Wall Street analysts spend millions forecasting the next major economic shift, yet the most powerful financial forces of the past few years caught them completely off guard. You do not have to look at trading floors to see where money is moving—you just have to look at your grocery cart. Instead of returning to traditional patterns after recent economic turbulence, Americans rewrote the rules. From older adults re-entering the workforce to homeowners refusing to abandon their historically low mortgage rates, everyday people have driven a massive cultural shift. Here are seven financial trends that defied the experts and how they impact your bottom line.

Why People Are Talking About This

For decades, economists relied on predictable models: when interest rates go up, consumer spending goes down; when inflation cools, people return to their favorite brands. But the economic shocks of the early 2020s permanently altered consumer psychology. Americans faced a bizarre cocktail of soaring living costs, high borrowing rates, and an unexpectedly resilient job market.

Instead of acting exactly as the textbooks predicted, you and millions of others adapted in highly creative ways. People tightened their belts where it mattered most, yet leveraged new tools to maintain their standard of living. This grassroots financial maneuvering created an economy that looks vastly different from what major financial institutions projected. Understanding these shifts is crucial because they highlight practical ways ordinary Americans are successfully navigating a tough financial landscape.

1. “Loud Budgeting” Replaces Quiet Luxury

Social media frequently glorifies wealth, giving rise to trends like “quiet luxury”—the idea of wearing unbranded but wildly expensive clothing to signal status. But a counter-movement took hold and rapidly turned into a real economic force. Enter “loud budgeting.”

Loud budgeting is the unapologetic practice of being highly vocal about your financial boundaries. Instead of making up excuses for skipping an expensive group dinner, you simply tell your friends that you are prioritizing your emergency fund. This transparent approach to money strips away the shame traditionally associated with frugality. It relies on positive peer pressure; when you normalize saying no to overpriced experiences, you give your peers permission to do the same. This cultural shift translates into significant savings, keeping money in your pocket rather than sacrificing it to the fear of missing out.

2. Buy Now, Pay Later Creeps Into the Grocery Aisle

When Buy Now, Pay Later (BNPL) services first exploded, they were largely used to finance fashion hauls, electronics, and luxury exercise bikes. Wall Street viewed BNPL as a modern layaway system for discretionary goods. They did not predict it would become a lifeline for basic necessities.

As food prices climbed, shoppers began splitting their weekly supermarket bills into bi-weekly installments. According to a 2026 survey from LendingTree, 29 percent of BNPL users now use the service to purchase groceries, a sharp increase from previous years. This trend highlights how tight household cash flow has become. While BNPL offers immediate relief at the checkout counter, the Consumer Financial Protection Bureau (CFPB) has warned that it functions as a close substitute for credit cards, complete with the risk of compounding late fees if payments slip through the cracks.

3. The “Golden Handcuff” Renovation Boom

Real estate experts generally assume that as families grow or empty nesters downsize, they will sell their current homes and buy new ones. But the market froze when mortgage rates jumped from roughly 3 percent to over 6 percent.

Homeowners realized that trading up meant sacrificing their historically low interest rates. This created the “golden handcuff” effect. Redfin data showed that the median length of time Americans stay in their homes climbed to 12 years by 2025. Instead of moving, you are much more likely to stay put and renovate. Basements are becoming home offices, and outdated kitchens are getting facelifts.

“The ‘golden handcuff’ effect has fundamentally altered the housing market. By refusing to surrender their low mortgage rates, homeowners have inadvertently triggered a localized boom in the renovation and remodeling sectors.”

This refusal to move choked off housing inventory and sparked ongoing demand for local contractors, fundamentally altering the real estate cycle.

4. Store Brands Permanently Defeat Brand Loyalty

During periods of high inflation, consumers typically trade down to generic grocery items to save money. Historically, once prices stabilize or wages catch up, shoppers return to their familiar name brands. Wall Street expected the same rebound—but it never happened.

Retailers invested heavily in the quality and packaging of their private-label goods. Store brands no longer feel like a sacrifice; in many cases, they are manufactured in the exact same facilities as the national brands. Private label retail sales in the United States reached a record $282.8 billion in 2025, capturing an impressive 23.5 percent of total unit share. Shoppers traded down for the price, but they stayed for the quality, dealing a permanent blow to corporate brand loyalty.

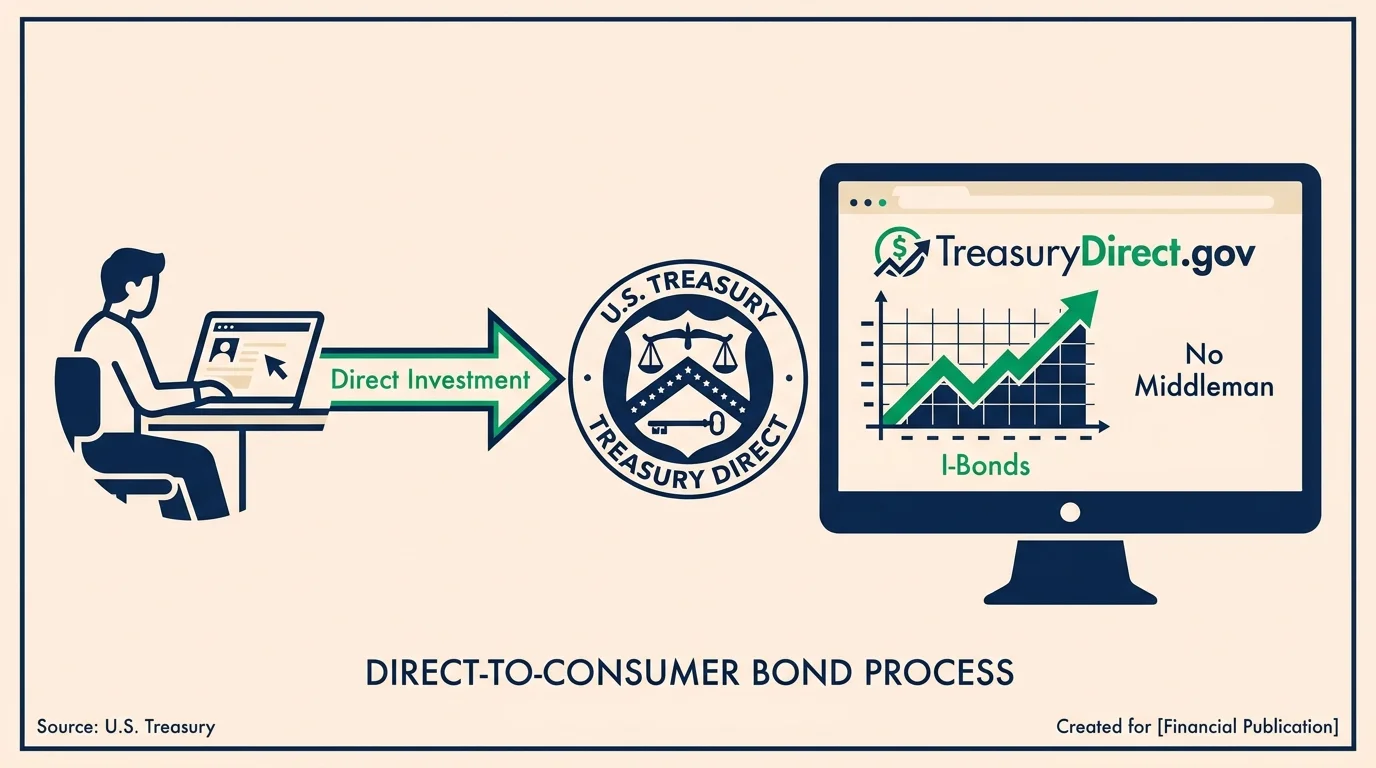

5. The Direct-to-Consumer Government Bond Rush

For years, the U.S. government’s retail bond website, TreasuryDirect, was a sleepy platform utilized mostly by financial nerds. Wall Street assumes retail investors will route their money through mutual funds or wealth managers. But when inflation spiked, the average American bypassed the middlemen entirely.

Drawn by the massive yields on Series I Savings Bonds and short-term Treasury bills, millions of people took their cash straight to the source. During the height of the inflation surge, the platform saw nearly 3 million new accounts open in a single year, representing an astronomical 543 percent increase. This DIY approach to fixed-income investing proved that budget-conscious Americans are more than capable of executing sophisticated yield-chasing strategies without paying management fees.

6. The “Un-Retirement” Wave

The traditional retirement model implies a clean break from the workforce. When the pandemic hit, millions of older adults retired early, leading economists to declare a permanent shrinking of the labor force. However, inflation and rising healthcare costs forced a rapid reversal.

The trend of “un-retirement” caught labor analysts off guard. A 2026 survey from AARP found that 48 percent of older adults re-entering the workforce did so primarily to make money, driven by the persistent high cost of living. Whether picking up part-time consulting gigs, working in retail, or monetizing hobbies, older Americans are redefining what the golden years look like out of both economic necessity and a desire for structure.

7. The Stubborn Reign of High-Yield Savings

When the Federal Reserve began aggressively raising interest rates, bank savings accounts finally started paying meaningful interest. Wall Street assumed that once the stock market rebounded, this cash would flood right back into equities.

Instead, everyday savers realized that earning a guaranteed return on their emergency funds was incredibly attractive. Rather than shifting all their liquidity back into volatile stocks, Americans treated high-yield savings accounts and certificates of deposit (CDs) as core, long-term components of their portfolios. Cash transformed from a stagnant holding pen into a reliable income generator.

Things to Watch Out For

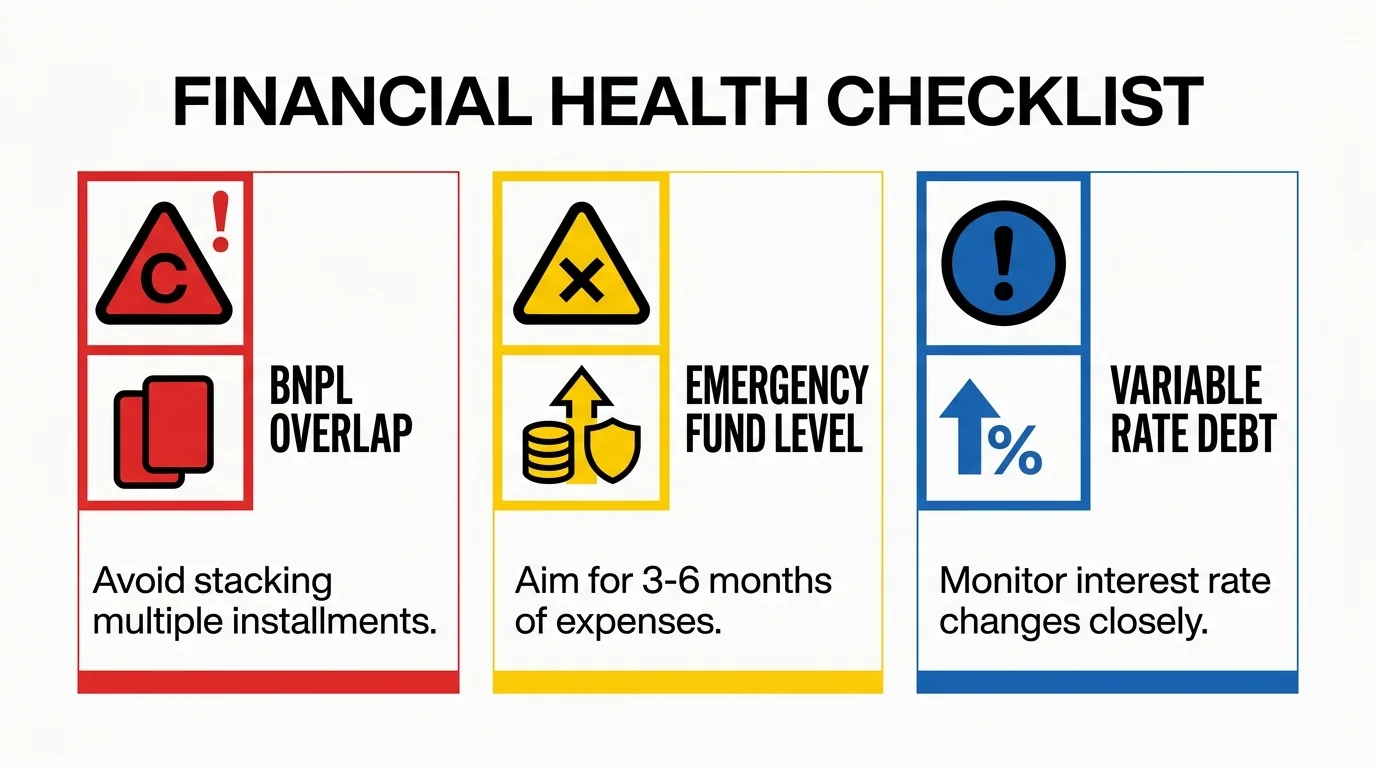

While these grassroots trends showcase financial resilience, they come with their own set of modern pitfalls. If you are participating in these shifts, keep an eye on these specific scenarios:

- BNPL Debt Stacking: Using Buy Now, Pay Later for groceries at one store, clothes at another, and car parts at a third creates multiple overlapping payment schedules. It is dangerously easy to overdraft your checking account if four different auto-drafts hit on the same day.

- Over-Renovating Your Home: The golden handcuff effect might push you to renovate, but be careful not to price your home out of its own neighborhood. Sinking $100,000 into a luxury kitchen in a neighborhood of modest starter homes will not yield a dollar-for-dollar return if you eventually sell.

- Treasury Tax Surprises: While buying T-bills and I-Bonds directly from the government is a smart move, remember that the interest earned is subject to federal income tax (though exempt from state and local taxes). Failing to account for this at tax time can result in an unexpected bill.

- The Un-Retirement Social Security Trap: If you claim Social Security before your full retirement age and decide to go back to work, your benefits could be temporarily reduced if your earnings exceed the annual limit.

When DIY Isn’t Enough

Managing your money through grassroots trends is empowering, but some financial crossroads require a deeper level of expertise. You should strongly consider consulting a licensed professional in these specific situations:

| Equity Option | Best For | Impact on Current Mortgage Rate |

|---|---|---|

| Home Equity Loan | One-time, fixed-cost renovation projects | None. Your original primary mortgage stays intact. |

| HELOC | Ongoing projects with variable costs over time | None. Acts as a secondary revolving line of credit. |

| Cash-Out Refinance | Consolidating heavy debt alongside renovations | Replaces your entire mortgage with today’s prevailing rates. |

- Navigating Work and Medicare: If you are un-retiring and your new employer offers health insurance, the rules regarding how it interacts with Medicare Parts A and B are incredibly complex. A misstep can lead to lifetime late-enrollment penalties.

- Accessing Major Home Equity: If you are staying put and need to fund a renovation, deciding between a cash-out refinance, a Home Equity Loan, or a Home Equity Line of Credit (HELOC) requires running long-term amortization math. A fiduciary financial advisor can help you protect your underlying mortgage rate.

- Transitioning Heavy Cash Positions: If you have hoarded cash in a high-yield savings account but are falling behind on your retirement goals, you face inflation risk. A professional can help you build a bridge from safe, short-term cash to diversified, long-term investments.

Frequently Asked Questions

Does Buy Now, Pay Later affect my credit score?

Traditionally, most BNPL providers did not report on-time payments to the major credit bureaus, meaning the loans did not build your credit. However, if you miss a payment or default, the provider may send the account to collections, which will severely damage your credit score.

Are store brands actually manufactured by the same companies as name brands?

In many cases, yes. Major food manufacturers often produce private-label goods on the same assembly lines as their premium products, simply swapping the packaging at the end of the run. The ingredients might have minor variations, but the core quality is frequently identical.

How do I start loud budgeting with my friends?

Start small. The next time a friend suggests an expensive outing, confidently say, “I am focusing on saving for a house right now, so I am skipping high-priced dinners. Would you want to grab coffee or go for a walk instead?” Framing the refusal around a positive goal makes the conversation empowering rather than awkward.

The smartest financial moves rarely make the evening news. While Wall Street obsesses over corporate earnings and macroeconomic models, the real economy is driven by the quiet, practical decisions you make every day. Whether you are actively choosing generic brands, maximizing a high-yield savings account, or openly setting financial boundaries with your friends, these trends prove that everyday Americans possess an incredible ability to adapt to changing times.

As you navigate your own budget, remember that you do not need to follow traditional scripts to succeed. Take advantage of the tools that work for your specific situation, and ignore the financial noise that doesn’t serve you. The information here is meant for educational purposes. Specific circumstances—including health conditions, finances, location, and goals—may require different approaches. When in doubt, consult a licensed professional or check official sources directly.

Last updated: May 2026. Rules, prices, and details change—verify current information with official sources before acting on it.