Retiring brings a new set of financial rules that can work entirely in your favor. Beyond standard retail discounts, a valuable layer of financial perks unlocks precisely when you reach your sixties. Federal agencies and state governments offer specific provisions designed to shield your retirement income and cut everyday expenses. These benefits include enhanced tax deductions, local property tax freezes, and penalty-free access to health savings accounts for non-medical spending. Because these programs are rarely advertised, millions of eligible older adults miss out on keeping more of their own money. By understanding the exact age thresholds and application requirements for these targeted benefits, you can strategically lower your overhead and stretch your retirement savings further.

1. The IRS “Bonus” Standard Deductions for Seniors

As you map out your retirement cash flow, your tax strategy should shift to take advantage of specific age-based deductions. According to the Internal Revenue Service, the tax code layers multiple benefits for older filers that can drastically reduce your taxable income.

If you are 65 or older and choose not to itemize, you receive the regular standard deduction plus an “additional standard deduction.” For the 2025 and 2026 tax years, this extra deduction provides $2,000 for single filers or $1,600 per qualifying spouse for married couples filing jointly.

Furthermore, recent tax legislation introduced a temporary $6,000 Senior Bonus Deduction per eligible person aged 65 or older. This deduction applies whether you take the standard deduction or itemize. It begins to phase out for single filers with a Modified Adjusted Gross Income (MAGI) over $75,000 and for joint filers with a MAGI over $150,000. When you stack the regular standard deduction, the additional senior standard deduction, and the new bonus deduction, a qualifying married couple can shield tens of thousands of dollars from federal income taxes before paying a single cent.

2. Penalty-Free HSA Withdrawals for Non-Medical Expenses

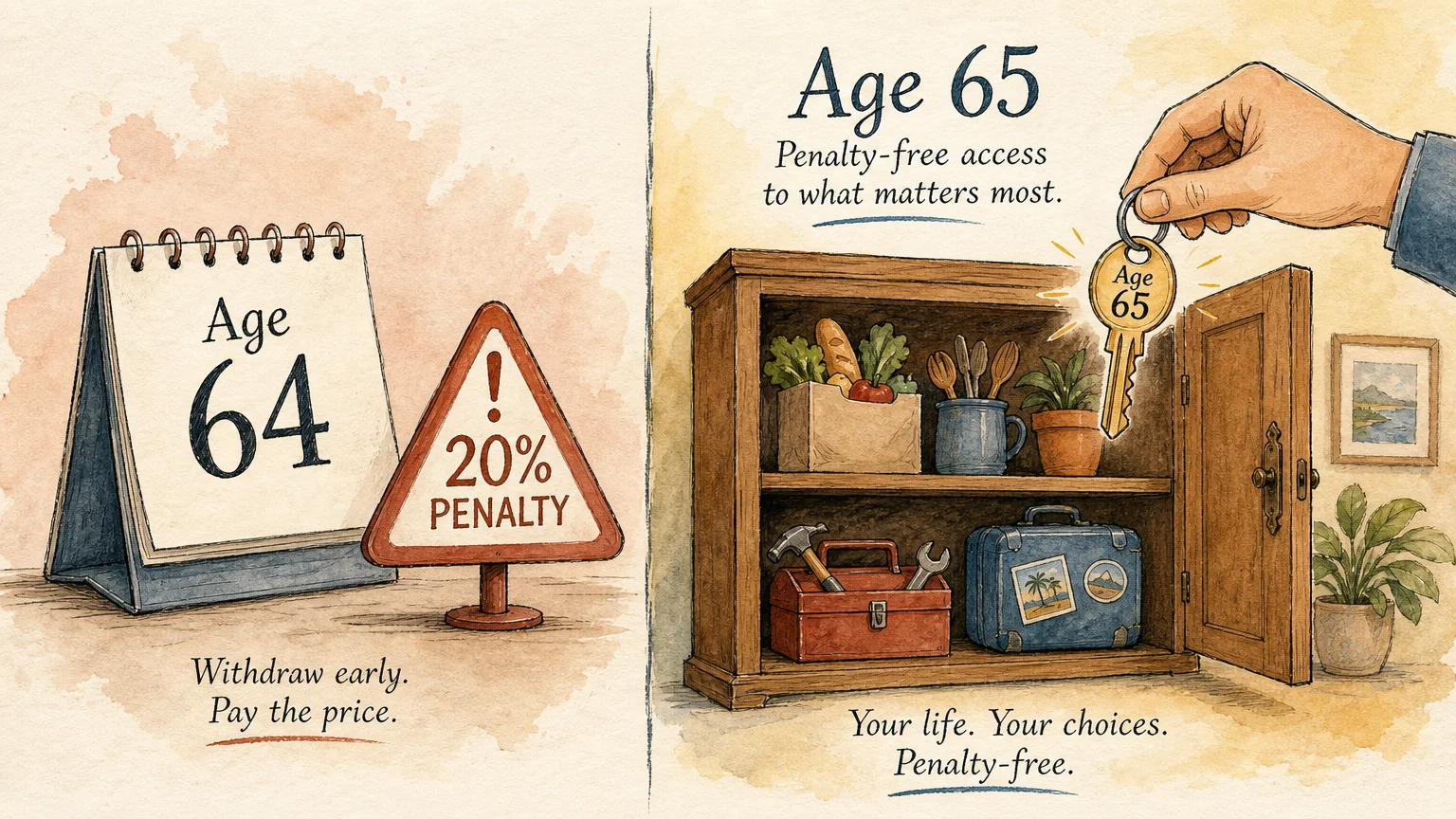

Health Savings Accounts (HSAs) operate under strict regulations during your working years, but those rules loosen significantly on your 65th birthday. Before age 65, pulling money out of an HSA for anything other than qualified medical expenses triggers a steep 20% IRS penalty on top of ordinary income taxes.

Once you turn 65, that 20% penalty disappears entirely. You can withdraw funds for home repairs, groceries, or a vacation; you will simply pay ordinary income tax on the withdrawal, making the account function identically to a Traditional IRA.

Additionally, crossing the age-65 threshold unlocks new tax-free medical spending options. According to IRS Publication 969, you can use your HSA funds to pay your Medicare Part B, Part C (Medicare Advantage), and Part D prescription drug premiums tax-free.

| Health Savings Account Feature | Before Age 65 | Age 65 and Older |

|---|---|---|

| Non-Medical Withdrawals | Subject to income tax plus a 20% IRS penalty | Subject to income tax only (no 20% penalty) |

| Medicare Premiums (Parts B, C, D) | Not an eligible tax-free expense | Eligible tax-free expense |

| Medigap (Supplemental) Premiums | Not eligible | Not eligible |

| New Contributions | Allowed if enrolled in a qualifying HDHP | Must stop once enrolled in any part of Medicare |

3. State Exemptions on Social Security Taxes

A common retirement myth suggests that if the federal government taxes a portion of your Social Security benefits, your state government will inevitably do the same. In reality, the vast majority of states leave your benefits alone.

By 2026, 41 states completely exempt Social Security income from state taxation. Recent legislative pushes have eliminated the tax entirely in states like Missouri, Kansas, Nebraska, and Iowa. Only nine states still tax these benefits: Colorado, Connecticut, Minnesota, Montana, New Mexico, Rhode Island, Utah, Vermont, and West Virginia.

Even if you live in one of the nine states that still tax Social Security, you might not owe anything. Many of these states offer income-based exemptions that protect average earners. West Virginia, for example, is actively phasing out its Social Security tax entirely by 2026. Understanding your state’s specific threshold can help you decide exactly how much income to draw from your other retirement accounts without triggering state taxes on your Social Security check.

4. The $80 Lifetime America the Beautiful Senior Pass

Travel ranks highly on most retirement bucket lists, but entrance fees to federal lands can drain a fixed budget quickly. The National Park Service offers a massive, lifelong discount specifically designed for older adults.

U.S. citizens and permanent residents age 62 and older can purchase the America the Beautiful Senior Lifetime Pass for a one-time fee of $80. If you prefer a short-term option, an annual version is available for $20. This pass provides access to over 2,000 federal recreation sites across the country, covering entrance fees at national parks, national wildlife refuges, and national forests.

The pass covers the owner and all passengers in a single, private, non-commercial vehicle. While recent changes raised the non-resident annual pass to $250, the U.S. resident senior rate remains untouched, making the $80 lifetime pass an exceptional financial value for domestic retirees.

5. Local Property Tax Freezes and Circuit Breaker Credits

Rising property values invariably lead to rising property taxes. When you live on a fixed income, this dynamic can force you to sell a home you otherwise want to keep. To prevent older adults from being priced out of their neighborhoods, many states and local municipalities offer specific property tax relief programs.

These programs generally fall into two categories:

- Property Tax Freezes: States like Texas offer an “Over-65” exemption that permanently places a ceiling on the amount of school district taxes you pay on your primary residence. Once you qualify, your school tax bill will not rise, even if your property value skyrockets. New York provides a similar benefit through its Senior Citizen Tax Exemption and the STAR program.

- Circuit Breaker Programs: States like Michigan and Maryland utilize “circuit breaker” models. These programs act like an electrical circuit breaker—if your property tax bill exceeds a specific percentage of your household income (often 3% to 5%), the state steps in with a direct tax credit or refund to absorb the financial overload.

These benefits are rarely automatic. You must proactively file an application with your county or municipal tax assessor, and you usually need to provide proof of age and income.

6. Tuition-Free College Courses and Auditing Programs

Retirement provides the time to learn new skills, and state governments often provide the funding. Over 50 states offer some form of free or deeply discounted college education for older residents.

Florida’s Senior Scholar program allows residents aged 60 and older to audit courses at state universities and colleges completely free of charge, with tuition and associated fees waived. Ohio State University runs Program 60, allowing residents 60 and older to take tuition-free, non-credit courses and connect with the university community.

These programs typically require you to register on a space-available basis and cover the cost of your own textbooks. However, stripping away the cost of tuition removes the largest financial barrier to lifelong learning, allowing you to explore subjects ranging from art history to personal finance without taking on student debt.

What This Means for You

Retirement planning often fixates on accumulating assets, but managing your expenses and taxes in retirement is equally vital. Stringing these six distinct perks together alters your fundamental cash flow. Saving a few thousand dollars on federal income taxes, eliminating state taxes on your Social Security benefits, and securing a property tax freeze can drastically reduce your monthly overhead.

The federal and state tax codes heavily subsidize the transition into retirement, but they do not do the work for you. You must know which boxes to check, which forms to file, and which deadlines to meet to capture the savings.

When your living expenses drop, you do not need to withdraw as much money from your 401(k) or traditional IRA. Keeping those funds invested longer gives your portfolio more time to grow, extending the lifespan of your retirement savings.

What Can Go Wrong

While these programs offer excellent benefits, they come with strict compliance rules. Misunderstanding the fine print can lead to unexpected tax bills or missed opportunities.

- Contributing to an HSA while on Medicare: Once you enroll in any part of Medicare—including the premium-free Part A—you are no longer eligible to make new contributions to an HSA. Continuing to contribute will trigger IRS tax penalties.

- Missing local property tax deadlines: Property tax freezes and circuit breaker credits require annual or one-time applications submitted directly to your local tax authority. If you miss the county deadline, you usually have to pay the higher tax rate for the entire year.

- Using HSA funds for Medigap premiums: While the IRS allows you to pay for Medicare Advantage and Part D premiums using tax-free HSA funds, Medicare Supplement (Medigap) premiums explicitly do not qualify. Reimbursing yourself for Medigap premiums will result in a taxable withdrawal.

- The “Married Filing Separately” trap: Certain federal tax benefits, including the new $6,000 Senior Bonus Deduction, completely disallow taxpayers who use the Married Filing Separately status. You must file jointly or as a single taxpayer to qualify.

Where Outside Advice Pays Off

Navigating the intersection of tax law, healthcare, and state regulations can quickly become complex. Hiring a professional is often worth the upfront cost in the following scenarios.

First, coordinate your Medicare enrollment with your HSA strategy. A financial advisor or Medicare specialist can help you calculate the exact date to stop your HSA contributions to avoid retroactive IRS penalties, which often apply because Medicare Part A coverage can backdate up to six months.

Second, seek tax planning assistance if your income fluctuates. Because the Senior Bonus Deduction phases out at specific modified adjusted gross income levels, a Certified Public Accountant (CPA) can help you time your IRA distributions or capital gains realization to ensure you stay under the threshold.

Finally, consult a professional before relocating for tax purposes. Moving to a state that does not tax Social Security might seem appealing, but an advisor can help you calculate the full picture—factoring in state sales taxes, local property taxes, and the cost of healthcare in your proposed destination.

Frequently Asked Questions

Do I automatically receive the extra standard deduction when I turn 65?

No. The IRS does not automatically apply the additional standard deduction or the Senior Bonus Deduction based on your birthdate alone. You must actively choose to take the standard deduction rather than itemizing, and you must check the specific age-related box on your Form 1040. If you use tax software, you must ensure your date of birth is entered correctly to trigger the prompt.

Can I still contribute to my HSA if I am over 65 but still working?

Yes, but only if you have strictly delayed your Medicare enrollment. If you are over 65, remain covered by an eligible high-deductible health plan through your employer, and have not enrolled in any part of Medicare (including Part A), you can continue making contributions. The moment your Medicare coverage goes active, your eligibility to contribute ends.

Are property tax circuit breaker programs available in every state?

No. Property taxes are governed at the state and county level, meaning relief programs vary wildly depending on your zip code. While nearly all states offer some form of basic homestead exemption, only about half utilize true income-based circuit breaker programs. You must check with your county tax assessor to find out exactly which programs operate in your jurisdiction and what the income limits are.

Securing your finances in retirement requires an active approach to your benefits. Take the time to audit your eligibility for these six perks. A few hours spent filing the right forms with the IRS, the National Park Service, or your local county assessor can yield thousands of dollars in savings year after year.

Last updated: June 2026. Rules, prices, and details change—verify current information with official sources before acting on it. The information here is meant for educational purposes. Specific circumstances—including health conditions, finances, location, and goals—may require different approaches. When in doubt, consult a licensed professional or check official sources directly.