Millions of Americans base their retirement plans on Social Security, yet the rules dictating your monthly benefit continue to shift. As we navigate 2026, understanding the latest changes to the program is no longer optional—it is a critical requirement for protecting your household budget. From new limits on how much you can earn while working to updated cost-of-living projections and a shrinking timeline for the program’s trust fund, the landscape looks different than it did just a few years ago. Securing your financial future requires knowing exactly how these updates impact your payout. Here are ten concrete facts defining the next chapter of Social Security to help you maximize every dollar you have earned.

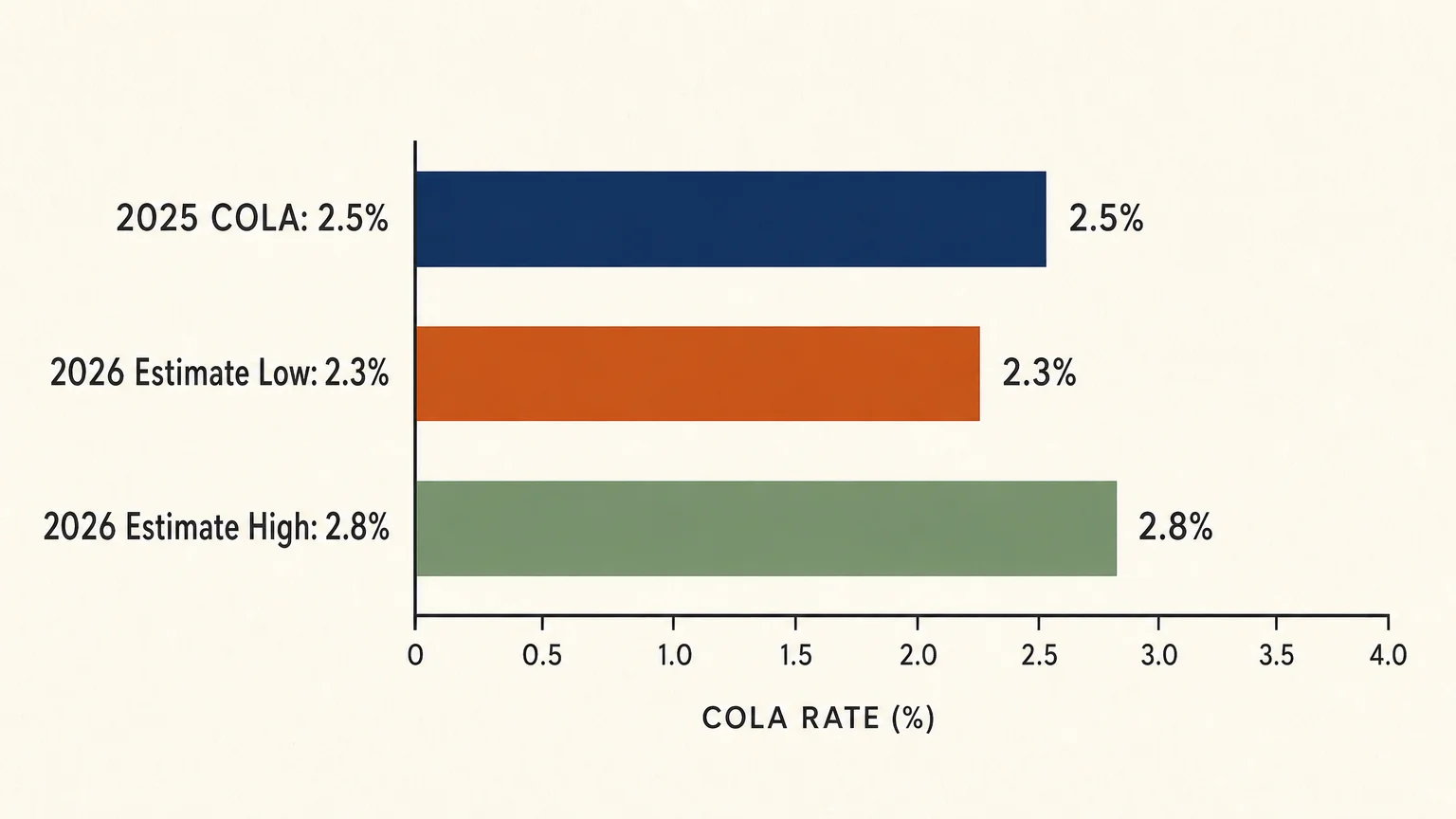

1. The Cost-of-Living Adjustment (COLA) Forecast Points to Moderation

For 2026, initial estimates point to a modest cost-of-living adjustment compared to the historic highs seen earlier in the decade. Early projections from The Senior Citizens League place the 2026 COLA around 2.3 percent, while some financial industry models estimate it could tick up to 2.8 percent. This represents a slight cooling from the 2.5 percent increase beneficiaries saw in 2025. The official COLA number is finalized every October, determined by the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) during the third quarter of the year. While a smaller COLA indicates inflation is easing, many retirees note that specific living expenses—like housing, property taxes, and healthcare—continue to outpace the official inflation metrics.

2. The Trust Fund Depletion Timeline Is Shrinking

The latest Social Security Trustees Report highlights a closing window for the program’s primary financial reserves. Current forecasts indicate the Old-Age and Survivors Insurance (OASI) trust fund could run dry by the fourth quarter of 2032. However, many people misunderstand what “depletion” actually means. It does not mean Social Security goes bankrupt and payments stop completely. Current payroll taxes from active workers will continue to roll in. If Congress fails to enact a fix before the 2032 deadline, those ongoing revenues will only cover about 78 percent of scheduled benefits, which would result in an automatic, across-the-board benefit cut of roughly 22 percent. As Nancy Altman, president of Social Security Works, noted following the recent report:

“If we cut Social Security, nobody will be able to retire.”

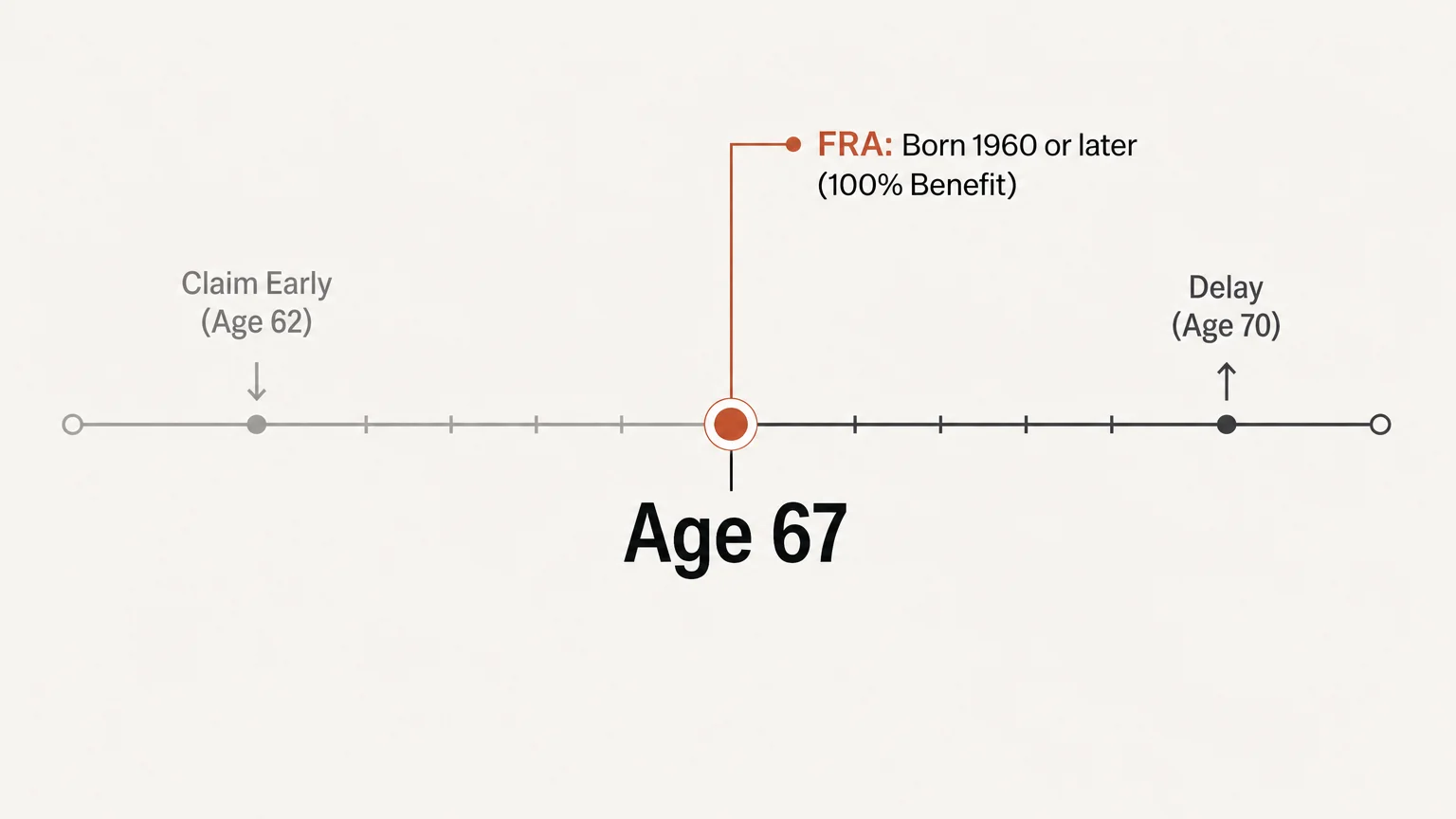

3. Full Retirement Age (FRA) Is Locked at 67

Your Full Retirement Age is the exact age when you are entitled to 100 percent of your earned monthly benefit. Under current law, for anyone born in 1960 or later, your FRA is precisely 67. If you were born between 1955 and 1959, your FRA scales up in two-month increments. Knowing your specific FRA is crucial because every other Social Security retirement calculation—whether you file early or delay—hinges on this baseline number. Claiming before your FRA permanently reduces your check, while waiting past it permanently increases it.

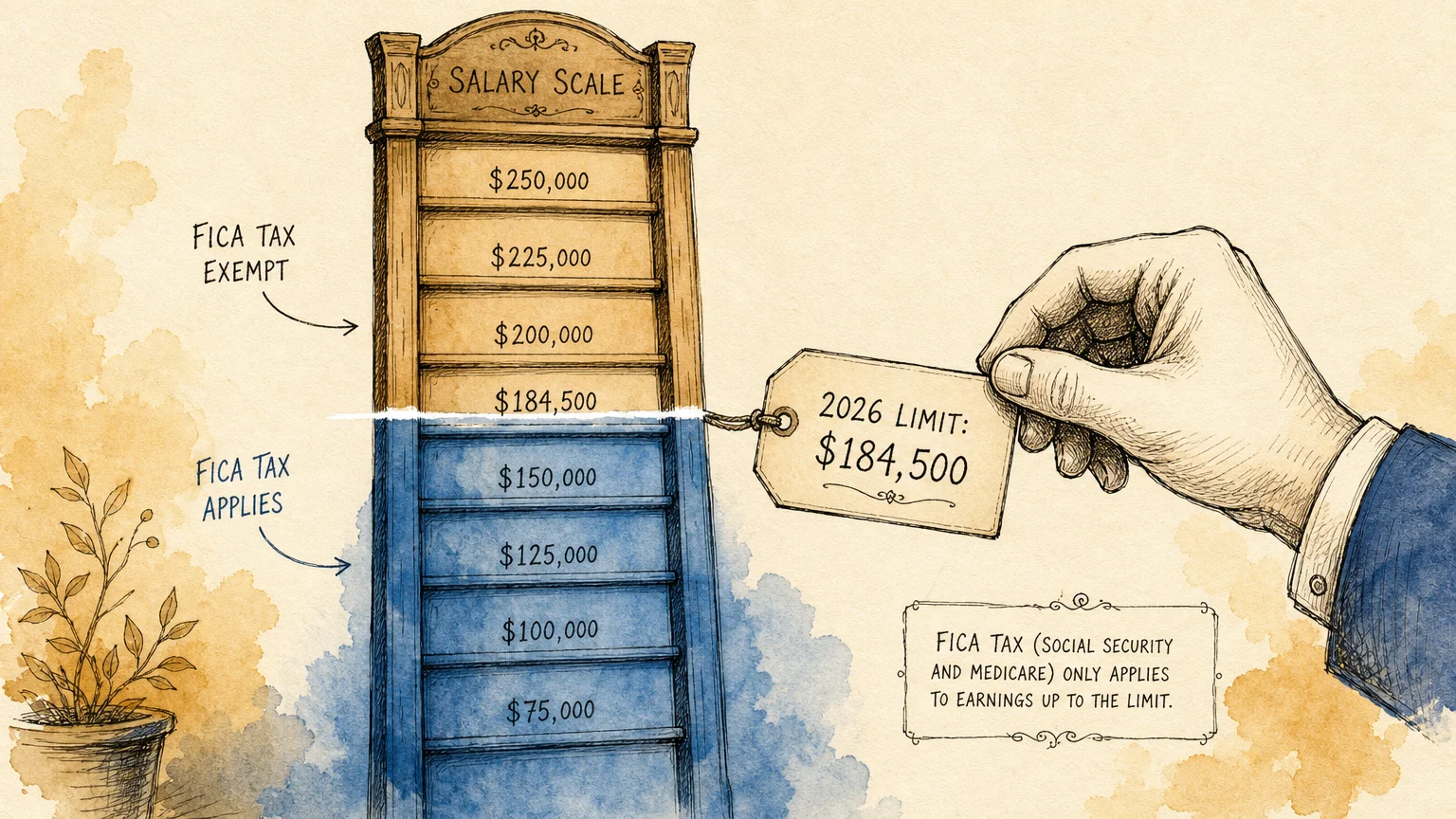

4. The Maximum Taxable Earnings Limit Rose Again

Social Security is funded largely by the Federal Insurance Contributions Act (FICA) payroll tax. Most workers pay 6.2 percent of their wages, and their employers match that amount (self-employed individuals pay the full 12.4 percent). However, high earners do not pay this tax on all of their income. In 2026, the maximum taxable earnings limit is $184,500. Any income earned above that threshold is entirely exempt from Social Security payroll taxes. The IRS adjusts this limit annually to keep pace with average national wage growth. Keep in mind, while the Social Security tax has a cap, the Medicare payroll tax applies to all earned income without any limit.

5. You Can Work While Claiming Early, But There Is a Limit

Many Americans choose to claim benefits early while still holding down a job. If you do this before reaching your FRA, your income is subject to the retirement earnings test (RET). In 2026, the standard earnings limit is $24,480. If your wages exceed this threshold, the Social Security Administration will withhold $1 in benefits for every $2 you earn above the cap. In the specific calendar year you reach your FRA, the limit jumps significantly to $65,160, and the penalty drops to $1 withheld for every $3 over the limit. Once you hit the actual month of your Full Retirement Age, the earnings limit disappears entirely, allowing you to earn as much as you want without penalty.

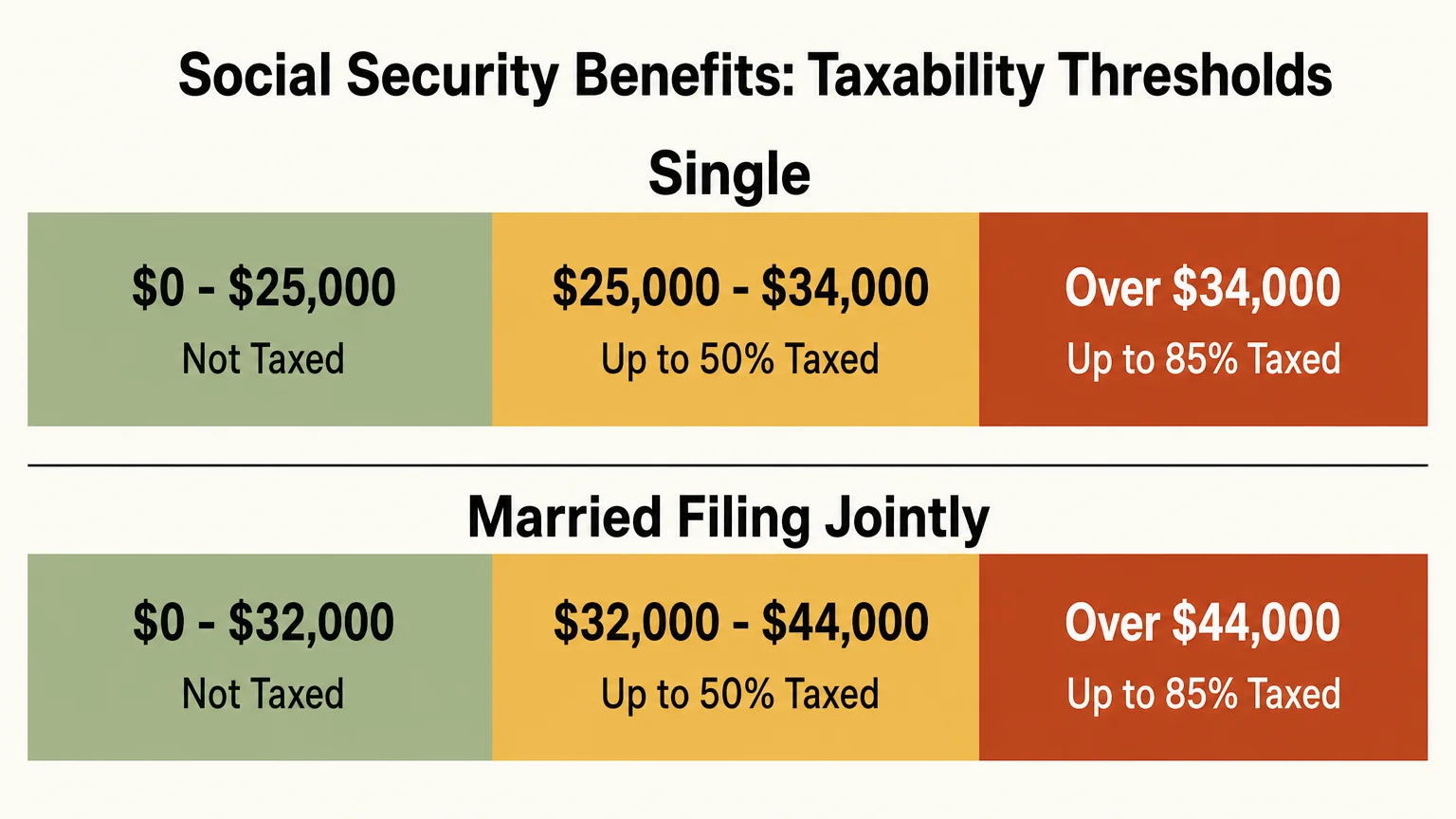

6. Your Benefits Might Trigger Federal Income Tax

Up to 85 percent of your Social Security benefits may be subject to federal income tax, depending on your overall financial picture. The IRS uses a specific formula called “provisional income,” which equals your adjusted gross income, plus any nontaxable interest, plus half of your annual Social Security benefits. If your provisional income lands above $25,000 for a single filer or $32,000 for married couples filing jointly, up to 50 percent of your benefit becomes taxable. If you cross the secondary thresholds of $34,000 for single filers or $44,000 for couples, up to 85 percent becomes taxable. Because these thresholds were established decades ago and are not indexed for inflation, normal cost-of-living increases push more middle-class retirees into this tax bracket every single year.

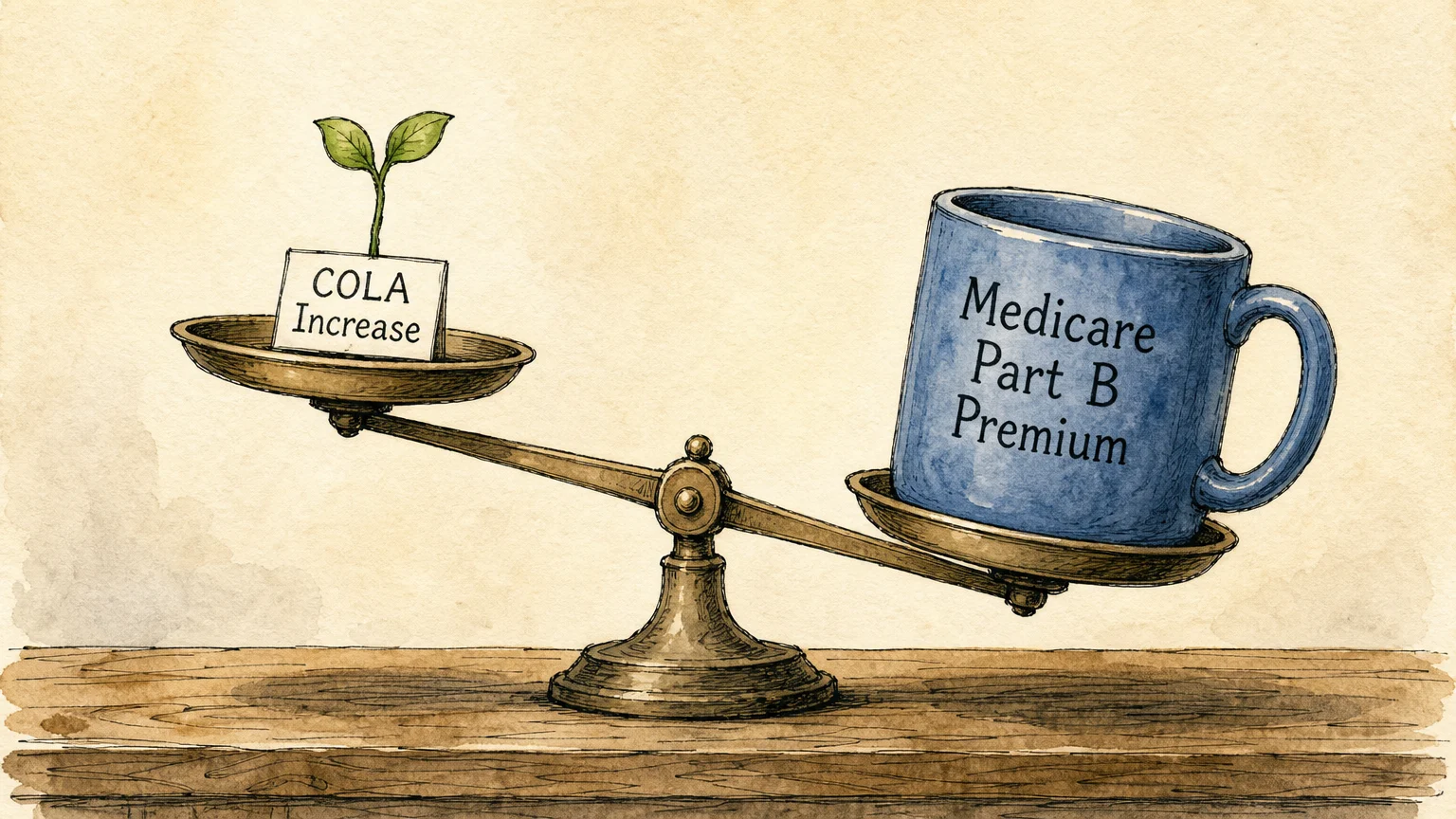

7. Medicare Part B Premiums Often Absorb Your COLA

Most retirees have their Medicare Part B premiums automatically deducted from their monthly Social Security payments before the money ever hits their bank account. Because healthcare costs typically rise faster than general inflation, an increase in Part B premiums can easily consume a significant portion of your annual Social Security COLA. If standard Part B premiums rise sharply in 2026, the net dollar increase you actually see deposited could be much smaller than the headline COLA percentage suggests. Fortunately, a statutory “Hold Harmless” provision protects most beneficiaries from seeing their net Social Security check outright decrease simply due to standard Medicare premium hikes.

8. Spousal Benefits Stop Growing at Full Retirement Age

A non-working or lower-earning spouse can claim a benefit based on the primary earner’s work record. Spousal benefits max out at 50 percent of the primary earner’s FRA benefit amount. However, the rules for spousal benefits differ significantly from primary worker benefits when it comes to delaying your claim. Spousal benefits do not earn delayed retirement credits. Waiting past your own FRA to claim a spousal benefit will not increase the payout percentage. This means there is absolutely zero financial incentive for a spousal-only claimant to delay filing past their Full Retirement Age.

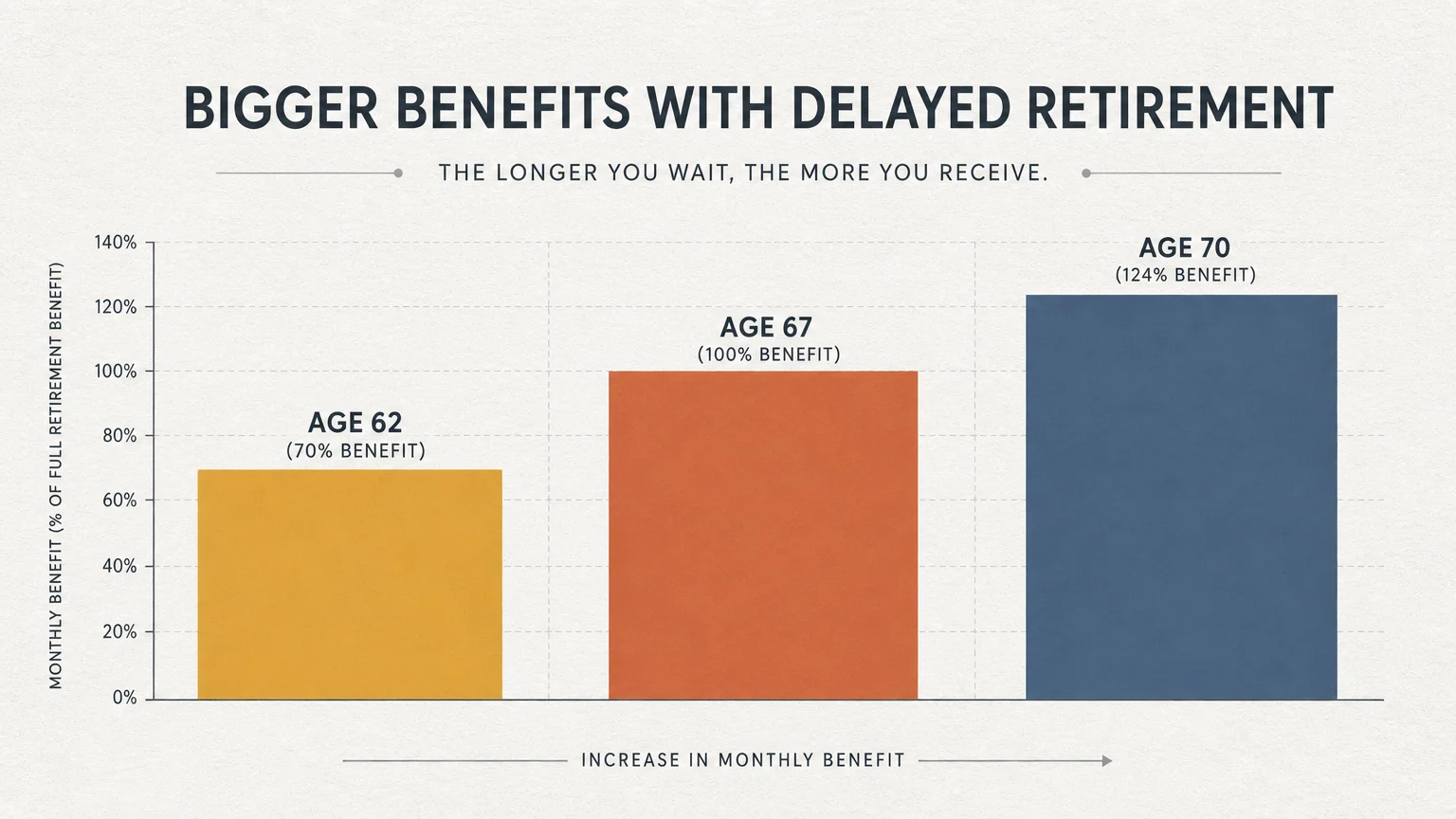

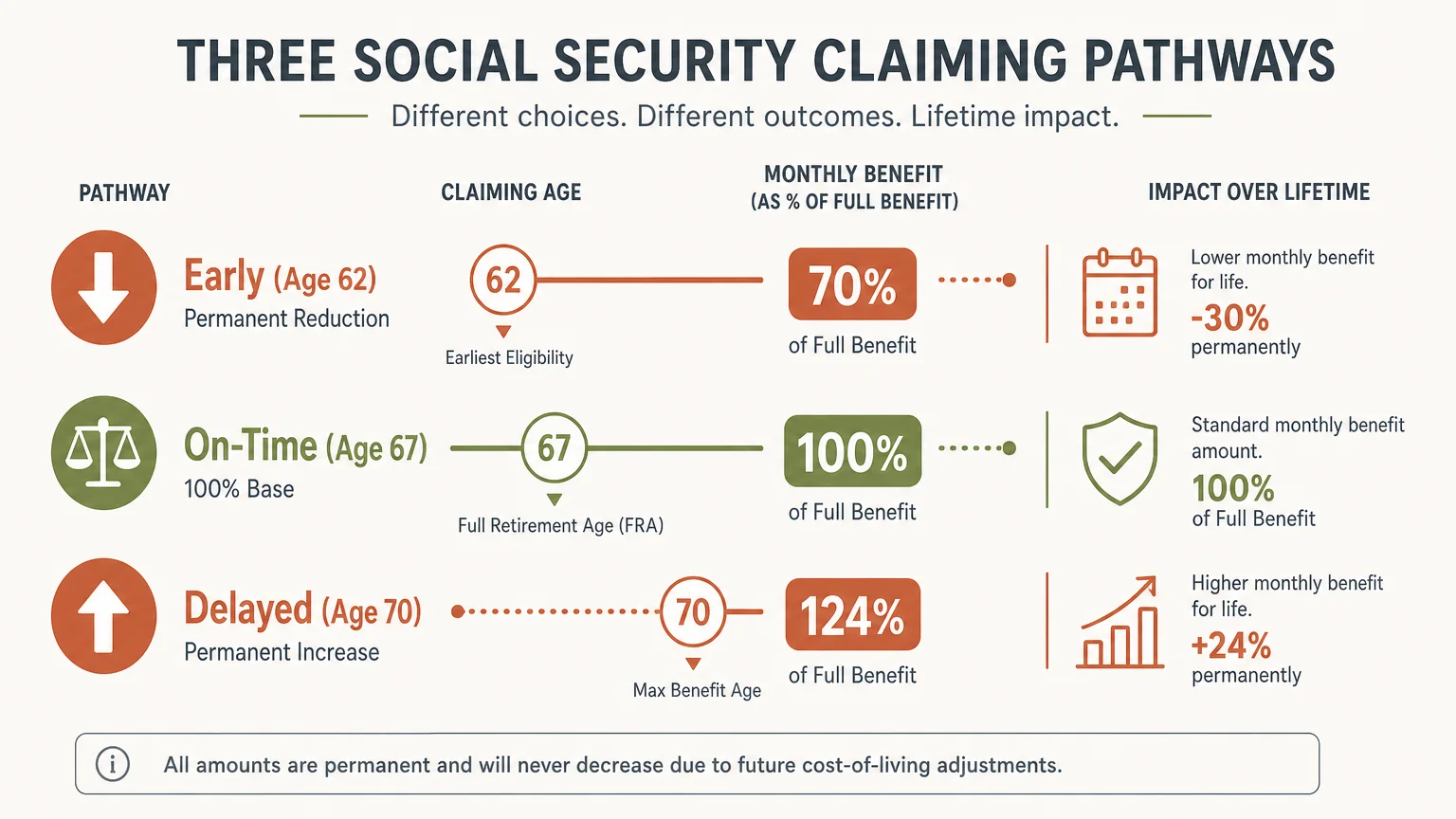

9. Delayed Retirement Credits Max Out at Age 70

You can file for Social Security as early as age 62, but doing so results in a permanently reduced benefit. Conversely, if you wait past your FRA, the government rewards you with delayed retirement credits. These credits increase your monthly payout by 8 percent for every full year you delay. However, this 8 percent annual bonus strictly stops the month you turn 70. Waiting past age 70 leaves free money on the table without generating any further permanent increase to your monthly baseline check.

10. The 12-Month “Do-Over” Rule Offers a Backup Plan

Retirement transitions do not always go as planned, and sometimes retirees regret claiming their benefits early. The Social Security Administration offers a strict, one-time “do-over” option. If you change your mind within 12 months of your original application approval, you can withdraw your claim. The catch is that you must repay every cent you and your family received, including any Medicare premiums that were deducted from your checks. Once repaid in full, your record resets completely, allowing you to claim a higher benefit amount later down the line when you are older.

At a Glance: How Claiming Age Affects Your Benefit

Your claiming age permanently alters your monthly cash flow. Using a hypothetical $2,000 monthly benefit at a Full Retirement Age of 67, here is how filing at different milestones shifts the math:

| Claiming Age | Percentage of FRA Benefit | Hypothetical Monthly Benefit | Best Fit For |

|---|---|---|---|

| Age 62 (Earliest) | 70% | $1,400 | Those needing immediate cash flow, leaving the workforce early, or facing poor health outlooks. |

| Age 67 (FRA) | 100% | $2,000 | Those who want their standard earned benefit and the freedom to work without earnings limits. |

| Age 70 (Maximum) | 124% | $2,480 | Those with longevity in their family history and sufficient personal savings to bridge the gap until 70. |

How to Check Your Personal Numbers

To make concrete decisions, you need to know exactly what the Social Security Administration has on file for your lifetime earnings history. Checking your statement annually is the best way to catch clerical errors that could permanently shortchange your retirement.

- Create an official account: Visit the government’s my Social Security portal to establish your secure profile.

- Review your earnings record: Verify that your taxable earnings for every working year match your past tax returns and W-2s. Missing years will drag down your average.

- Check your estimates: Use the built-in calculators to view your specific projected monthly benefit at age 62, your exact Full Retirement Age, and age 70.

The Bigger Picture

Social Security was designed during the Great Depression to serve as a safety net against severe poverty in old age, not as a primary wealth-building tool or a sole source of income. On average, the program replaces about 40 percent of a typical worker’s pre-retirement income. Financial professionals generally recommend replacing 70 to 80 percent of your working income to maintain your current standard of living in retirement. The growing structural deficits and the fast-approaching 2032 trust fund timeline make it even more critical to build a diversified retirement strategy. Personal savings, 401(k) accounts, IRAs, and investments must pick up the slack to ensure you have a comfortable buffer against future policy changes.

Worth Keeping in Mind

Navigating the complex rules of the program requires vigilance. Consider these potential pitfalls before locking in your strategy:

- Survivor benefits operate on different timelines: If you are a widow or widower, you can claim survivor benefits as early as age 60 (or age 50 if disabled). You also have the flexibility to switch between a survivor benefit and your own retirement benefit later if the math works in your favor.

- Divorce does not necessarily erase benefits: If your marriage lasted at least 10 consecutive years and you remain currently unmarried, you may be entitled to claim benefits based on your ex-spouse’s earnings record. Claiming on their record does not impact their payout or the payout of any current spouse they may have.

- Retiring mid-year has special rules: If you claim benefits in the middle of the year, the standard annual earnings limit can be problematic. Thankfully, the SSA applies a “monthly earnings test” for the remainder of your first calendar year of retirement, meaning you will not be penalized for the high wages you earned before you retired.

When to Get Professional Help

Social Security decisions are largely permanent, and a simple miscalculation can cost a household tens of thousands of dollars over a lifetime. It is wise to consult a fee-only fiduciary financial planner or tax professional if you face any of the following scenarios:

- You own a business: Entrepreneurs need strategic advice on how taking a salary versus owner draws affects their FICA taxes and future benefit calculations.

- You have a pension from a government job: Teachers, police officers, and other public servants who did not pay Social Security taxes may fall under the Windfall Elimination Provision (WEP) or the Government Pension Offset (GPO), which can drastically reduce expected benefits.

- You have a large age gap with your spouse: Couples with significant age differences require specialized claiming strategies to maximize joint lifetime income and protect the younger surviving spouse over the long haul.

Frequently Asked Questions

Will Social Security run out of money completely?

No. Even if the trust funds deplete entirely by 2032, ongoing payroll taxes collected from active workers will continue funding the majority of scheduled benefits. Current projections suggest incoming tax revenue would still cover around 78 percent of scheduled payouts.

Can I pause my benefits if I decide to go back to work?

Yes, but only if you have reached your Full Retirement Age. You can voluntarily suspend your benefits, which allows them to earn the 8 percent delayed retirement credits up to age 70, resulting in a larger monthly check when you eventually resume them.

Are Social Security spousal benefits different from survivor benefits?

Yes, they are calculated very differently. A spousal benefit maxes out at 50 percent of the primary earner’s FRA amount while both spouses are alive. A survivor benefit, however, allows a widow or widower to step into the primary earner’s full benefit, collecting up to 100 percent of what the deceased spouse was receiving.

Your Social Security benefit is one of the most valuable financial assets you will ever own. Taking the time to understand the filing rules, the tax implications, and the broader health of the program ensures you can make informed, confident choices. By tracking your earnings history and planning your claiming age carefully, you can protect your financial stability well into the future.

This article provides general information only. Every reader’s situation is different—what works for others may not be the right fit for you. For personalized guidance on health, legal, or financial matters, consult a qualified professional.

Last updated: May 2026. Rules, prices, and details change—verify current information with official sources before acting on it.