For years, taxpayers have been bracing for the dreaded 2026 “sunset” of the Tax Cuts and Jobs Act, expecting smaller deductions and higher tax brackets. Instead, the passage of the One Big Beautiful Bill Act (OBBBA) in mid-2025 permanently locked in those lower rates and introduced sweeping new deductions that completely reshape your tax strategy for 2026. Rather than losing benefits, millions of middle-class filers will now see an expanded standard deduction, a larger child tax credit, and brand-new write-offs for overtime pay, tipped income, and auto loan interest. As you plan your finances for the year ahead, understanding how these updated rules affect your paycheck and your eventual tax return is the easiest way to keep more money in your pocket.

The Standard Deduction Gets Bigger (and Permanent)

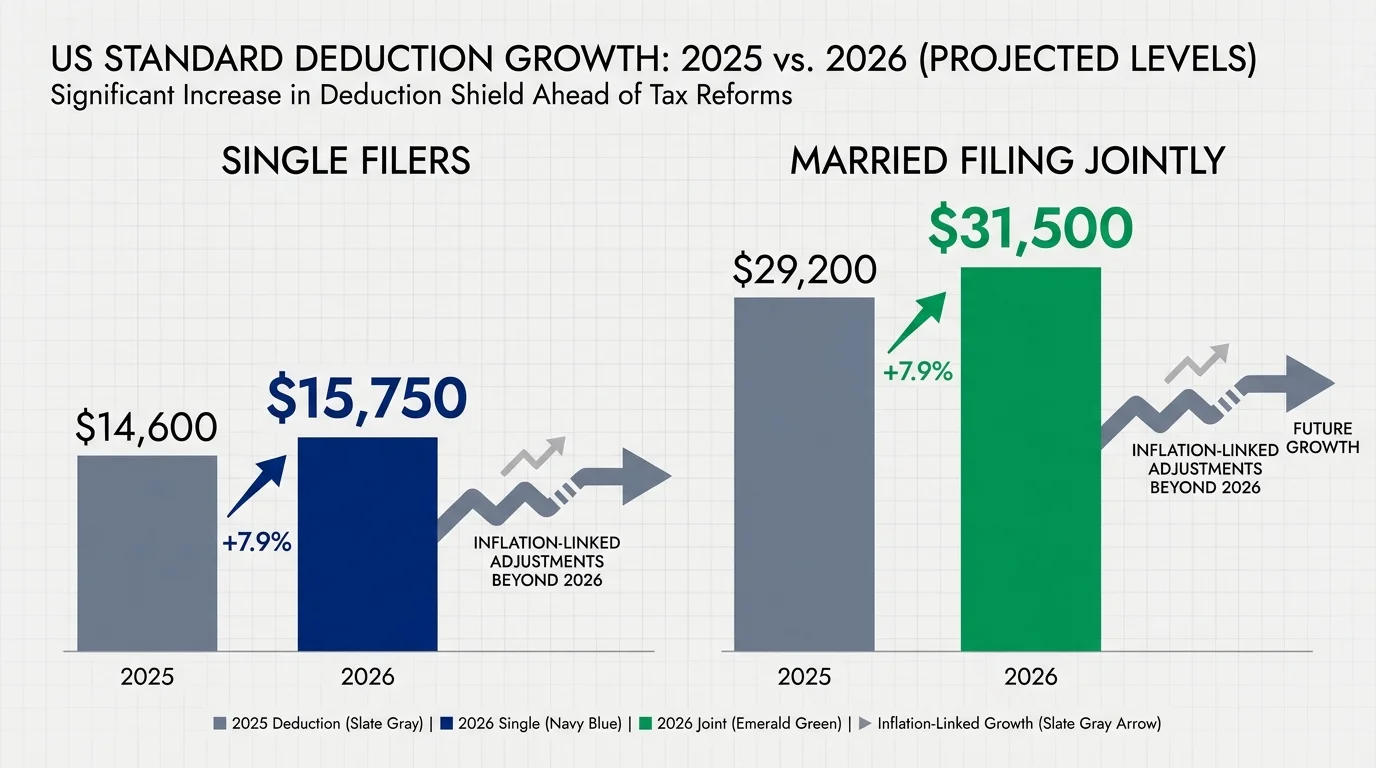

When the tax code was overhauled in 2017, lawmakers roughly doubled the standard deduction, drastically simplifying tax season for the majority of Americans who no longer needed to meticulously track receipts to itemize their deductions. However, that elevated baseline was strictly temporary and scheduled to revert to pre-2018 levels at the end of 2025. This would have forced millions back into the complicated process of itemizing just to avoid a massive tax hike.

The new legislation changes course entirely. It not only rescues the standard deduction from shrinking but pushes it even higher. For the 2026 tax year, the baseline standard deduction climbs to $15,750 for single filers and $31,500 for married couples filing jointly. Even better, the government made these elevated figures permanent and tied them to inflation.

This means your tax-free baseline will automatically adjust upward in future years to keep pace with the rising cost of living. If you and your spouse earn a combined $100,000 in 2026, the first $31,500 of your income is entirely shielded from federal income tax before you even calculate a single specific write-off. This structural permanence offers immense peace of mind; you can project your household budget years into the future without fearing an arbitrary drop in your tax shield.

Income Tax Brackets Escape the 2026 Spike

Perhaps the most highly anticipated shift for 2026 was the return of the old, higher income tax brackets. Without congressional intervention, the top marginal tax rate was scheduled to jump from 37% back to 39.6%, while middle-class brackets were set to compress and increase simultaneously.

Instead, the current favorable tax brackets have been permanently cemented into law. The federal income tax system will retain its seven-tier structure with rates locked at 10%, 12%, 22%, 24%, 32%, 35%, and 37%. Because the tax system operates on marginal rates—meaning you only pay the higher rate on the specific dollars that fall into that tier—keeping these brackets broad and the rates low provides a substantial buffer for wage growth.

If you receive a significant promotion or take on a profitable side hustle in 2026, you will not suddenly lose a massive percentage of your extra earnings to a punitive pre-2018 tax bracket. Research from the Tax Foundation shows that permanently extending these rates provides critical stability for household financial planning and shields middle-income earners from a sudden reduction in take-home pay.

The Child Tax Credit Climbs to $2,200

Raising children is incredibly expensive, and the Child Tax Credit (CTC) has long been a vital lifeline for working families. Under the old law, parents were staring down a harsh reality for 2026: the CTC was scheduled to plummet from $2,000 per child down to just $1,000. Furthermore, the income threshold where the credit begins to phase out was scheduled to drop dramatically, threatening to disqualify millions of dual-income households.

The new rules provide massive relief. The base credit is officially increased to $2,200 per qualifying child. Crucially, the legislation introduces an annual inflation adjustment to the CTC starting in 2026, ensuring the credit does not lose its purchasing power over time. The income phase-out thresholds remain generous: the credit only begins to decrease once your modified adjusted gross income (MAGI) exceeds $200,000 for single filers or $400,000 for married couples filing jointly.

Additionally, the refundable portion of the credit—known as the Additional Child Tax Credit—has been expanded up to $1,700 per child. Refundability is a powerful mechanism; it means that if your calculated tax bill drops to zero before you exhaust your full credit, the IRS will send you the remaining balance as a direct cash refund. This guarantees that lower-income and middle-income families reap the complete financial benefit of the expanded credit.

The State and Local Tax (SALT) Cap Jumps to $40,400

If you live in a state with high income or property taxes—such as New York, California, or New Jersey—the $10,000 cap on the State and Local Tax (SALT) deduction has likely been a major pain point since it was introduced in 2017. Many homeowners found themselves paying tens of thousands of dollars in local property taxes that they were forbidden from deducting on their federal returns.

While the cap was scheduled to disappear completely in 2026, lawmakers compromised by raising the limit substantially rather than eliminating it entirely. Beginning in 2026, the SALT deduction limit jumps from $10,000 to $40,400. Furthermore, this cap is programmed to increase by 1% annually through 2029.

This increased ceiling is high enough to fully cover the local tax burdens of the vast majority of middle-class and upper-middle-class households. However, the legislation does include a targeted phase-out to prevent ultra-wealthy taxpayers from claiming massive deductions. If your MAGI exceeds $500,000, your allowable SALT deduction begins to phase down, eventually hitting a strict floor. For the average homeowner, this change represents a golden opportunity to resume itemizing deductions if their local tax burden exceeds the new standard deduction.

Brand New Write-Offs for Tips and Overtime Pay

In a major victory for service workers and hourly employees, the tax code now features two highly targeted, above-the-line deductions. Effective from 2025 through 2028, workers can actively shield large portions of their variable income from federal taxation.

First, the “No Tax on Tips” provision allows employees to deduct up to $25,000 of qualified tip income per year. To qualify, the tips must be earned in an occupation that customarily receives tips—such as hospitality, dining, or salon services—and the income must be officially reported on a W-2 or 1099 form.

Second, the “No Tax on Overtime” rule allows workers to deduct up to $12,500 of qualified overtime compensation. If both you and your spouse earn overtime pay, a married couple filing jointly can deduct up to $25,000. This applies specifically to the premium portion of time-and-a-half pay mandated by the Fair Labor Standards Act.

Because these are accessible to both itemizing and non-itemizing taxpayers, you do not need to give up your standard deduction to use them. However, high earners are excluded; both the tip and overtime deductions phase out completely if your MAGI exceeds $150,000 as a single filer or $300,000 as a married couple.

Seniors Gain an Extra $6,000 Deduction

Older Americans living on fixed incomes receive a significant boost under the new tax framework. For decades, the tax code has offered a modest “additional standard deduction” for individuals aged 65 and older. The newly enacted rules layer a massive bonus on top of that existing benefit.

From 2025 through 2028, taxpayers who are 65 or older by the last day of the tax year can claim a new $6,000 bonus deduction. This is calculated on a per-person basis, meaning a married couple where both spouses are 65 or older qualifies for a combined $12,000 reduction in taxable income. According to the IRS, this deduction is available regardless of whether you choose to take the standard deduction or itemize your return.

When you combine the $31,500 base standard deduction, the existing senior standard deduction add-ons, and this new $12,000 bonus, a qualifying older married couple can earn well over $45,000 before owing a single cent in federal income tax. Be aware, however, that this benefit targets middle-income retirees. The $6,000 bonus deduction begins to phase out if your modified AGI exceeds $75,000 for single filers or $150,000 for joint filers.

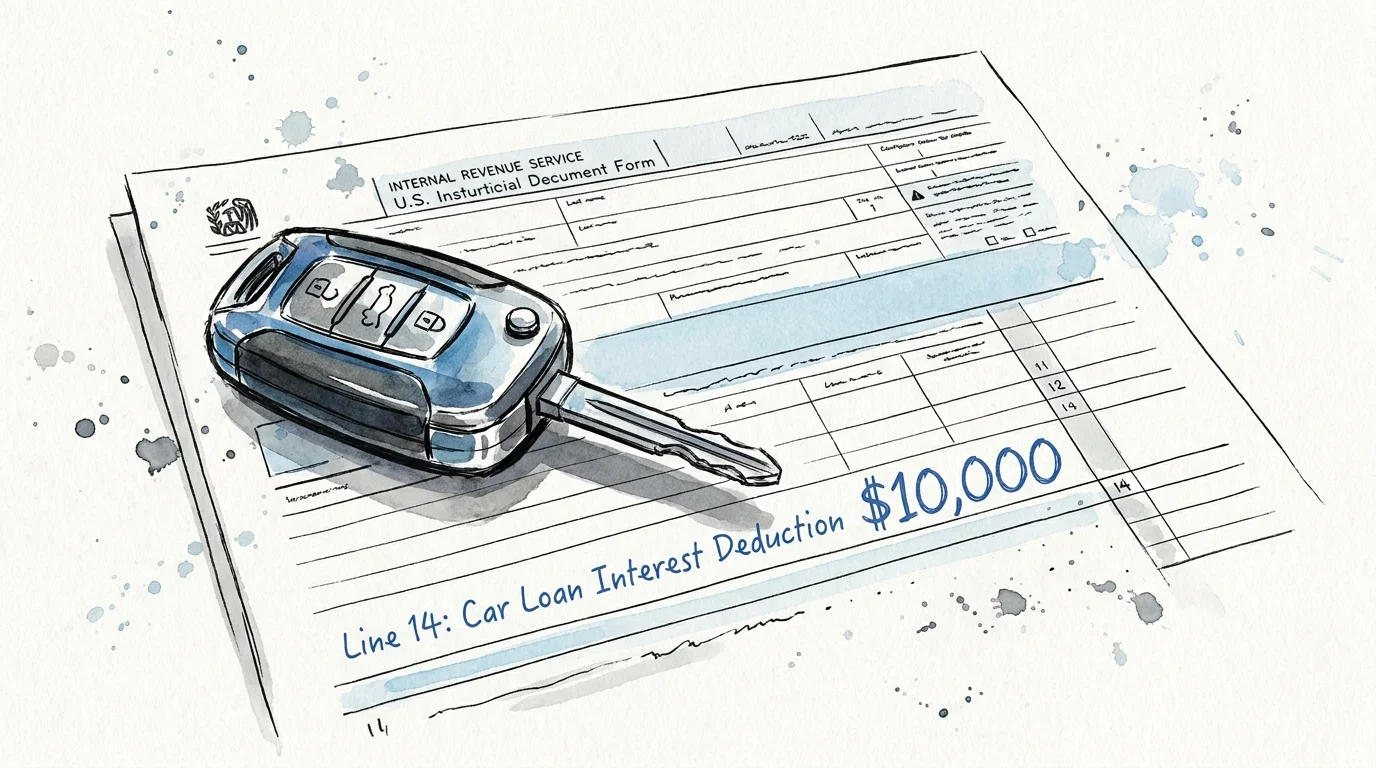

A $10,000 Deduction for Car Loan Interest

For the first time since the 1980s, you can deduct the interest paid on a personal auto loan. With vehicle prices and financing rates sitting at historically elevated levels, this temporary provision provides substantial relief for car buyers. You are permitted to deduct up to $10,000 of auto loan interest paid during the tax year.

However, the IRS has placed strict eligibility requirements on this write-off:

- Domestic assembly required: The vehicle’s final assembly point must be located within the United States. Imported cars are strictly ineligible.

- Personal use only: The vehicle must be purchased for personal use. Commercial vehicles or business fleets do not qualify under this specific rule.

- No used cars or leases: The deduction applies to new vehicle purchases only. Leased vehicles and used cars are excluded.

- Income restrictions: The tax benefit phases out if your modified adjusted gross income exceeds $100,000 for single filers or $200,000 for married couples filing jointly.

If you finance a $45,000 American-assembled truck at an 8% interest rate, you could easily pay over $3,000 in interest during your first year of ownership. Under the new law, every dollar of that interest directly reduces your taxable income.

What This Means for You

The expiration of the TCJA was universally expected to complicate tax planning and shrink paychecks. Instead, the current landscape offers a unique combination of permanent structural stability and lucrative temporary write-offs. By permanently securing the broader tax brackets and the elevated standard deduction, the government has given you a reliable foundation to plan your long-term wealth building.

To grasp the scale of the changes, it helps to view them side-by-side. The following table contrasts what Americans expected to face in 2026 versus the reality enacted under the new legislation.

| Tax Provision | Previous 2026 Scheduled Rule (Sunset) | New 2026 Rule Under Enacted Legislation |

|---|---|---|

| Standard Deduction (Married Filing Jointly) | Drop to roughly $14,600 | Permanent at $31,500 (plus annual inflation adjustments) |

| Income Tax Brackets | Revert to higher pre-2018 levels (top rate 39.6%) | Locked permanently at lower rates (top rate 37%) |

| Child Tax Credit | Drop to $1,000 per child | Increased to $2,200 per child (indexed to inflation) |

| State and Local Tax (SALT) | Unlimited deduction (cap expires) | Capped at $40,400 (increases 1% annually) |

| Qualified Business Income (QBI) | 20% deduction expires entirely | Made permanent for eligible pass-through businesses |

“The One Big Beautiful Bill Act makes many of the individual tax cuts and reforms of the TCJA permanent. It improves upon the TCJA by making expensing for R&D and equipment permanent.” — Tax Foundation

Analysis by the Brookings Institution highlights that while these cuts will boost short-term household income, the long-term macroeconomic impacts—particularly regarding the national deficit—will require ongoing attention. For the everyday taxpayer, however, the immediate directive is clear: update your tax strategy to capture every new deduction you qualify for.

What Can Go Wrong

While the new tax landscape is overwhelmingly taxpayer-friendly, it introduces significant complexity. Navigating these rules incorrectly can lead to denied deductions, unexpected IRS correspondence, or leaving thousands of dollars on the table.

- Tripping over the income phase-outs: Nearly all of the new temporary benefits—including the tip, overtime, senior, and car loan interest deductions—feature strict MAGI phase-outs. Earning just a few thousand dollars over the limit can rapidly diminish or entirely erase your eligibility for these write-offs.

- Misunderstanding the car loan rules: It is easy to assume any new car purchase qualifies for the interest deduction. If you fail to verify the vehicle’s final assembly location before signing the financing paperwork, you will lose the deduction entirely.

- Failing to report tip income: The “No Tax on Tips” provision requires a paper trail. If you receive cash tips and fail to report them to your employer for inclusion on your W-2 or 1099, you cannot legally claim the deduction at tax time.

- Assuming temporary provisions are permanent: While the standard deduction and tax brackets are locked in, the specific deductions for tips, overtime, car loan interest, and the $6,000 senior bonus are strictly temporary and set to expire after 2028. Do not build decades-long financial plans around these short-term benefits.

Where Outside Advice Pays Off

Filing a basic W-2 tax return remains straightforward, but as soon as your financial life involves businesses, estates, or complex retirement drawdowns, the new rules drastically increase the value of professional guidance. Engaging a certified public accountant (CPA) or a credentialed financial advisor is highly recommended in the following scenarios:

- Estate Planning: The legislation permanently increased the federal estate and gift tax exemption to $15 million per individual. While this shields the vast majority of families from federal estate taxes, state-level estate taxes still apply in many regions. A professional can help you update your trusts and gifting strategies to match the permanent federal limits.

- Structuring a Small Business: Because the 20% Qualified Business Income (QBI) deduction was made permanent, the legal structure of your business matters more than ever. An advisor can calculate whether operating as a Sole Proprietor, LLC, or S-Corporation yields the highest tax savings under the permanent framework.

- Managing Retirement Withdrawals: If you are over 65, your goal should be to maximize the new $6,000 senior bonus deduction. Because this deduction phases out at $75,000 for single filers and $150,000 for joint filers, an advisor can help you perfectly time your IRA withdrawals and Social Security strategy to keep your MAGI just below the phase-out threshold.

Frequently Asked Questions

Did the 2017 tax cuts expire?

No. While many provisions of the 2017 Tax Cuts and Jobs Act were scheduled to expire at the end of 2025, new legislation passed in mid-2025 made the core individual income tax brackets and the elevated standard deduction permanent.

Can I deduct my car loan interest if I bought a used car?

No. The new car loan interest deduction is strictly limited to new vehicles purchased for personal use. Additionally, the vehicle must have its final point of assembly within the United States. Leased vehicles and used cars do not qualify.

Do I need to itemize my taxes to claim the new overtime and tip deductions?

No. The deductions for qualified tip income and qualified overtime pay are available to both itemizing and non-itemizing taxpayers. You can safely take the $31,500 standard deduction (for married couples) and still deduct your eligible tips and overtime on top of it, provided you meet the income requirements.

Is the $10,000 SALT cap gone forever?

Not exactly. The strict $10,000 cap was raised to $40,400 for the 2026 tax year and is programmed to increase by 1% annually through 2029. However, taxpayers with a modified adjusted gross income over $500,000 will see their allowable SALT deduction phase down.

By understanding how the permanent brackets, larger standard deductions, and temporary write-offs interact with your unique situation, you can proactively structure your finances to lower your tax burden. Track your qualifying expenses carefully, verify your eligibility for the new income-based write-offs, and adjust your payroll withholdings if you expect a significantly lower tax bill next spring.

This is general informational content based on widely accepted guidance. Individual results vary. Verify current details—rules, prices, eligibility, regulations—with official sources before making important decisions.