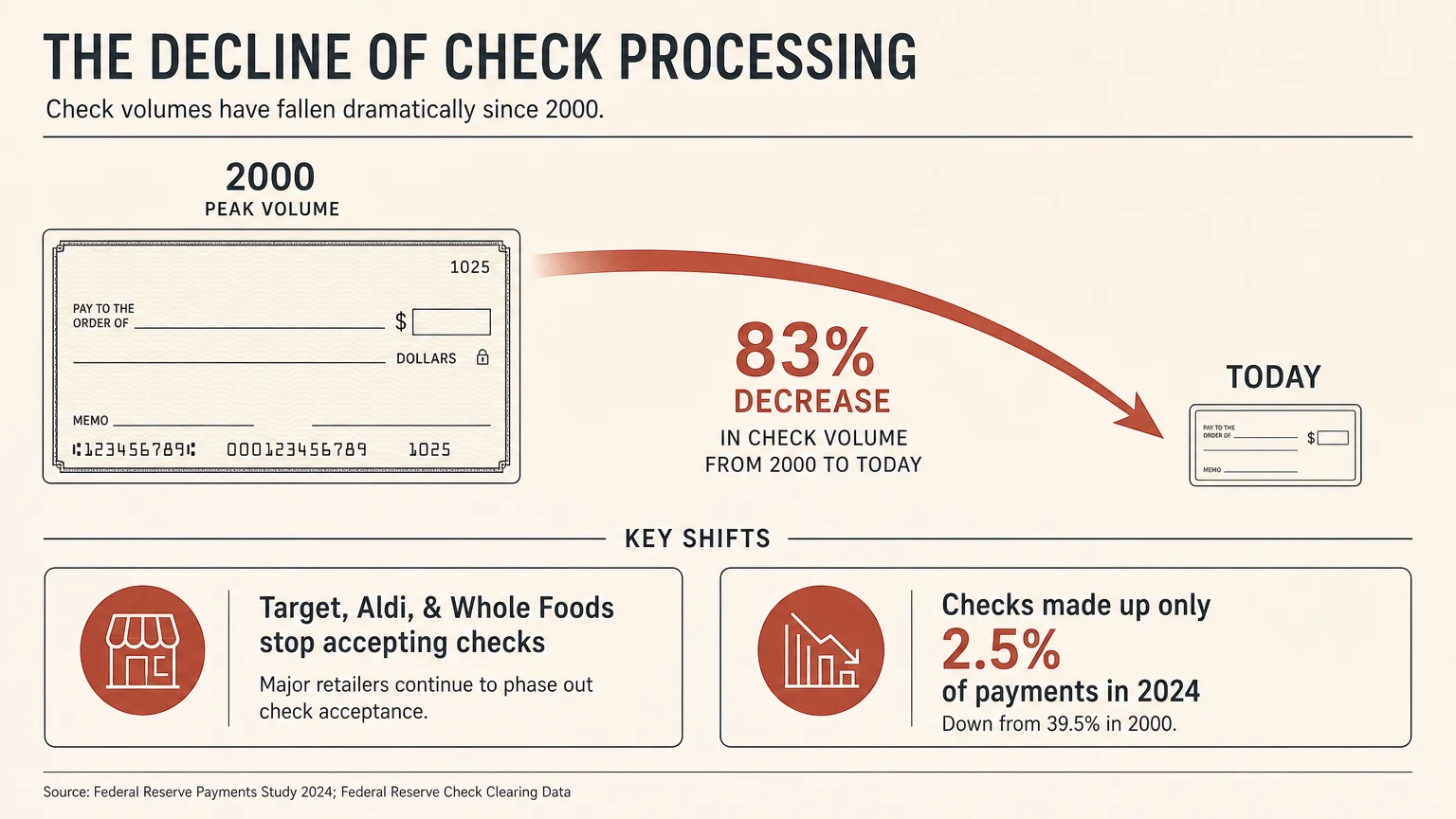

Writing a paper check used to be the default way to pay rent or buy groceries, but that familiar slip of paper is rapidly losing its place in everyday life. Driven by rising processing costs and a staggering surge in mail theft and check fraud, retailers and banks are making checks harder to use. In fact, commercial check volume processed by the Federal Reserve has plummeted by roughly 83% since 2000. Major stores like Target have stopped accepting personal checks entirely, while banks are increasing checkbook fees and extending hold times on deposited funds. If you still rely on a checkbook to manage your monthly budget, adapting to faster, safer digital alternatives is no longer just an option—it is becoming a necessity.

The Essentials

- Retailers are moving on: Major national chains, including Target, Aldi, and Whole Foods, have stopped accepting personal checks at the register.

- Fraud is soaring: Check fraud is a booming criminal enterprise, with banks filing hundreds of thousands of suspicious activity reports annually regarding washed or stolen checks.

- Infrastructure is shrinking: The Federal Reserve is actively evaluating the future of its check-processing services due to aging systems and severely reduced consumer demand.

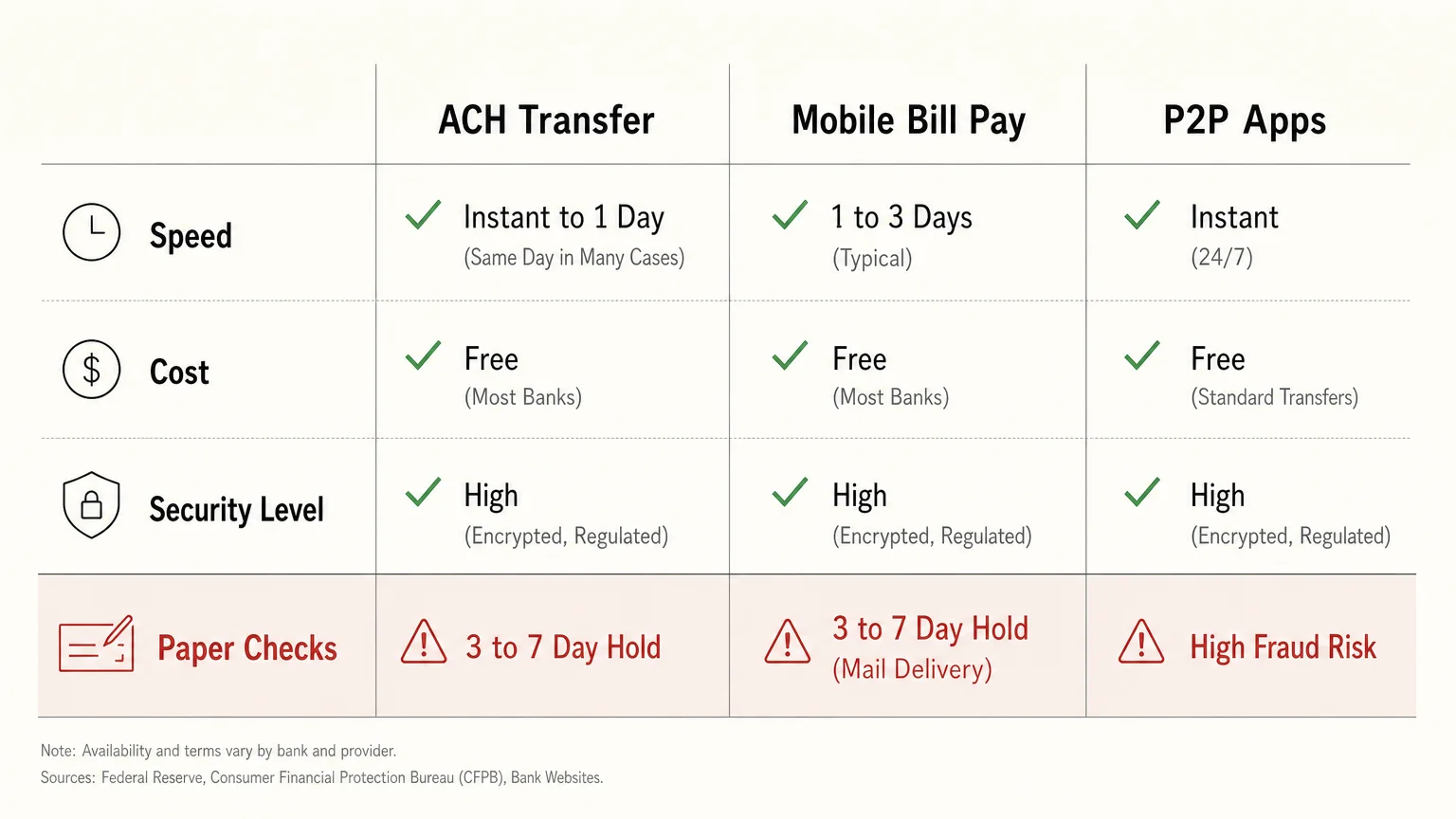

- Digital options are safer and cheaper: ACH transfers, mobile banking bill pay, and peer-to-peer (P2P) payment apps offer faster, more secure ways to move your money without exposing your account details.

The Hidden Costs and Rising Friction of Paper Checks

For decades, checking accounts came with a free box of checks, and banks readily cleared those handwritten slips within a day or two. Today, the landscape looks entirely different. Financial institutions are actively disincentivizing paper checks because they are expensive to process and fraught with risk.

First, consider the direct costs. Many major banks now charge anywhere from $20 to $35 for a standard box of checks. Add in the rising cost of postage stamps, and you are paying a premium just for the privilege of paying your bills. But the hidden costs go far beyond the price of paper and ink.

When you deposit a check today, you are likely to encounter extended hold times. In the past, banks often made funds available the next business day. Now, due to the rampant spike in counterfeit checks, banks frequently place holds of three to seven business days on deposited funds while they wait for the issuing bank to verify the transaction. If you are living paycheck to paycheck or need immediate access to your money, a five-day hold on a deposited check can completely derail your budget and trigger overdraft fees on your other automated payments.

Furthermore, the very infrastructure that supports check processing is shrinking. In late 2025, the Federal Reserve Board requested public input on the future of its check services. The Federal Reserve processes a significant portion of the nation’s commercial checks, but with check usage hitting historic lows, maintaining the aging sorting facilities and transportation networks is becoming financially unviable. As the central bank scales back these operations, the processing of paper checks will inevitably become slower and more expensive for local banks and credit unions—costs that will ultimately be passed down to you.

According to research from the Federal Reserve Bank of Atlanta, checks accounted for just 2.5 percent of consumer payment activity in 2024, a steep drop from 6 percent in 2015. As the volume shrinks, the system becomes less efficient, making your paper check an outlier in a digital financial world.

Why Retailers Are Closing the Register on Checks

If you have stood in a grocery store checkout line recently, you know that speed is the ultimate goal. Retailers have optimized their registers for tap-to-pay cards, digital wallets, and self-checkout kiosks. A customer pulling out a checkbook, writing the date, filling in the amount, and waiting for the cashier to run the paper through a verification machine brings the entire line to a halt.

Because of this friction, corporate retailers are steadily removing the option entirely. In July 2024, Target officially stopped accepting personal checks at checkout, citing extremely low usage volumes and a desire for an efficient checkout experience. Target joins other major grocery chains like Aldi and Whole Foods, which abandoned check acceptance years ago.

For businesses, banning checks is not just about moving the line faster; it is about risk management. When a customer pays with a debit or credit card, the merchant knows instantly whether the transaction is approved. When a customer pays with a personal check, the store assumes the risk that the check might bounce days later due to insufficient funds. Recovering money from a bounced check requires the retailer to pay return fees to their own bank and employ collection agencies to track down the customer.

Additionally, the rise of self-checkout lanes heavily influences this trend. Retailers are dedicating more square footage to automated kiosks, which physically cannot accept or process paper checks. If you plan to shop at major national chains, relying on a checkbook will increasingly force you into a single, understaffed traditional lane—if the store even allows checks at all.

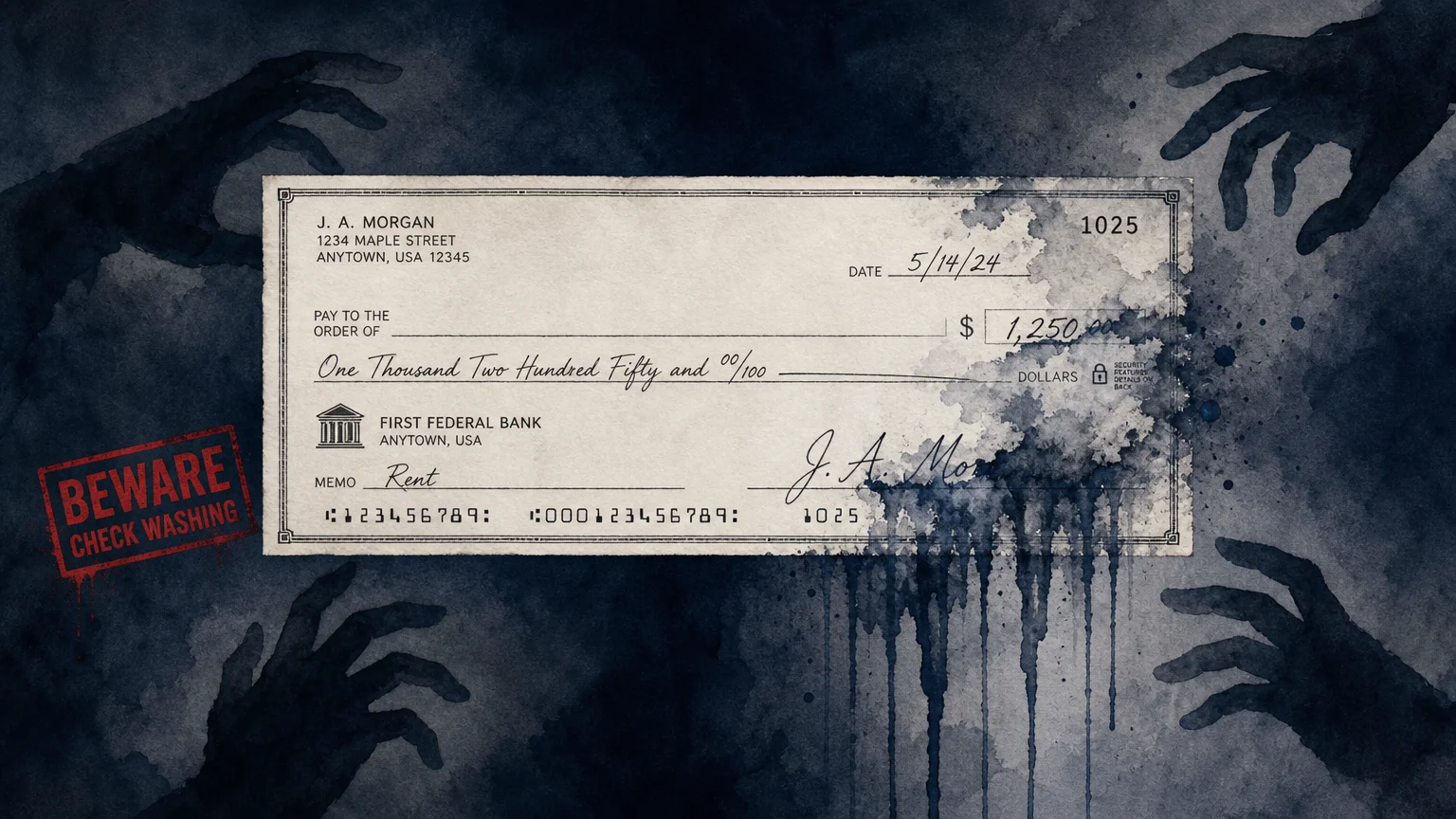

The Fraud Factor: Why the Mail Is No Longer Safe

Perhaps the most urgent reason to reconsider your checkbook is the staggering rise in organized check fraud. Mailing a check to pay a utility bill or send a birthday gift was once considered perfectly safe. Today, doing so exposes you to a significant risk of financial theft.

Thieves target iconic blue United States Postal Service (USPS) collection boxes, often stealing the universal arrow keys carried by postal workers to access the mail inside. Once criminals have their hands on envelopes containing checks, they deploy a technique called check washing. Using common household chemicals, such as nail polish remover or bleach, thieves dissolve the ink used to write the payee’s name and the dollar amount. They leave your signature intact, then rewrite the check to themselves—often for thousands of dollars—and deposit it via a mobile app using a synthetic identity.

The scale of this crime is monumental. According to data published by the Financial Crimes Enforcement Network (FinCEN), financial institutions filed more than 682,000 Suspicious Activity Reports (SARs) related to check fraud in 2024 alone. This represents a massive spike compared to the pre-pandemic era. The crisis has grown so severe that the USPS has publicly advised Americans to avoid leaving checks in standalone mailboxes overnight.

If you become a victim of check fraud, the recovery process is grueling. Unlike fraudulent credit card charges—which can usually be reversed with a single phone call—a washed check results in money actually leaving your checking account. Your bank must launch an investigation, contact the bank where the fraudulent check was deposited, and fight to reclaim the funds. This process can take weeks or even months. During that time, you are out the money, which can lead to bounced rent checks, missed mortgage payments, and severe financial stress.

How to Transition Your Finances to Digital Banking

If you have used checks for decades, switching your entire financial life to a digital format might feel overwhelming. However, breaking the transition into small, manageable steps makes the process straightforward.

First, audit your outgoing payments. Look at your bank statements for the past six months and highlight every instance where you wrote a paper check. Group these payments into categories: fixed monthly bills like rent or a mortgage, variable utility bills like water or electricity, and personal payments like paying a gardener or giving a gift.

For your fixed and variable bills, utilize your bank’s native bill-pay feature. Nearly every bank and credit union offers an online bill-pay portal that allows you to input the company’s name and your account number. Your bank will then electronically send the funds on the date you specify. If the recipient does not accept electronic transfers—such as a small, independent landlord—your bank will print and mail a secure corporate check on your behalf. This protects your personal checking account number and completely hides your signature from potential mail thieves.

For everyday personal transactions, familiarize yourself with peer-to-peer (P2P) payment platforms. If your bank uses Zelle, you can send money instantly to anyone with a US bank account using only their email address or phone number. Setting up automated clearing house (ACH) transfers for your credit card bills guarantees you never miss a due date or pay a late fee because a check was delayed in the mail.

Finally, set up real-time text or email alerts on your checking account. You can program your bank to notify you immediately whenever a withdrawal over a specific amount takes place. This digital vigilance allows you to spot unauthorized activity instantly, rather than waiting for your monthly paper statement to arrive in the mail.

Comparing Your Payment Alternatives

When you put down the checkbook, you need reliable alternatives. Different payment methods serve different purposes, and understanding when to use each will help you avoid unnecessary fees and processing delays.

| Payment Method | Best Used For | Processing Time | Cost |

|---|---|---|---|

| ACH Transfer (Direct Bank-to-Bank) | Paying utility bills, mortgages, and credit card balances. | 1 to 3 business days. | Usually free. |

| Bank Bill Pay | Sending payments to landlords or local businesses without digital portals. | 3 to 5 business days. | Usually free. |

| P2P Apps (Zelle, Venmo, Cash App) | Splitting dinner bills, paying babysitters, or sending small gifts. | Instant or within minutes. | Free for standard transfers (fees apply for credit card funding). |

| Credit or Debit Card | Groceries, retail purchases, and online shopping. | Instant approval. | Free for consumers (merchants cover processing fees). |

| Wire Transfer | Large, time-sensitive purchases like buying a home. | Same day (often within hours). | $15 to $50 per transfer. |

Common Mistakes to Avoid

Transitioning away from paper checks protects your money, but digital banking requires its own set of safety protocols. Avoid these common pitfalls to ensure your funds remain secure:

- Mailing checks from blue collection boxes: If you absolutely must write a paper check, do not drop it in a standalone USPS collection box, especially after the day’s final pickup time. Instead, take the envelope directly inside your local post office and hand it to a clerk, or drop it in the secure interior wall slot.

- Treating P2P apps like checking accounts: Apps like Venmo and Cash App are convenient for transferring funds, but keeping large balances in these apps can be risky. The Consumer Financial Protection Bureau (CFPB) has recently finalized rules to increase federal oversight of popular digital payment apps due to rising fraud complaints. However, funds sitting in a digital wallet may not always carry the same robust FDIC insurance as a traditional bank account. Transfer received funds to your main bank account promptly.

- Sending P2P payments to strangers: Zelle and similar services are explicitly designed for paying people you know and trust. Because the transfers are instantaneous and irreversible, scammers frequently use them to sell fake concert tickets or phantom goods online. If you are buying an item from a stranger, use a credit card with fraud protection.

- Tossing old checks in the trash: If you decide to close an account or stop using checks, never throw blank checks in the garbage. They contain your account number and bank routing number. Shred them thoroughly.

Frequently Asked Questions

Are paper checks going away completely?

Paper checks are unlikely to disappear overnight, but their use is rapidly shrinking into niche business-to-business (B2B) transactions and specific government disbursements. For everyday consumer purchases and retail shopping, checks are actively being phased out by merchants and heavily discouraged by banks.

What is the safest pen to use if I have to write a check?

If you must write a check, financial experts recommend using a gel pen with black or blue ink. Gel ink permeates the fibers of the paper, making it incredibly difficult for thieves to wash the ink away using standard household chemicals. Standard ballpoint pen ink sits on top of the paper and is much easier to erase.

Can my bank refuse to accept a check I want to deposit?

Yes. Banks reserve the right to refuse a check deposit if they suspect the check is fraudulent, altered, or drawn on an account with insufficient funds. Additionally, banks will often reject checks that are made out to multiple parties without proper endorsements or checks that are missing a clear signature.

Is mobile check deposit safe?

Yes, utilizing your bank’s official mobile app to deposit a check is very secure. The image is encrypted and transmitted directly to the bank’s servers, bypassing the physical risks associated with mail transport. Once the check clears, be sure to physically destroy the paper copy to prevent it from falling into the wrong hands.

As the banking industry moves toward instant digital payments, holding onto a paper checkbook offers diminishing returns. By embracing secure digital tools—like automated bill pay, ACH transfers, and peer-to-peer applications—you can streamline your budget, save on unnecessary check-printing fees, and significantly reduce your risk of financial fraud. Transitioning your habits may take a quiet afternoon of updating accounts, but the long-term peace of mind is well worth the effort.

This is general informational content based on widely accepted guidance. Individual results vary. Verify current details—rules, prices, eligibility, regulations—with official sources before making important decisions.

Last updated: June 2026. Rules, prices, and details change—verify current information with official sources before acting on it.