Deciding when and how to claim Social Security is one of the most critical financial choices you will make, and being married adds entirely new layers to the math. Spousal and survivor benefits offer powerful ways to maximize your household income, but strict age limits, earnings caps, and hidden deadlines can easily derail your retirement if you miscalculate. You cannot afford to guess how these rules apply to your unique timeline.

Whether you are coordinating a dual-income retirement or planning for a spouse who stayed home, understanding exactly how the Social Security Administration views your marriage ensures you capture every dollar you have earned. Here is exactly how the rules work for couples navigating the system today.

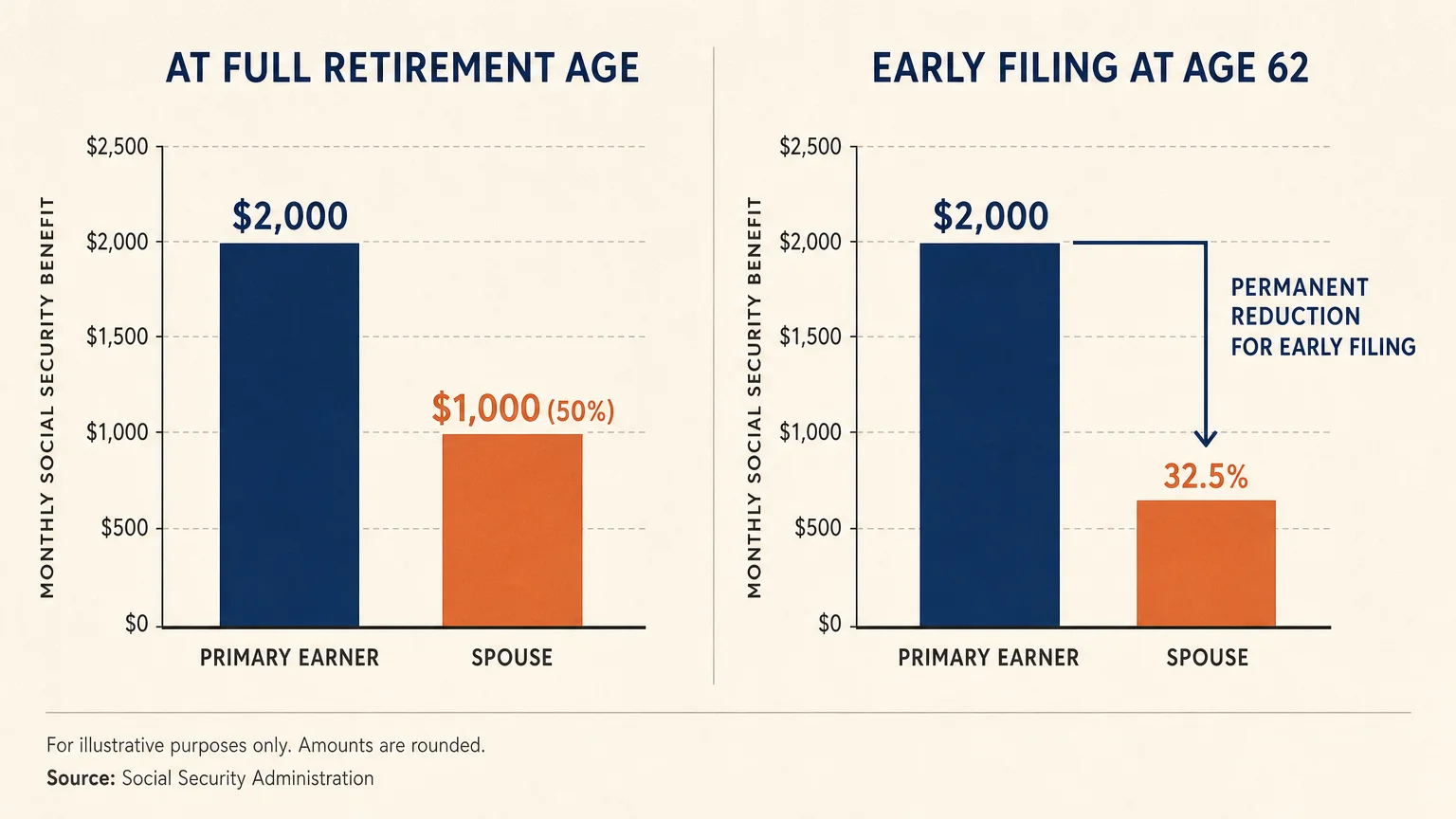

The Mechanics of Spousal Benefits

1. Spousal benefits cap at 50% of the worker’s primary insurance amount

The absolute maximum a spouse can receive on their partner’s work record is 50% of the primary earner’s full retirement age benefit. If your spouse’s full benefit is $2,000 a month, your maximum spousal benefit is $1,000. Claiming this spousal benefit does not reduce the primary earner’s check. However, to get that full 50%, you must wait until your own full retirement age to file. If you claim the spousal benefit early—as early as age 62—the Social Security Administration permanently reduces your percentage. For instance, claiming at 62 could reduce your spousal benefit to as little as 32.5% of the primary earner’s amount.

2. You cannot claim a spousal benefit until your partner actually files

You cannot receive a spousal benefit while your partner continues to defer their own retirement application. Even if you reach your full retirement age, the Social Security Administration will not pay you a spousal benefit until the primary earner officially files for their benefits. This rule requires strategic coordination. If the higher earner plans to delay claiming until age 70 to maximize their payout, the lower earner must also wait to access spousal benefits, though they can still claim their own individual benefit in the meantime if they qualify.

3. Waiting past full retirement age does not increase a spousal benefit

Workers who delay claiming their own retirement benefits past their full retirement age earn delayed retirement credits, boosting their payout by 8% per year up to age 70. Spousal benefits do not work this way. A spousal benefit maxes out at the claimant’s full retirement age. Waiting until age 68, 69, or 70 to claim a spousal benefit provides no financial advantage whatsoever. If your strategy relies primarily on spousal benefits, delaying past your full retirement age only means you forfeit months of checks.

4. The dual entitlement rule pays your own earned benefit first

You cannot double-dip by collecting your full individual benefit plus a full spousal benefit. Under the dual entitlement rule, the Social Security Administration always pays out your own earned benefit first. If your earned benefit is lower than your spousal benefit, the agency adds a supplemental amount to bring your total check up to the spousal maximum. For example, if your own benefit is $800 and your spousal benefit limit is $1,000, Social Security pays your $800 plus a $200 top-up. The end result is a $1,000 check, not $1,800.