The average Social Security retirement benefit in 2026 hovers around $2,071 per month—roughly $24,850 a year. For most Americans, that payout falls far short of actual living expenses, creating a daunting financial gap. According to the Bureau of Labor Statistics, the average household aged 65 and older spends about $61,432 annually on housing, healthcare, transportation, and daily necessities. Whether you are already collecting checks or plotting your future exit from the workforce, understanding the precise math between guaranteed benefits and real costs is non-negotiable. By dissecting the latest data, adjusting for taxes, and identifying smart withdrawal strategies, you can build a sustainable financial plan that prevents your savings from running dry.

The Reality of the Average Social Security Check in 2026

The system was never designed to be your sole source of retirement income. When Social Security was created, it was meant to act as a safety net that replaced roughly 40% of an average earner’s pre-retirement wages. Today, however, many Americans enter their senior years relying on those monthly deposits to cover the bulk of their bills.

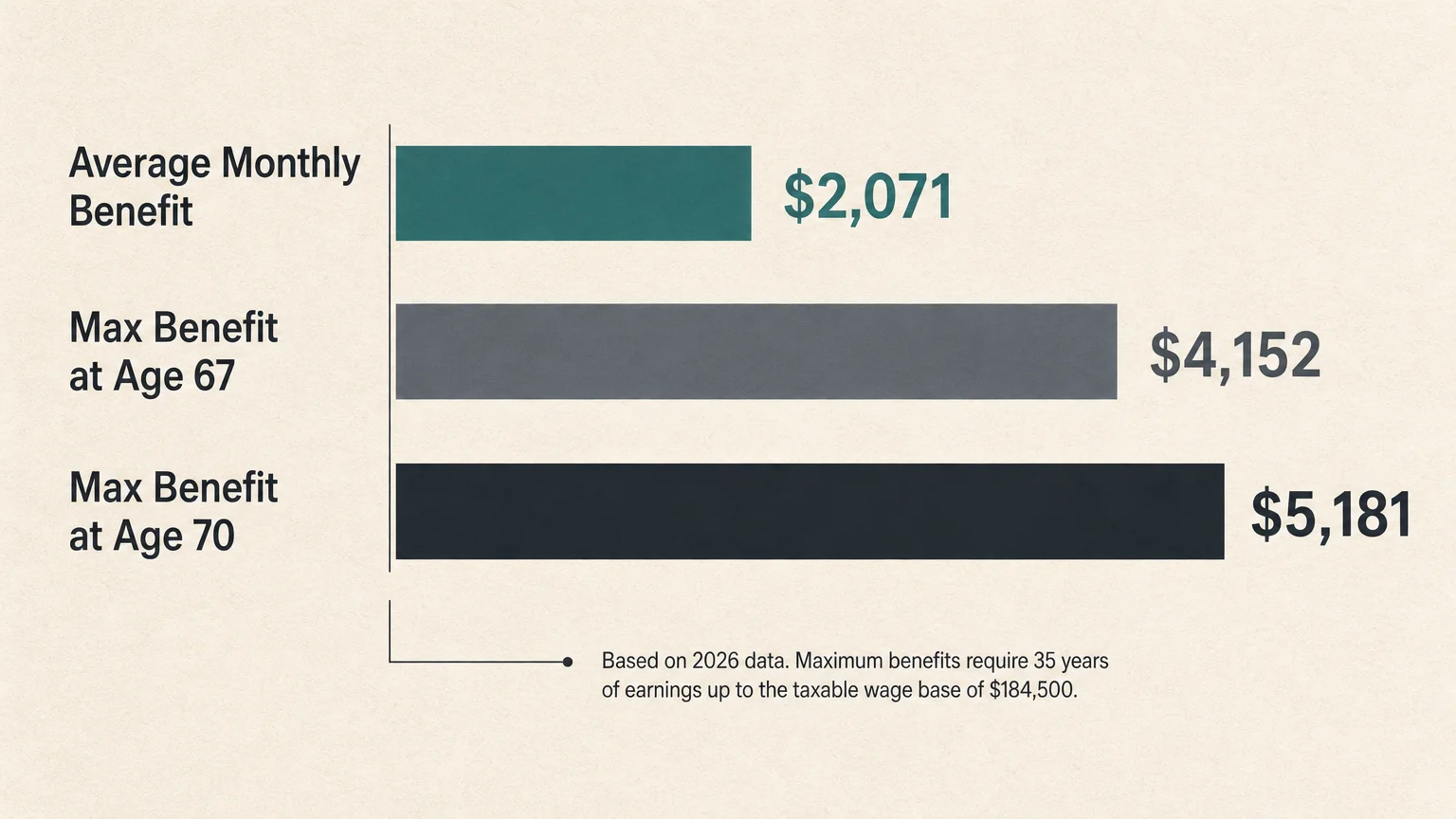

For 2026, the Social Security Administration applied a 2.8% cost-of-living adjustment (COLA). This bump brought the average monthly retirement benefit to $2,071. While seeing the average check cross the $2,000 threshold represents a milestone, the reality of living on $24,850 a year is sobering when compared to current market prices for rent, groceries, and medical care.

Of course, your personal benefit depends entirely on your earnings record and your claiming age. If you wait until full retirement age—which is 67 for anyone born in 1960 or later—the maximum possible benefit tops out at $4,152 per month in 2026. If you delay claiming until age 70, that ceiling rises to $5,181. However, securing the absolute maximum requires you to have earned at or above the taxable wage base (capped at $184,500 in 2026) for 35 separate years. Only a tiny fraction of the workforce achieves this. The vast majority of retirees must learn to navigate their golden years closer to the $2,071 average.

What It Actually Costs to Live in Retirement

Understanding the income side of the equation is only half the battle. To see the true financial picture, you must look at outlays. According to the Consumer Expenditure Survey published by the U.S. Bureau of Labor Statistics, households led by individuals aged 65 and older spend an average of $61,432 per year. That breaks down to about $5,119 per month.

Where exactly does that money go? The budget of an average retiree is heavily skewed toward a few non-negotiable categories:

- Housing: This is consistently the largest expense, absorbing nearly a third of a retiree’s budget. Even if you have paid off your mortgage, you still face property taxes, homeowners insurance, routine maintenance, and utility bills. For renters, the burden is often heavier, as annual rent increases outpace fixed-income adjustments.

- Healthcare: Healthcare acts as the ultimate wild card in retirement. Original Medicare (Parts A and B) does not cover everything. You are still responsible for monthly premiums, deductibles, co-pays, and services like routine dental care, vision exams, and hearing aids. The BLS notes that older adults spend significantly more out-of-pocket on medical care than younger demographics.

- Transportation: Whether you are making a daily commute or just driving to the grocery store and doctor appointments, vehicle maintenance, insurance, and fuel remain significant line items. Older households still average thousands of dollars a year simply keeping a car on the road.

- Food and Utilities: The cost of groceries and dining out continues to pressure fixed incomes. Meanwhile, utility costs for heating, cooling, and internet access remain fixed, regardless of how much your portfolio earns in a given year.

There is also a hidden mathematical headwind: inflation impacts retirees differently than active workers. The Social Security COLA is tied to the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). However, retirees generally spend a much larger percentage of their income on healthcare—a sector where costs historically rise much faster than standard consumer goods. As a result, your official cost-of-living increase often feels inadequate compared to the actual bills arriving in your mailbox.

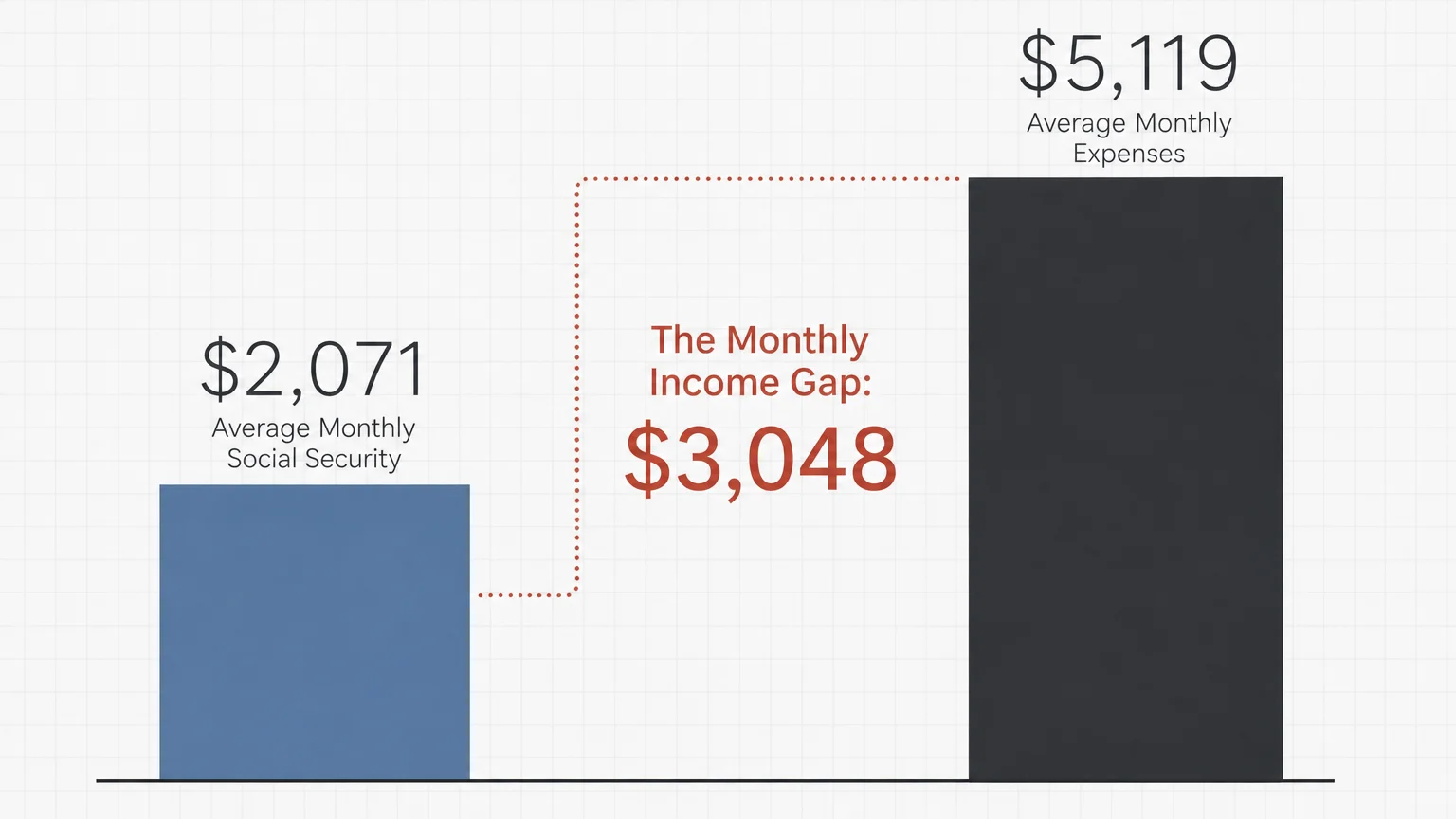

The Monthly Gap: Social Security vs. Real-World Expenses

The tension between what the government provides and what life actually costs becomes glaringly obvious when you place the numbers side by side. Consider the gap between the average Social Security benefit and the average household expenses reported by the BLS.

| Household Scenario | Average Monthly Social Security Income | Estimated Monthly Living Expenses | The Monthly Shortfall |

|---|---|---|---|

| Single Retiree (Assuming average benefit and modestly adjusted expenses) |

$2,071 | $3,800 | -$1,729 |

| Dual-Retiree Household (Both receiving the average benefit) |

$4,142 | $5,119 | -$977 |

| Single Retiree Claiming Early at 62 (30% reduction applied to average) |

$1,449 | $3,800 | -$2,351 |

These shortfalls represent the amount you must withdraw from your 401(k), IRA, pension, or personal savings every single month just to maintain a baseline standard of living. For a single retiree receiving the average benefit, that $1,729 monthly gap translates to roughly $20,748 a year. Over a 25-year retirement, you would need more than half a million dollars in supplementary savings just to break even—and that is before factoring in taxes, market volatility, or a long-term care event.

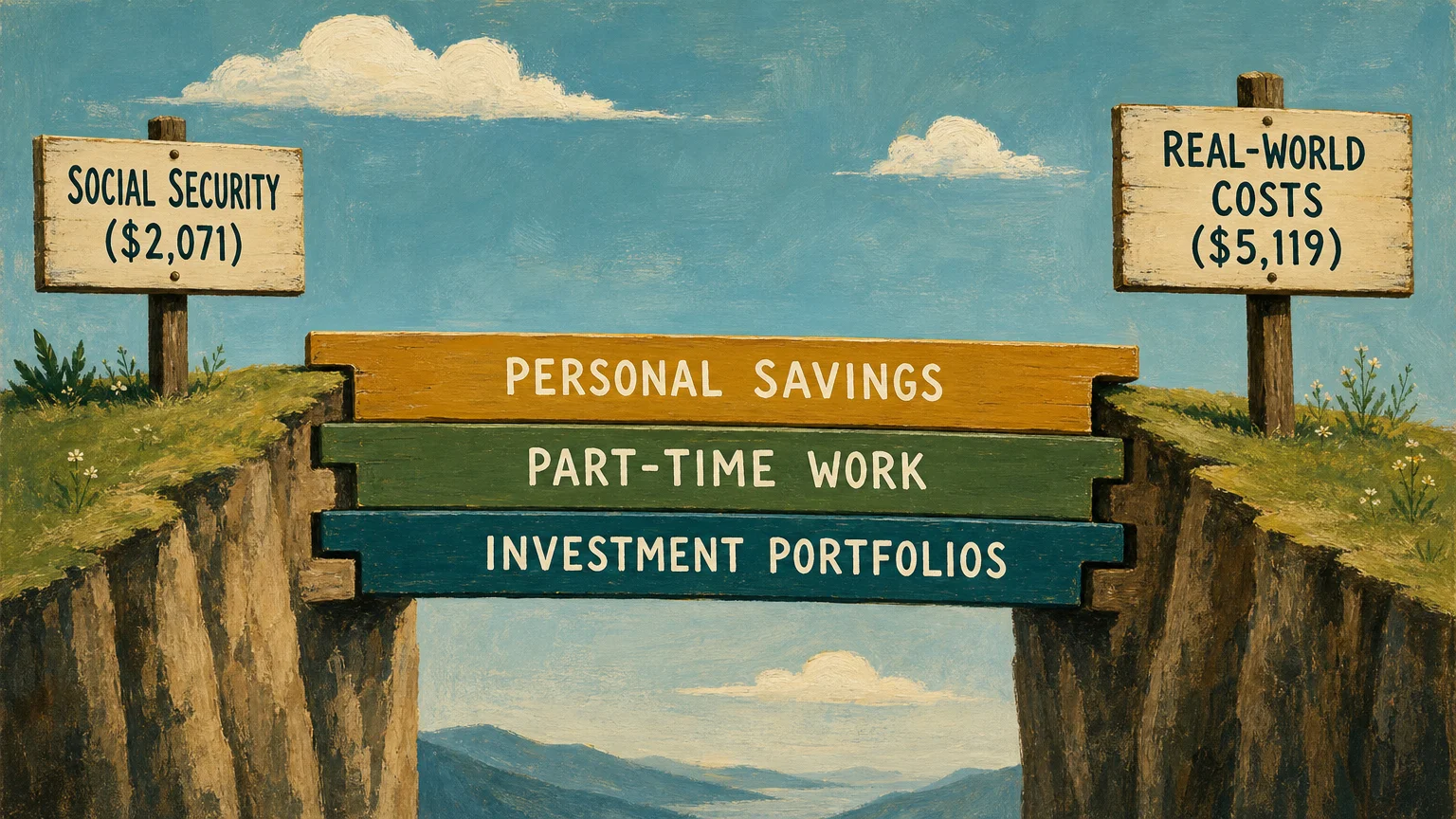

Strategies to Bridge the Retirement Income Gap

If the math leaves you feeling uneasy, the good news is that you have levers you can pull to close the gap. Bridging the shortfall requires a mix of income optimization and strategic cost reduction.

- Maximize your claiming age: Timing is the most powerful tool you have. If you claim Social Security at 62, your monthly check is permanently reduced by up to 30%. Conversely, for every year you delay claiming past your full retirement age, your benefit increases by a guaranteed 8% until age 70. Waiting from 67 to 70 locks in a 24% permanent boost, significantly reducing the pressure on your personal savings.

- Relocate to a tax-friendly environment: Housing and taxes drain retirement accounts quickly. Relocating to a state with no income tax—or a state that explicitly exempts Social Security and pension income from taxation—can instantly increase your take-home pay. Downsizing to a smaller, more energy-efficient home also slashes property taxes, utility bills, and maintenance costs.

- Adopt a dynamic withdrawal strategy: Relying on the traditional “4% rule” is a start, but a dynamic approach works better. By adjusting your portfolio withdrawals based on market performance—taking less during bear markets and slightly more during bull markets—you can preserve your capital. Keeping a cash bucket holding one to two years of living expenses prevents you from having to sell stocks at a loss when the market dips.

- Generate supplementary income streams: You do not necessarily need to work a strenuous full-time job. Many retirees bridge the gap through part-time consulting, freelance work, or turning a hobby into a small business. Additionally, reallocating a portion of your portfolio toward dividend-paying stocks or a fixed annuity can create a steady stream of cash to cover your baseline utility and grocery bills.

Things to Watch Out For

When you are operating on a fixed income, small miscalculations can trigger cascading financial problems. Before finalizing your retirement budget, pay close attention to these specific pitfalls.

- The “Tax Torpedo” on your benefits: Social Security benefits are not automatically tax-free. The IRS uses a formula called “provisional income” (your adjusted gross income + nontaxable interest + half of your Social Security benefits). If your provisional income exceeds $25,000 as a single filer or $32,000 as a joint filer, up to 50% of your benefits become taxable. If it exceeds $34,000 (single) or $44,000 (joint), up to 85% of your benefits can be taxed. Failing to account for this will leave you with a smaller net income than you projected.

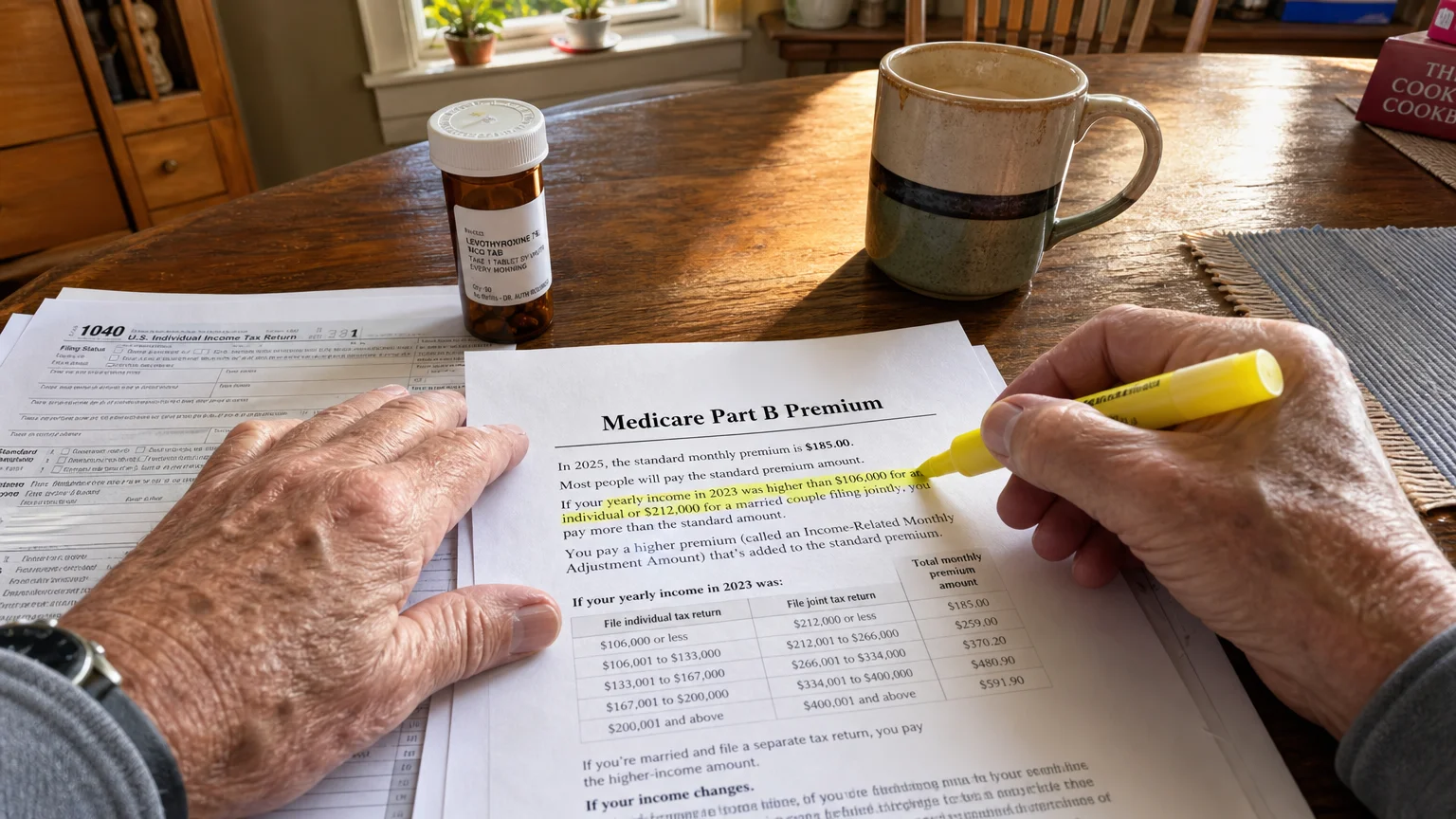

- Medicare Part B premium hikes: Your Medicare Part B premiums are deducted directly from your Social Security check before the money ever hits your bank account. In years where healthcare costs surge, a significant portion of your annual COLA can be instantly wiped out by a corresponding increase in Part B premiums. Always budget for net Social Security income, not the gross amount.

- The earnings test penalty: If you decide to claim Social Security before reaching your full retirement age but continue to work, the SSA will withhold a portion of your benefits if you earn over a specific threshold. In 2026, the SSA deducts $1 from your benefits for every $2 you earn above $24,480. While you eventually get this money back in the form of a recalculated benefit later, the immediate cash flow reduction catches many working retirees off guard.

- Claiming early out of fear: Some retirees rush to claim at 62 because they fear the Social Security trust fund will run dry. According to the latest trustees report, even if the trust fund reserves are depleted by the mid-2030s, ongoing payroll taxes would still cover roughly 80% of promised benefits. Locking in a permanent 30% reduction at age 62 to hedge against a potential future 20% cut is often a mathematical mistake that harms your longevity protection.

When DIY Isn’t Enough

Managing a budget and tracking expenses is something most people can handle on their own. However, retirement income planning features complex, interconnected rules. Making the wrong move in one area can trigger severe tax consequences in another. In the following scenarios, bringing in a fiduciary financial planner or tax advisor is a smart investment.

- Coordinating spousal and survivor benefits: If you are married, divorced, or widowed, the rules surrounding whose earnings record you can claim on are highly specific. A professional can run the break-even math to determine the optimal sequence for you and your spouse to claim, ensuring the surviving spouse is left with the highest possible monthly benefit.

- Navigating the Medicare IRMAA surcharge: If you have a year of unusually high income—perhaps from selling a home, taking a massive portfolio withdrawal, or doing a large Roth conversion—you could trigger the Income-Related Monthly Adjustment Amount (IRMAA). This significantly inflates your Medicare Part B and Part D premiums for a full year. Professionals can help you structure your income to stay just below these painful thresholds.

- Executing Roth conversions: Moving money from a traditional, tax-deferred IRA into a tax-free Roth IRA can save you thousands over a long retirement. However, the conversion amount is treated as ordinary income in the year you make the move. A tax advisor can help you execute a multi-year conversion strategy that fills up the lower tax brackets without accidentally pushing you into a higher one.

- Managing Required Minimum Distributions (RMDs): Once you hit age 73 (or 75, depending on your birth year), the IRS forces you to withdraw a specific percentage of your tax-deferred accounts annually, whether you need the money or not. A professional can help you formulate a charitable giving strategy or a qualified longevity annuity contract (QLAC) to mitigate the tax impact of these forced distributions.

You have worked decades to build your financial foundation. Navigating the transition from collecting a paycheck to living off your assets requires a fundamental shift in how you view your money. While the average Social Security benefit will not cover a luxury lifestyle, pairing it with clear-eyed budgeting, tax optimization, and a strategic withdrawal plan allows you to command your future with confidence. Take the time to run your specific numbers, account for inflation, and structure your assets to protect your independence.

This article provides general information only. Every reader’s situation is different—what works for others may not be the right fit for you. For personalized guidance on health, legal, or financial matters, consult a qualified professional.

Last updated: May 2026. Rules, prices, and details change—verify current information with official sources before acting on it.