annuities are often flawed, a basic Single Premium Immediate Annuity (SPIA) operates very differently. With an SPIA, you hand an insurance company a lump sum of cash in exchange for a guaranteed monthly paycheck for the rest of your life. It acts as a personal pension, directly solving the risk of outliving your money. If you lack a traditional corporate pension and worry that market volatility will wipe out your savings, dedicating a portion of your portfolio to a low-cost, fixed annuity provides absolute certainty that you will receive a check every single month.

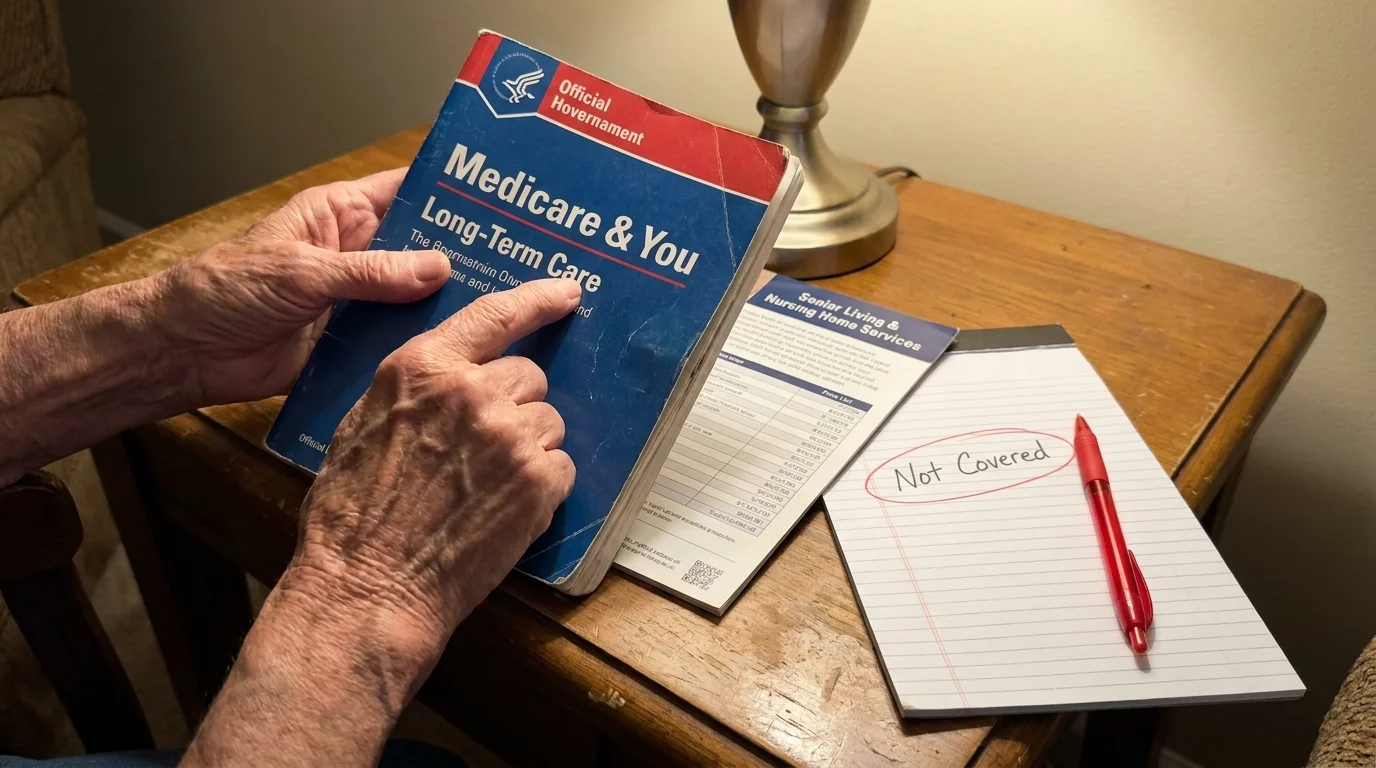

8. Assuming Medicare Will Cover Long-Term Care

The assumption that Medicare will pay for a nursing home or an in-home health aide is one of the most widespread and devastating misconceptions in retirement planning. Medicare is specifically designed to cover acute, medically necessary care. It will pay for a temporary stay in a skilled nursing facility—typically up to 100 days—following a qualifying hospital admission, but it outright rejects coverage for long-term custodial care, such as help with bathing, dressing, and eating.

If you develop severe dementia or experience general physical decline, you must pay for that ongoing care out of your own pocket until your assets are nearly depleted, at which point Medicaid may step in. The costs are staggering. The latest Cost of Care Survey from CareScout and Genworth reveals that the national median daily rate for a private room in a nursing home totals roughly $129,575 annually. Failing to plan for these expenses—either through long-term care insurance, hybrid life insurance policies, or earmarked savings—can completely wipe out a lifetime of careful wealth accumulation in a matter of years.

Things to Watch Out For

Even if you avoid the major pitfalls above, retirement planning is a moving target. Be mindful of these secondary risks that can disrupt a solid financial foundation:

- The Provisional Income Threshold for Social Security: Your Social Security benefits are not entirely tax-free. If your combined income (adjusted gross income plus non-taxable interest plus half of your Social Security benefits) exceeds certain thresholds, up to 85 percent of your benefits become subject to federal income tax.

- Premium Creep on Health Insurance: Medigap policies and Medicare Advantage plans are not price-locked. Insurance carriers routinely raise premiums as you age and as healthcare costs inflate. You must budget for these regular increases rather than assuming your healthcare costs will remain flat.

- Sequence of Returns Risk: Experiencing a severe market crash during the first few years of your retirement is vastly more damaging than a crash occurring twenty years later. Withdrawing funds from a shrinking portfolio compounds your losses, making it nearly impossible for the principal to recover when the market eventually rebounds.

When DIY Isn’t Enough

Personal finance relies heavily on basic math and discipline, but specific retirement transitions involve complex legal and tax codes. Attempting to handle the following scenarios on your own can lead to costly errors:

- Executing a Multi-Year Roth Conversion Strategy: Calculating exactly how much to convert from a Traditional IRA to a Roth IRA without crossing into a higher tax bracket or triggering Medicare IRMAA surcharges requires precise tax modeling.

- Coordinating Spousal Benefits: Deciding when each spouse should claim Social Security involves variables like age gaps, differing lifetime earnings, and survivor benefits. An error here permanently limits the surviving spouse’s income.

- Structuring a Medicaid Spend-Down: If you are facing imminent long-term care needs and need to qualify for Medicaid without impoverishing a healthy spouse, you must navigate strict five-year lookback rules. A mistake in transferring assets can result in severe coverage penalties.

Frequently Asked Questions

Does Medicare pay for assisted living facilities?

No. Medicare covers medically necessary acute care, such as hospital surgeries, doctor visits, and brief rehabilitation stays in skilled nursing facilities. It does not pay for room and board at an assisted living facility or for long-term custodial care.

What is the financial penalty for claiming Social Security at age 62?

If your full retirement age is 67, claiming benefits at age 62 results in a permanent 30 percent reduction to your monthly check. Furthermore, you forfeit the delayed retirement credits that would have increased your base benefit by 8 percent for every year you delay past age 67.

Why are Required Minimum Distributions (RMDs) considered a tax risk?

RMDs compel you to withdraw a specific percentage of your pre-tax retirement accounts every year starting at age 73. Because the IRS taxes these withdrawals as ordinary income, they can artificially inflate your tax bracket, trigger taxes on your Social Security benefits, and increase your Medicare premiums.

Taking control of your retirement means looking beyond the choices that simply feel comfortable in the moment. By understanding how taxes, inflation, and healthcare costs interact with your savings, you can build a strategy that protects your wealth for decades to come. This article provides general information only. Every reader’s situation is different—what works for others may not be the right fit for you. For personalized guidance on health, legal, or financial matters, consult a qualified professional.

Last updated: May 2026. Rules, prices, and details change—verify current information with official sources before acting on it.