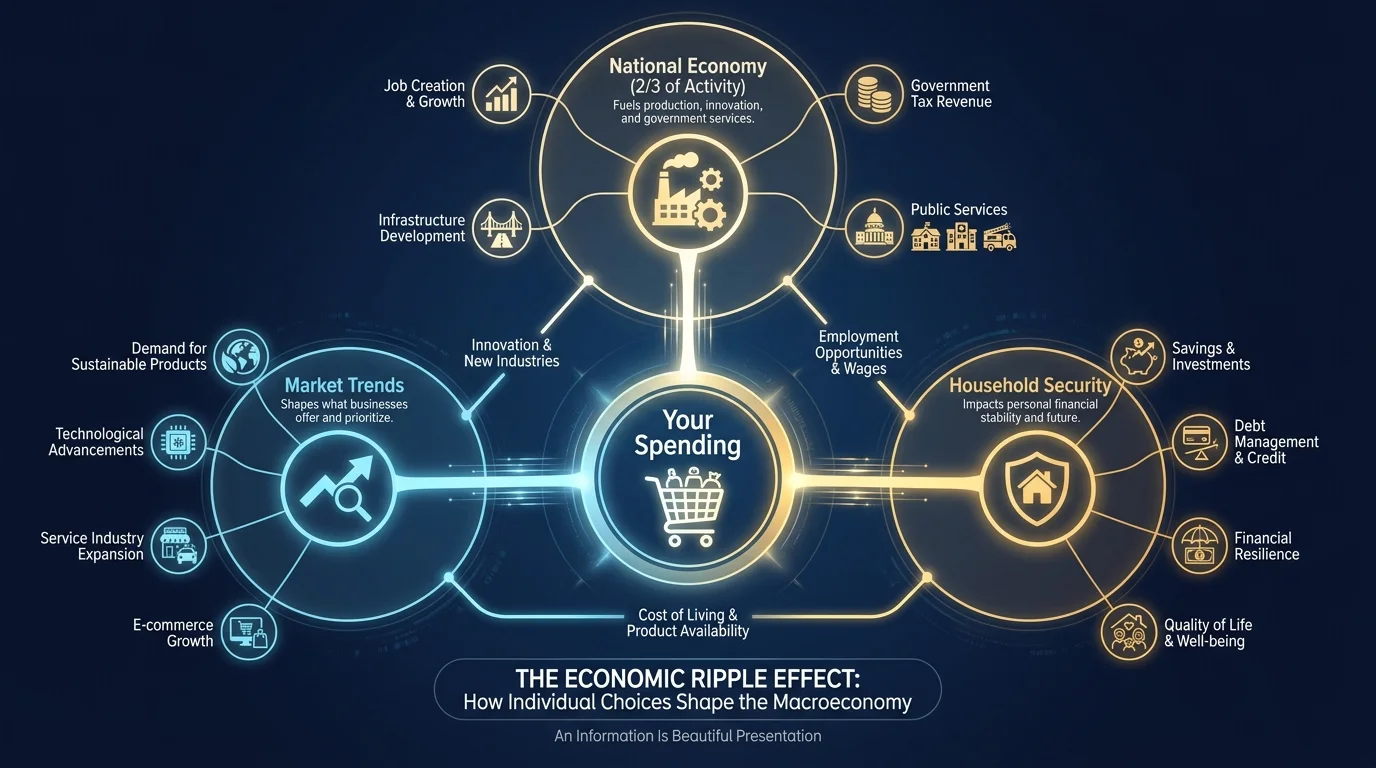

Your daily spending choices do more than just manage your household budget; they send massive signals to the broader economy. In 2026, economists are closely monitoring a consumer landscape defined by sticky inflation, climbing housing costs, and rapidly changing shopping technologies. Despite persistent price fatigue, Americans still wield enormous economic power, driving more than two-thirds of the nation’s economic activity. However, the ways you save, splurge, and subscribe are shifting dramatically. While some households are doubling down on budget brands, others are leaning into artificial intelligence to hunt for the perfect deal. Understanding these emerging patterns can help you anticipate market changes, avoid common financial traps, and ultimately make smarter decisions with your own money this year.

1. The Great Subscription Purge

If you feel overwhelmed by the number of digital services draining your checking account each month, you are experiencing a documented economic trend. In 2024, the average American household juggled over seven active digital subscriptions. By early 2026, data from Deloitte indicates that number has dropped to 5.8, signaling a widespread bout of subscription fatigue.

Consumers are aggressively auditing their recurring costs, canceling redundant streaming platforms, pausing monthly snack boxes, and consolidating software services. Instead of maintaining year-round memberships, many shoppers now practice “subscription rotation”—signing up for a single month to watch a specific television series or utilize a service, and immediately canceling before the auto-renew kicks in. To protect your own budget, review your credit card statements quarterly and challenge every recurring charge. If you haven’t used a service in the past thirty days, pause it.

2. Using AI to Hunt for Deals

Artificial intelligence has officially moved from a tech novelty to a practical shopping companion. According to McKinsey consumer research from early 2026, nearly one in five US consumers report using generative AI tools to discover, evaluate, or decide on products and services.

Instead of sifting through dozens of browser tabs and generic search results, shoppers are deploying AI assistants to do the heavy lifting. A prompt like, “Compare the durability and price of these three vacuum brands for a home with pets,” yields immediate, customized advice. This shift reduces impulse buying by equipping consumers with comprehensive price comparisons and historical data in seconds. However, it is essential to verify AI-generated recommendations directly on retailer websites, as pricing and availability fluctuate rapidly.

3. Leaning Heavily Into Private-Label Groceries

The supermarket checkout line remains the front line for inflation. With grocery prices having climbed nearly 30% over the past five years, the way Americans stock their pantries has permanently changed. Brand loyalty is eroding; instead, shoppers are actively trading down to store brands and private labels at grocers like Aldi, Walmart, and Trader Joe’s.

This behavior crosses income brackets. Even households with comfortable margins are realizing that generic pantry staples, cleaning supplies, and frozen goods offer identical quality at a fraction of the cost. The stigma once associated with “generic” labels has vanished, replaced by a strategic, value-driven approach to essential spending. Optimizing your grocery budget now requires flexibility—buying the store brand for staples and saving premium name-brand purchases strictly for items where you can actually taste or feel the difference.

4. The “K-Shaped” Divergence in Discretionary Spending

Economists frequently use the term “K-shaped” to describe an environment where different demographic groups experience drastically different financial realities. In 2026, this divergence is highly visible in discretionary spending. Higher-income households continue to drive robust spending in travel, domestic flights, and premium experiences, bolstered by stock market gains and higher yields on savings.

Conversely, middle- and lower-income earners are scaling back. Faced with higher borrowing costs and depleted pandemic-era savings, this group is strictly budgeting to cover essentials. If you find yourself in the cautious camp, focus on fortifying your emergency fund rather than keeping up with the discretionary spending habits of peers. Prioritizing liquidity and minimizing high-interest consumer debt remains the safest strategy in a bifurcated economy.

5. The Rise of “Cheap Thrills”

When big-ticket luxuries—like international vacations or new vehicles—feel out of reach due to financing costs, consumers naturally pivot to smaller, more affordable indulgences. This phenomenon keeps specific sectors of the economy surprisingly robust.

“Consumer spending trends in 2026 remain focused on ‘cheap thrills’ and necessary services, and away from expensive and highly discretionary activities.” — The Conference Board, April 2026

Rather than committing to a massive expense, you might upgrade your weekly take-out order, invest in premium pet care, or purchase high-end skincare. These modest treats provide an emotional boost without requiring a loan or derailing long-term financial goals. Recognizing this habit in your own life can help you budget for it intentionally, ensuring these “cheap thrills” remain enjoyable rather than becoming a source of guilt.

6. Social Commerce Taking Over the Cart

The gap between viewing a product online and checking out has virtually disappeared. Social commerce—driven heavily by livestream shopping and in-app checkout features on platforms like TikTok and Instagram—is projected to capture roughly 17% of all online sales in 2026.

This frictionless environment blends entertainment directly with purchasing, making it incredibly easy to spend money without a second thought. Flash sales and exclusive influencer codes create a manufactured sense of urgency. To navigate this landscape safely, institute a mandatory 24-hour cooling-off period for any social media purchase. If you still want the item the next day, you can buy it; more often than not, the impulse will fade.

7. Prioritizing Housing Over Everything Else

Housing costs continue to dictate the rest of the consumer budget. Data shows the average American household is dedicating roughly 33.2% of its income to housing expenses in 2026. Whether you are dealing with elevated mortgage rates, rising property taxes, or steep rent renewals, this fixed cost leaves less wiggle room for everything else.

Because housing consumes such a massive portion of the paycheck, variable expenses like dining out, apparel, and entertainment are taking the hit. If your housing costs exceed the traditional 30% rule of thumb, it is crucial to aggressively monitor your variable spending. Negotiating better rates on auto insurance, cell phone plans, and utilities can help claw back some of the margin lost to housing.

Why It Matters Now

Understanding these habits is crucial because consumer spending makes up over 67% of the total US economic activity. The way you allocate your paycheck directly influences corporate strategies, inventory levels, and even Federal Reserve interest rate decisions.

Forecasters at the Federal Reserve Bank of Philadelphia and other institutions note that while inflation has cooled from its historic peaks, it remains “sticky.” Core Personal Consumption Expenditures (PCE) inflation is hovering around 2.6% to 2.7% in 2026. This means prices are not broadly dropping; they are simply rising at a more manageable pace. Adjusting to this permanent higher-price plateau requires a shift from short-term survival tactics to long-term sustainable habits.

| Spending Behavior | Previous Approach (2023-2024) | 2026 Consumer Trend |

|---|---|---|

| Product Discovery | Search engines and browsing physical aisles | Generative AI comparisons and livestream social commerce |

| Brand Loyalty | Sticking rigidly to familiar household name brands | Trading down to high-quality private labels and store brands |

| Digital Services | Accumulating multiple streaming and software subscriptions | Aggressive consolidation; averaging fewer than six active subscriptions |

| Discretionary Treats | Saving for major luxury goods and massive vacations | Prioritizing everyday “cheap thrills” like premium dining and pet care |

Common Mistakes to Avoid

Navigating the 2026 economy requires vigilance. Protect your budget by avoiding these specific financial traps:

- Ignoring auto-renewals: Letting a $15 monthly charge run unnoticed for a year costs you $180. Treat subscription audits as a mandatory quarterly chore.

- Buying entirely on impulse through social media: The seamless checkout process on social platforms bypasses your brain’s natural hesitation. Always force a delay between seeing a product and clicking “buy.”

- Letting AI entirely dictate your purchases: While AI tools are excellent for initial research, they occasionally pull outdated pricing or hallucinate specs. Always verify the final details on the official retailer’s site.

- Sacrificing emergency savings for “cheap thrills”: Treating yourself is important for morale, but not if it comes at the expense of your financial safety net. Automate your savings deposits first, then spend what is left over.

Getting Expert Input

While tweaking your grocery list or canceling a streaming service is something you can easily do independently, larger financial adjustments in this economy require a professional eye. Consider consulting a certified financial planner, fiduciary, or tax advisor in these scenarios:

- Rebalancing your investment portfolio: If sticky inflation is eating into your cash reserves, an advisor can help you allocate assets to better outpace rising costs.

- Refinancing or taking a home equity loan: With housing costs dominating budgets, unlocking home equity can be tempting. A professional can help you calculate the true cost of borrowing against your home in a shifting interest rate environment.

- Restructuring high-interest credit card debt: If you leaned heavily on credit cards over the past two years, an expert can guide you through consolidation strategies or balance transfer options to minimize interest payments.

Frequently Asked Questions About 2026 Spending

Are everyday prices expected to drop in 2026?

Broadly speaking, no. Economists project “disinflation,” which means prices are rising at a slower, more normal rate (around 2.6%). While specific categories like eggs or certain electronics may see price drops, the overall cost of living is stabilizing at its current, higher plateau rather than returning to 2019 levels.

What is the biggest driver of consumer spending right now?

Housing and necessary services dominate the consumer budget. Because Americans are spending roughly a third of their income on shelter, spending growth in other areas is largely fueled by essentials, healthcare, and modest entertainment choices rather than massive durable goods.

How do economists track these inflation and spending trends?

Economists primarily use two metrics: the Consumer Price Index (CPI), which measures out-of-pocket expenses for urban consumers, and the Personal Consumption Expenditures (PCE) price index. The Federal Reserve heavily favors the PCE because it accounts for changes in consumer behavior—like swapping expensive beef for cheaper poultry when prices rise.

Tracking macroeconomic data might sound complex, but it ultimately boils down to how you behave in the grocery aisle, on your smartphone, and at the gas pump. By staying aware of how algorithms, inflation, and subscription models influence your choices, you regain control over your cash flow. The information here is meant for educational purposes. Specific circumstances—including health conditions, finances, location, and goals—may require different approaches. When in doubt, consult a licensed professional or check official sources directly.

Last updated: May 2026. Rules, prices, and details change—verify current information with official sources before acting on it.