Higher grocery prices take an oversized bite out of your budget when you rely on a fixed income, making the inflation numbers for 2026 a crucial factor for your financial health. While the 2026 Social Security cost-of-living adjustment provides a 2.8% boost—adding about $56 a month to the average retirement check—navigating the supermarket still requires strict discipline. The U.S. Department of Agriculture projects that food-at-home prices will rise 2.4% this year. That sounds moderate on paper, but sharp spikes in specific staples like beef quickly eat up those modest Social Security gains. To protect your retirement savings, you must adjust how you shop, rethink where you buy, and leverage age-specific assistance rules.

The 2026 Grocery Forecast: What the Numbers Actually Say

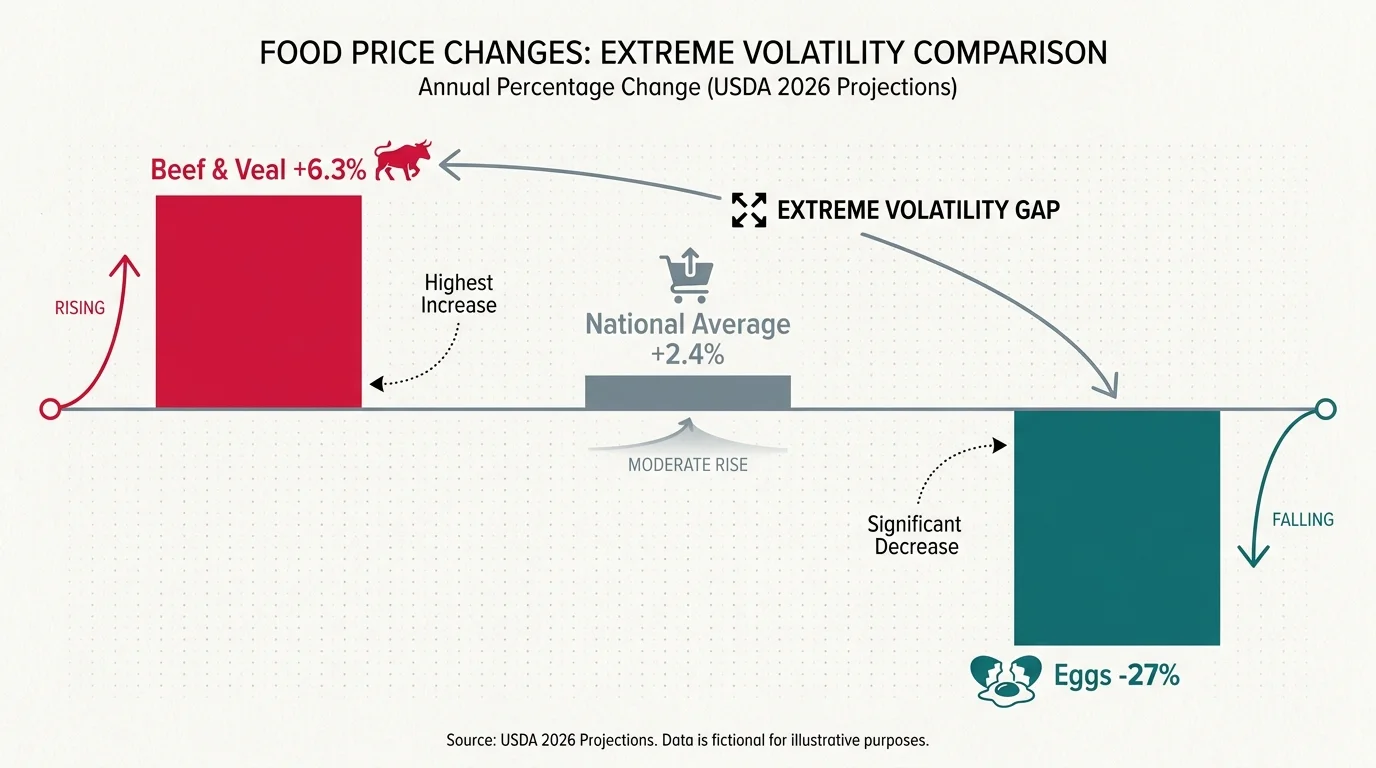

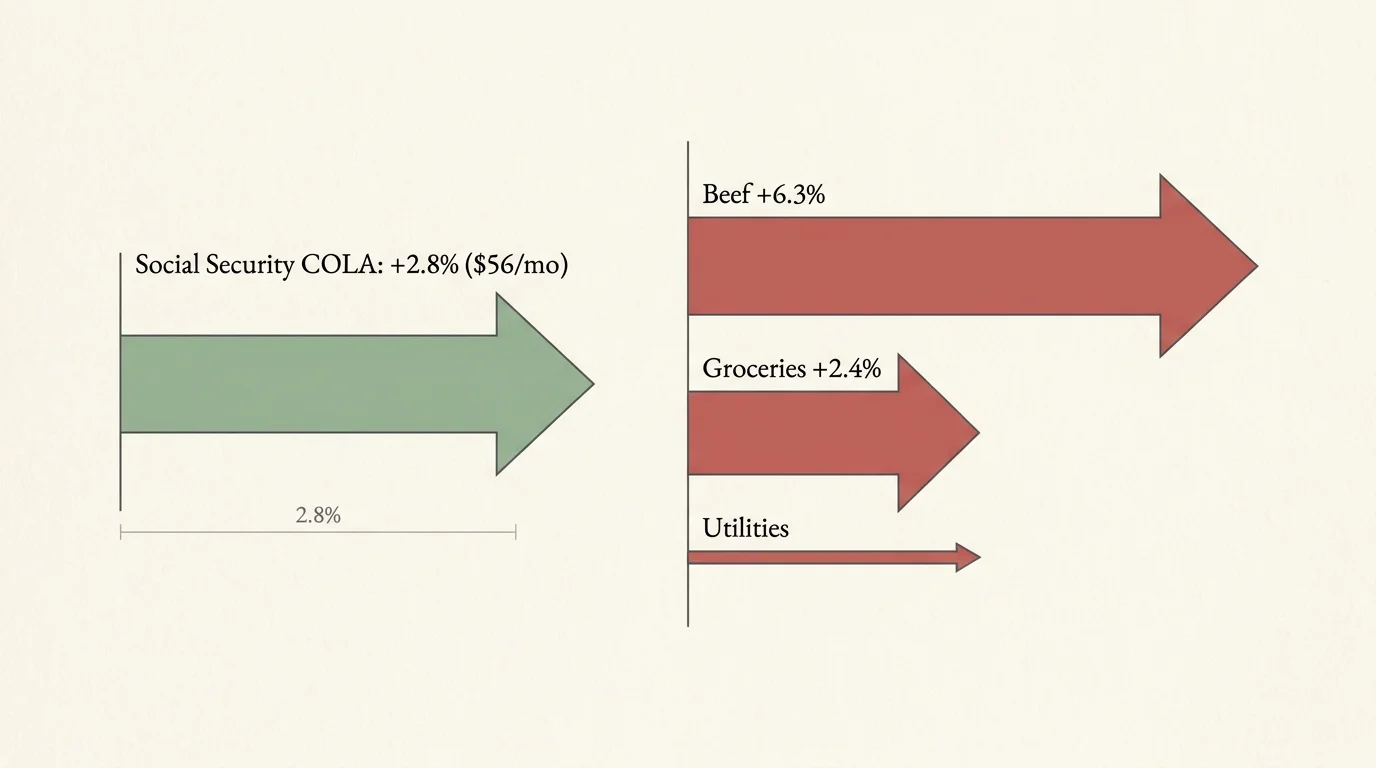

The grocery store continues to serve as the front line for inflation in 2026. According to the USDA Economic Research Service, food-at-home prices are expected to rise by 2.4% this year. On the surface, this figure represents a return to a more manageable baseline, falling slightly below the 20-year historical average of 2.6%. However, looking only at the broad national average disguises the extreme volatility happening in individual grocery aisles.

Beef and veal prices stand out as significant budget disruptors. The USDA forecasts a 6.3% increase in beef costs for 2026, driven heavily by tight cattle supplies and consistently firm consumer demand. If your weekly meal plan relies heavily on red meat, your personal inflation rate will outpace the national average. Sugar, sweets, fresh vegetables, and nonalcoholic beverages are also projected to see above-average price hikes this year, further pressuring the standard grocery cart.

Conversely, genuine relief is appearing in other sections of the supermarket. Egg prices, which experienced historic and highly publicized spikes earlier in the decade, are moving in the opposite direction. The USDA predicts egg prices will drop by more than 27% in 2026 as avian flu pressures ease and flock production normalizes. Dairy products are also expected to see mild price declines. For a retiree carefully tracking every dollar, this uneven inflation landscape dictates exactly where you should spend your money and where you should pull back.

The Growing Gap Between Groceries and Restaurants

If you regularly rely on restaurants, local diners, or takeout to supplement your weekly meals, the inflation hit feels much harder. While grocery inflation is moderating to 2.4%, the USDA predicts that food-away-from-home prices will rise by 3.6% in 2026. This rate sits above the 20-year historical average and highlights a persistent trend: dining out is becoming a luxury rather than a routine convenience.

Restaurants are currently fighting a multi-front battle against rising costs. They must absorb higher expenses for labor, commercial rent, utilities, and commercial insurance, passing those compounded costs directly to the consumer through higher menu prices and hidden service fees. What used to be a simple $15 lunch can quickly escalate past $22 once taxes, tips, and surcharges are factored into the final bill.

For a retiree living on a strict budget, replacing just two restaurant dinners a week with home-cooked meals can easily save hundreds of dollars a month. Those savings completely offset the 2.4% rise in grocery costs. Shifting your social habits from meeting friends at a restaurant to hosting a potluck or coffee at home acts as an immediate, highly effective defense mechanism against 2026’s economic pressures.

How the 2026 COLA Measures Up to the Checkout Aisle

Every October, the Social Security Administration announces the cost-of-living adjustment (COLA) that takes effect the following January. For 2026, beneficiaries received a 2.8% increase. In practical terms, this adjustment added approximately $56 per month to the average retirement benefit.

Comparing the 2.8% COLA directly to the 2.4% grocery inflation rate makes it look like retirees have a slight edge. But percentages do not buy groceries—raw dollars do. When you factor in the rising costs of property taxes, homeowners insurance, and Medicare premiums, that extra $56 must stretch across multiple expanding categories. It is rarely enough to cover the actual dollar increases across your entire household budget.

Furthermore, older adults spend a disproportionately large share of their income on essentials. Data from the U.S. Bureau of Labor Statistics shows that households aged 65 and older routinely allocate greater percentages of their fixed budgets to healthcare and food at home than younger demographics. Because you spend a larger piece of your pie on food, a bump in grocery prices hurts you more than it hurts a mid-career professional.

To highlight how grocery expenses vary based on shopping habits, consider the following estimates for a monthly food budget for an individual over 65 in 2026:

| Budget Level | Estimated Monthly Cost (Single Adult) | Shopping Style |

|---|---|---|

| Thrifty | $250 – $300 | Strict meal planning; heavily relies on sales, generic brands, and raw ingredients. |

| Low-Cost | $320 – $400 | Moderate flexibility; includes some convenience foods and occasional name brands. |

| Moderate-Cost | $410 – $500 | Wider variety of fresh meats, out-of-season produce, and premium brands. |

| Liberal | $520+ | Minimal price-checking; high consumption of fresh seafood, premium cuts of meat, and specialty items. |

What This Means for You

A shift in grocery prices demands an immediate response in your household spending. Unlike fixed mortgage payments or predictable utility averages, food costs are fluid; they change weekly based on supply chains, international tariffs, and even weather patterns. Because they fluctuate so frequently, your grocery budget requires continuous monitoring.

If you refuse to adjust your shopping habits to account for these 2026 price changes, the compounded effect of higher food costs will slowly erode your financial margin of error. You may find yourself forced to pull more money from your retirement accounts than you planned, or worse, carrying high-interest balances on your credit cards to cover basic living expenses. Maintaining your financial independence requires treating your grocery cart as a core component of your retirement portfolio—one that you must actively manage and optimize.

Actionable Strategies to Defend Your Food Budget

Beating inflation at the supermarket does not require extreme couponing, driving to five different stores, or adopting a miserable diet. Instead, it relies on strategic swaps and a solid understanding of retail pricing mechanics. Implementing just a few targeted changes can drop your monthly food spending by 10% to 15%.

- Substitute expensive proteins: With beef prices climbing aggressively in 2026, pivot to more cost-effective alternatives. Poultry, pork, beans, lentils, and canned fish offer excellent nutrition without the premium price tag. If you prefer red meat, switch from premium steaks to larger, cheaper cuts like chuck roast, and use a slow cooker to tenderize the meat over several hours.

- Maximize senior discount days: Many regional grocery chains offer a 5% to 10% discount on specific days of the month for shoppers over a certain age (often 55 or 60). Schedule your major restocking trips—especially for expensive non-perishable staples, olive oil, and cleaning supplies—exclusively on these designated days.

- Buy produce in season or frozen: Transporting out-of-season fruit across the hemisphere drives up the retail price at your local store. Stick to apples and root vegetables in the winter, and berries in the summer. Alternatively, buy frozen produce; these vegetables are picked at peak ripeness and flash-frozen, locking in nutrients at a fraction of the cost of fresh out-of-season items.

- Avoid the drugstore trap: Picking up a gallon of milk or a box of cereal at the pharmacy while waiting for a prescription is undeniably convenient, but drugstores notoriously mark up their grocery items. Plan your food purchases for dedicated grocery stores or wholesale clubs to avoid paying the convenience premium.

- Audit your receipts immediately: Checkout scanners are not infallible. Sales prices, bulk discounts, and digital coupons frequently fail to register in the computer system. Reviewing your receipt before leaving the store ensures you do not overpay due to a technical glitch, allowing you to address the error at the customer service desk immediately.

Leveraging Technology for the Checkout Aisle

Many older adults naturally shy away from using mobile apps to manage their groceries, preferring physical coupons and printed circulars. However, the retail industry has fundamentally shifted; supermarkets now reserve their absolute best discounts for their digital platforms. Ignoring these tools means you are subsidizing the discounts of more tech-savvy shoppers.

Start by downloading the official app for the primary grocery store you frequent. Most modern supermarket apps feature digital coupons that you can “clip” with a single tap. Once clipped, these discounts automatically apply to your total when you enter your phone number at the checkout register. You do not need to print anything or hand the cashier a stack of paper.

Beyond the store’s own app, consider third-party cash-back applications. These platforms allow you to take a photo of your receipt after you shop; the app then scans the receipt for qualifying items and deposits a small amount of cash back into your account. Over the course of a year, these small digital rebates can easily add up to enough money to cover a month’s worth of groceries.

Unlocking Hidden Food Assistance: The $35 Medical Deduction

If higher prices are squeezing your budget beyond what simple substitutions and digital coupons can fix, it is time to look at federal programs. The Supplemental Nutrition Assistance Program (SNAP) is not just for young families; millions of older adults qualify but never apply because they assume the rules exclude them.

The USDA Food and Nutrition Service maintains specific, highly favorable rules for households with a member aged 60 or older. First, older adults face a less restrictive income test, generally qualifying based on net income rather than the strict gross income limits applied to younger applicants. Second, the resource limits are higher. In 2026, households with an individual aged 60 or older can have up to $4,500 in countable resources (like checking and savings accounts) while still remaining eligible for assistance. Importantly, your primary residence and most retirement accounts generally do not count toward this $4,500 limit.

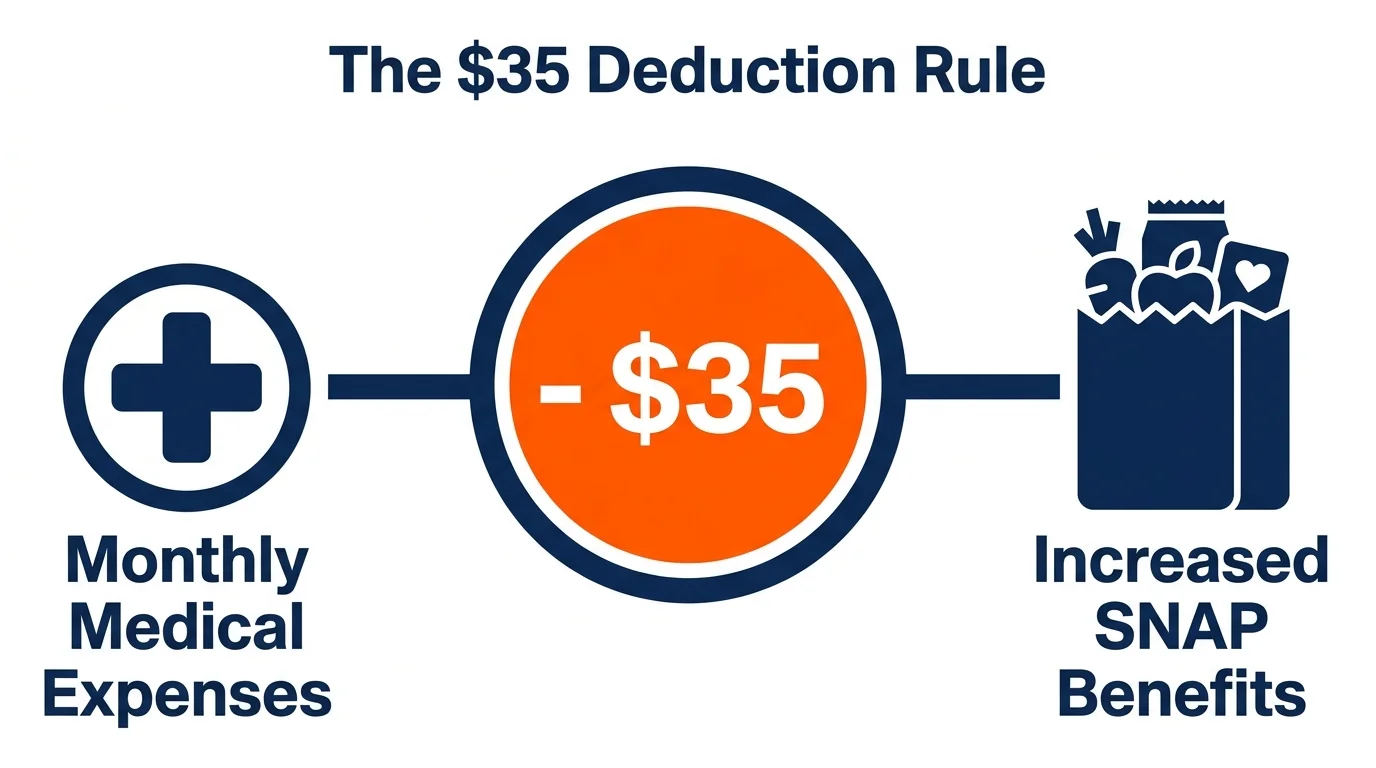

The most powerful—and most overlooked—tool for seniors applying for SNAP is the excess medical expense deduction. If you are 60 or older and have out-of-pocket medical expenses that exceed $35 per month, you can deduct those costs from your income when calculating your SNAP eligibility. This effectively lowers your “income” in the eyes of the government, resulting in a significantly higher monthly food benefit.

Qualifying out-of-pocket medical costs include a wide range of necessities: Medicare premiums, prescription drug copayments, over-the-counter medications approved by a doctor, dental care, dentures, hearing aids, and even the cost of transportation or mileage to medical appointments. Despite the massive financial benefit this deduction provides, federal estimates consistently show that a very small percentage of eligible older adults actually claim it on their applications.

What Can Go Wrong

Navigating a volatile grocery market introduces several budget traps that can quickly drain your wallet. Watch out for these specific pitfalls as you adjust your shopping routines:

- Falling for the bulk illusion: Buying a massive container of perishable food seems like a brilliant financial move until half of it spoils in your refrigerator. Food waste destroys any per-unit savings you gained at the register. Restrict your bulk buying to dry goods, paper products, and meats you can portion and freeze immediately.

- Self-disqualifying for SNAP: Many retirees incorrectly assume that owning a home, driving a decent car, or having a small pension automatically disqualifies them from food assistance. Because they never bother to apply, they leave hundreds of dollars in grocery benefits on the table every month. Let the state agency make the final determination.

- Shopping without a list: Grocery stores are meticulously engineered to encourage impulse buying, from the smell of the bakery near the entrance to the placement of high-margin items at eye level. Entering a supermarket without a concrete, written meal plan almost guarantees you will spend more than you intended.

- Chasing sales across town: Driving to three different supermarkets to save fifty cents on a dozen eggs or a dollar on coffee wastes time and fuel. The cost of gas and wear-and-tear on your vehicle will almost always erase your checkout savings. Stick to one or two stores along your normal driving route.

Where Outside Advice Pays Off

Managing your finances during periods of persistent inflation sometimes requires bringing in a professional. Consider seeking outside help in these specific scenarios:

- Evaluating benefit programs: A benefits counselor at your local Area Agency on Aging can assess your specific financial situation in detail. They understand the nuances of the $35 medical deduction and can help you navigate the complex paperwork for SNAP, the Medicare Savings Program, and local utility assistance.

- Managing strict dietary restrictions: If your doctor prescribes a specific diet—such as a low-sodium regimen for heart health or a diabetic-friendly meal plan—it can initially seem prohibitively expensive. A registered dietitian can teach you how to meet your nutritional requirements using affordable, everyday ingredients without relying on pricey specialty health foods.

- Adjusting retirement withdrawal rates: If rising living expenses are forcing you to pull more cash from your IRA or 401(k) just to cover groceries and utilities, a certified financial planner can help. They will recalibrate your withdrawal strategy and tax withholdings to ensure you do not deplete your nest egg prematurely during inflationary periods.

You have control over how you handle the 2026 grocery landscape. By tracking what you spend, adjusting your shopping habits to avoid high-inflation items like beef, and utilizing all the age-specific resources available to older adults, you can successfully protect your retirement budget from the checkout aisle.

The information here is meant for educational purposes. Specific circumstances—including health conditions, finances, location, and goals—may require different approaches. When in doubt, consult a licensed professional or check official sources directly.

Last updated: May 2026. Rules, prices, and details change—verify current information with official sources before acting on it.